Weekly insights about property in France!

Subscribe and don't miss an issue!

French Property Market Report

Volume XIX, Issue 10

As reported by the Chambre de Notaires de France, January 2021:

Market resilience and new real estate patterns in 2020?

At the end of 2020 the real estate market had already proven very resilient, supported by parameters that until now have provided reassuring momentum. Key questions remain, however, as to its durability. In 2021, will the market stand the test of a seemingly inevitable economic crisis, the true profile of which remains very much to be seen? Are the recent trends purely reactions to an unprecedented and unusual pandemic period, or do they mark the beginning of a new approach to buying property? Has this crisis simply expedited ongoing projects, or does it herald the start of a more fundamental shift?

At the end of 2020 the real estate market had already proven very resilient, supported by parameters that until now have provided reassuring momentum. Key questions remain, however, as to its durability. In 2021, will the market stand the test of a seemingly inevitable economic crisis, the true profile of which remains very much to be seen? Are the recent trends purely reactions to an unprecedented and unusual pandemic period, or do they mark the beginning of a new approach to buying property? Has this crisis simply expedited ongoing projects, or does it herald the start of a more fundamental shift?

The latest analyses of volumes for France as a whole show that since the second half of last year, results have been somewhat erratic, fluctuating from one month to the next at around the one million transaction mark. However, since late October 2020, the year-to-year volume of transactions on older properties has once again crossed this symbolic threshold, reaching 1,020,000 transactions at the end of November 2020, down only 4% compared to November 2019. There is every reason to believe that December 2020 will confirm this moderate downward trend at a national level. As we set out a few weeks ago, the market for older properties is expected to close 2020 at around 1 million transactions.

Despite the challenging operating conditions (as seen across the board), and despite the support of French-State guaranteed loans, banks have continued to play their “solvency role,” as confirmed by the steady growth in new home lending at a rate of +5.5% in October 2020, amid a slight decline in renegotiations of property loans.

This trend is expected to be confirmed in 2021, driven initially by interest rates remaining very low and falling steadily since July 2020 thanks to the action taken by the European Central Bank (ECB). Indeed, rates are currently very close to their historic low. A new development that is helping maintain a robust market comes from the now encouraging recommendations of the French High Council for Financial Stability (HCSF).

On December 17, 2020, the HCSF settled on less restrictive adjustments in terms of granting property loans, particularly to help first-time buyers. This initial observation is reassuring: such a slight decline in volume is the lesser evil after weeks of a near total standstill in economic activity—real estate activity in particular—between March and May 2020. Nevertheless, the dynamic is more complex than it seems, given the large gap between the French provinces, where volumes remained strong, and Greater Paris where they dropped by more than 15%.

