Weekly insights about property in France!

Subscribe and don't miss an issue!

The Loan Process: Today’s Reality

Volume XIX, Issue 44

The Local just published an article titled “Three ways the 2022 budget makes it easier to buy or renovate French property.” It’s all about a number of measures taken by the government to offer zero interest loans to “first-time and low-income buyers, seeking to invest in B2 or C zone properties (which excludes Paris), and not earning above a fixed amount (which varies according the number of people who will live in your future household).”

This lets out just about all of you, I imagine. Meanwhile, we’re tearing our hair out just trying to process the loans at all for our North American clients. There are very few banks willing to lend to us Americans, and we have FATCA and our own US government to thank for that. Add to it the banks’ own rules that limit age and their discrimination against self-employed persons, and you’ve got even more challenges. The flip side is that interest rates are well below two percent and that’s what I call “free money.”

Even with all that, our preferred broker, Kim Bingham at Private-Rate, can be quite successful in acquiring financing for our clients. But, here’s the new catch; internally, the bank personnel are experiencing burn-out and are simply not doing their jobs. They are taking long absences, not responding to emails and not doing the paperwork. Kim is tearing her hair out, way more than we are.

Here’s how it plays out; Under normal circumstances we can ask for 90 days from the signing of a pre-sale agreement to process the loan. That used to be more than enough time and the seller was normally willing to wait that long. Since the pandemic, that has changed as the banks cannot process the file within that time frame. The sellers don’t want to wait longer and will reject the purchase if we aren’t clever about it…so we have no choice but to agree to 90 days, knowing full well there may be a problem meeting the deadline. It’s a risk we all take, but the only choice is then not to take the loan and/or not buy the property.

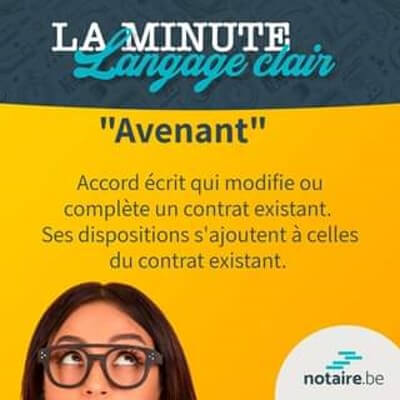

In many situations this past year, the bank has needed extensions. It starts with one and that’s not too difficult to achieve, if the extension is not too long…say two weeks. But, then there’s usually a second extension, and possibly a third one, and so forth. The seller must sign off on it in the form of an “avenant” or amendment to the pre-sale agreement.

In many situations this past year, the bank has needed extensions. It starts with one and that’s not too difficult to achieve, if the extension is not too long…say two weeks. But, then there’s usually a second extension, and possibly a third one, and so forth. The seller must sign off on it in the form of an “avenant” or amendment to the pre-sale agreement.

The sellers aren’t always so agreeable. They want their sale and they want their money. They could refuse the amendment and if they do, the buyer would be legally obligated to forfeit their 10 percent deposit held in escrow. That’s a steep price to pay and this is the risk. The saving grace is that the Notaire cannot turn over the 10 percent deposit without the permission of the buyer. Therefore, the buyer could force the seller to sue him for the money—not something anyone wishes for—and therefore it’s an incentive for the seller to agree to the extension. On the other hand, 10 percent can be quite a lot of money and might be attractive to the seller, less the cost of legal fees to acquire it.

Our solutions to appeasing the seller are varied, from offering that the buyer cover the seller’s carrying costs during the waiting period, such as the utilities, mortgage interest, etc.; to offering to transfer the amount of the down payment to the seller as additional earnest money; to writing a “lettre de motivation” that appeals to the seller’s heart rather than his pocket book. Whatever works!

Other options have been for the buyer to pay in cash and then get a post-sale loan, which the banks are willing to do. But, the buyer needs to be able to get their hands on the cash. None of this is simple or easy, not even for those with the deepest of pockets.

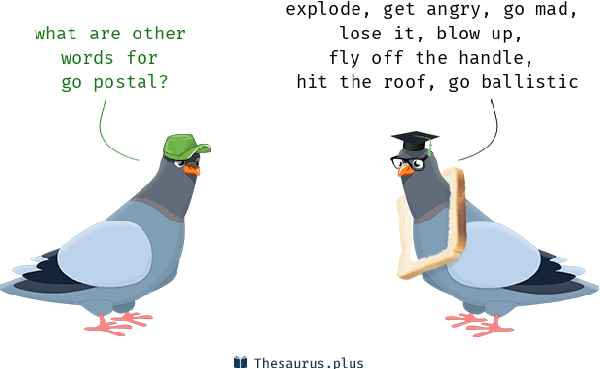

I write this today because we’re battling with a few files with these very same issues. Our clients risk losing the purchase of the properties, as well as their 10 percent deposits. We have no control over it and are at the mercy of the bank personnel who are “going postal” as a result of Covid-19 confinement plus excessive work loads. We’ve had delays up to four and five months!

(Going postal is an American slang phrase referring to a person going into extreme and uncontrollable anger, often bordering on violence and typically in a work environment. The phrase is derived from a series of mass killings by United States Postal Service (USPS) employees of superiors, co-workers, and police or civilians. For example, between 1970 and 1997, approximately 40 people were killed by USPS employees and former employees in about 20 work rage events. In the United States, between 1986 and 2011, workplace shootings occurred on average twice a year for a total of approximately 11.8 deaths per year. Source: Wikipedia.org)

We can do very little about the situation with the banks, but we do have to manage the expectations of our clients. So, if you are “smartly” entertaining a mortgage…”smartly” because money is virtually