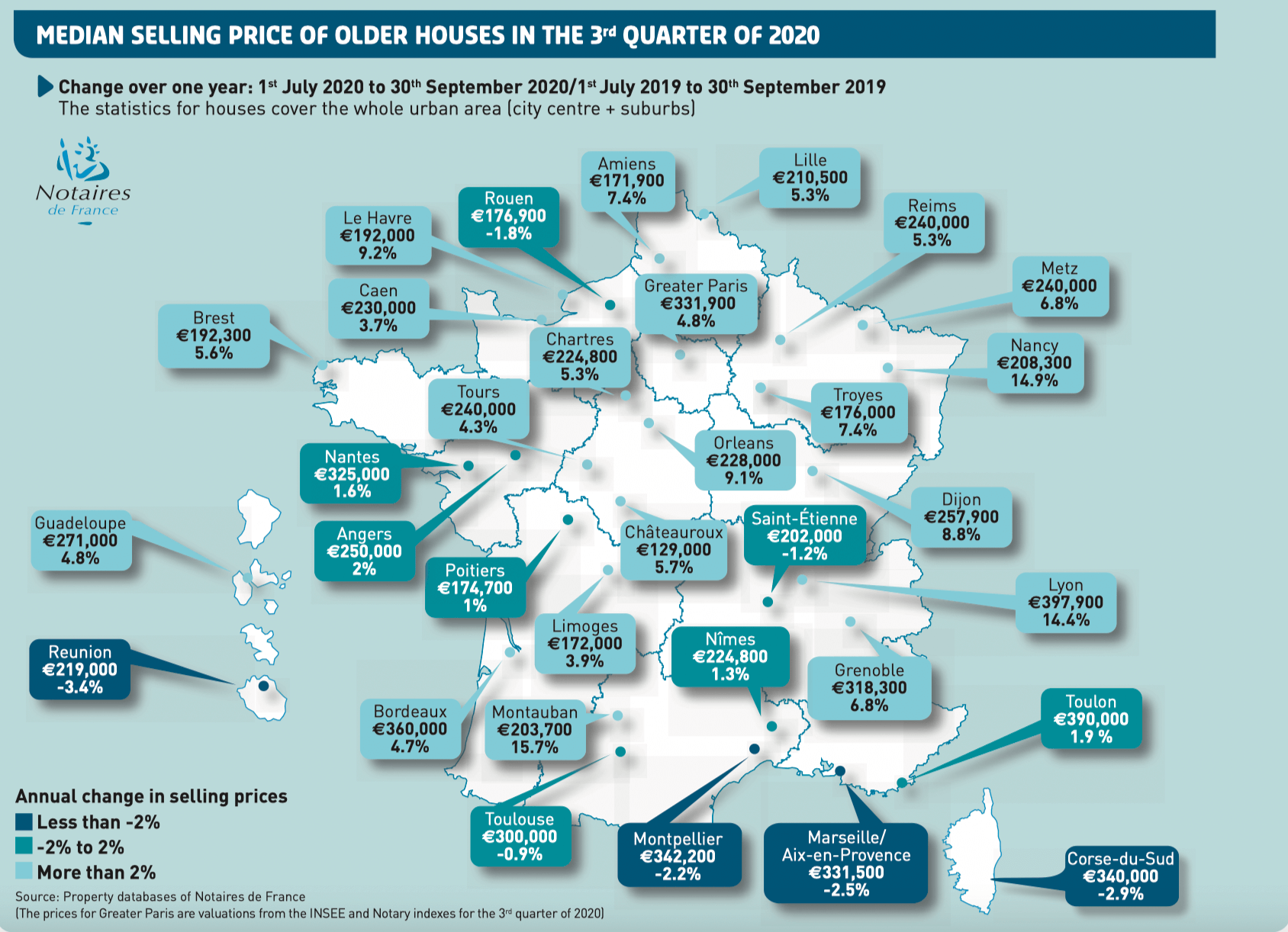

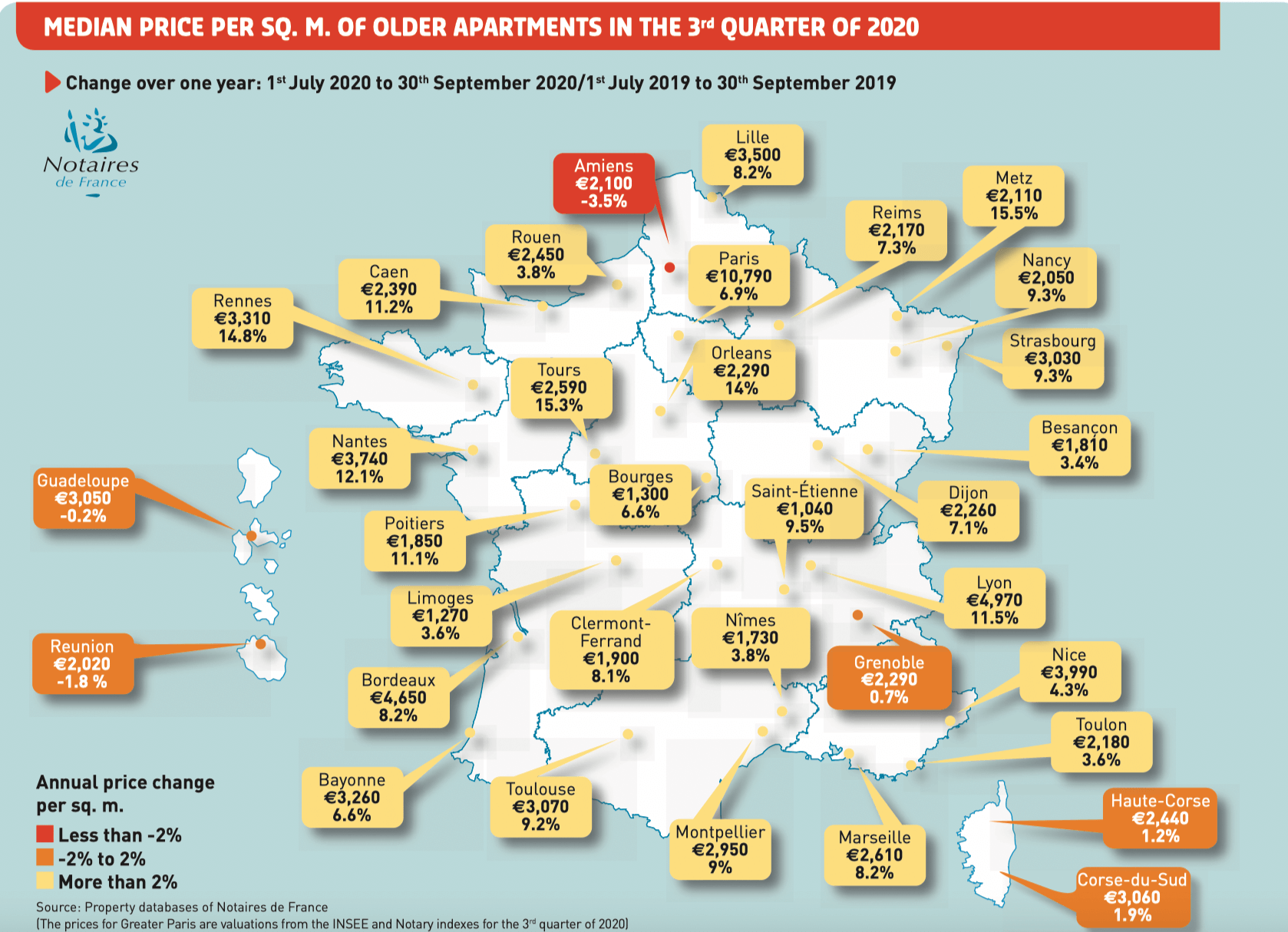

As such, volumes have clearly held up at national level, but in very different ways. In Greater Paris, the underperformance of volumes is already having an impact on prices: prices are rising less quickly than in previous quarters (+0.5% between 2nd Quarter and 3rd Quarter of 2020, after +1.8% and +2%)—a trend confirmed for inner Paris by the leading indicators from pre-sale contracts. Therefore, year-to-year prices will have increased less in the French capital than in the whole of the Greater Paris region, something that has not happened since 2013.

A shift in the market in 2021?

While it was often said that Paris could be the driving force behind the Greater Paris property market, 2020 definitely put this idea up for debate. The health crisis and initial lockdown brought about a collective awareness in the urban environment, and even more so in the Parisian market: too many financial constraints, a tough market, longer travel times… These are all factors that caused Greater Paris residents to spread out towards Normandy, La Perche or Burgundy, having been unable to purchase a house with a garden in the outer suburbs. Generally speaking, there has been a shift among the urban population towards greener areas. What’s more, with the sudden and widespread surge of remote working, with employers now being more open to this way of operating, employees are more able to organize themselves differently and create a family life in a greener space, with two distinct living areas (one close to the workplace and one as a family setting). As such, while the volume of transactions at national level fell by 4% year-to-year in November 2020, on the Paris market it dropped 18%.

Price trends coincided with the same area of disruption and the rise eased off in 3rd Quarter of 2020 in Greater Paris (+0.5% compared to 2nd Quarter). Paris saw the same slowdown with +6.9% annual growth in 3rd Quarter (after +8% in 1st Quarter). Negotiations for properties are tougher and last longer in Paris, while the market in the outer suburbs and provinces is smoother and more accessible. As a result, Greater Paris buyers have seen a marked increase compared to 3rd Quarter of 2019 in Yonne (27% +9 points), Eure (22% +6 points) and Orne (21% +6 points) in departments bordering Greater Paris.

Whenever there was a drop in the Parisian market, it was often said that this heralded a downturn in the national property market. Yet the health crisis is now casting doubt on this assumption, particularly given the resilience of the property market’s volumes in the provinces. Indeed, it might not be so much a reversal in market trends, as a shift towards a real estate market that is more provincial, closer to nature and with more space, while still remaining connected. The shift may also be fueled by the pursuit of a dual living environment.

Whether it is a collective increase in awareness or merely the acceleration of a lifestyle change that was already in motion prior to the health crisis, a fundamental movement seems to be underway, leading to new plans by investors or residents in the French provinces and outer suburbs rather than in Paris.

It remains to be seen whether this movement will continue beyond the pandemic, given that eight inter-municipal associations and metropolitan areas have expressed their interest in joining the rent control experiment that is currently underway in Paris and Lille. These include Lyon, Bordeaux, Montpellier and Grenoble among others. For those who chose bricks and mortar as their safer investment over the low returns offered by euro life insurance funds, this could act as a deterrent, unless they move their investment projects to more medium-sized cities where recent performances indicate renewed vitality.

Likewise, some cities are openly opposed to “overbuilding,” preferring to pursue the promise of a greener living environment following the example of Grenoble, which seems to be paving the way for Bordeaux, Lyon, Marseille, Strasbourg, Besançon and Poitiers. This movement is a concern for the building sector and will undoubtedly have an impact on the volume of transactions in cities with a risk of putting pressure on prices. To date, this trend has more of a rebalancing effect on the market and, once again, involves a potential shift to medium-sized cities that still offer all facilities in terms of connections.

Foreigners are notably absent on the national map. The share of non-resident foreign investors (a key factor for places of investment and a driving force for property prices to rise) is now close to its lowest level in 10 years (1.5% in 2019). In the same vein as French residents, non-resident foreign buyers in the provinces are shifting their investment from urban centres to rural areas. And Paris has been no exception: if we look at the most sought after arrondissements by non-resident foreign buyers (the 6th, 7th, 8th and 16th), their market share is clearly declining, particularly in the 6th arrondissement which accounted for 17% of buyers in 2015, yet only 9.4% in 3rd Quarter of 2020.

More generally, a prolonged health crisis can only damage a sector that was inevitably entering a phase of slowdown. The property market is unlikely to be able to evade the looming economic and social crisis.

Pre-sale Contracts

According to projections from pre-contracts, the price trend seen in 3rd Quarter of 2020 in mainland France is expected to continue until February 2021 at a similar pace in the apartment market (+0.6% compared to +0.7% in 3rd Quarter of 2020), but a faster pace in the house market (+1.6% compared to +0.3% in 3rd Quarter of 2020).

In the French provinces, projections from pre-sale contracts for the end of 2020 point to a further acceleration in the rise in house prices, with quarterly trends of +3% for houses and +2% for apartments at the end of December. At the end of February 2021, increases will be more moderate (around 1.5% for each of these markets).

According to indicators from pre-contracts, in Greater Paris the price per square metre is expected to peak in November 2020 at around €10,900, before falling very slightly for three consecutive months. In February 2021, the sale price per square metre is expected to be around €10,700 in Paris, i.e. a 1.7% decrease over three months. However, taking into account the accumulated increases in 2020, prices should still show a 3.4% annual rise in February 2021. Apartment prices appear to be stabilising in the inner and outer suburbs, trending at -0.1% and -0.4% respectively from November 2020 to February 2021.

Editorial Comment: While we are not experiencing a downturn in foreign investment by North American buyers, it is true that our buyers have expanded their horizons outside of Paris to other parts of France, particularly the Côte d’Azur. Paris buyers are moving away from the 6th, 7th, 8th and 16th arrondissements, one can assume factors such as price and popularity to affect decision to seek out other districts.

To read the report in its entirety, download the PDF.

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group

P.S. Interested in learning more about Paris and France than just property issues? If you aren’t already a reader of Adrian Leeds Nouvellettre®, our twice-weekly Nouvellettre® devoted to life, culture, and insights to living in Paris, Nice, and all of France, then be sure to subscribe to it now. Just click here to secure your subscription.

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.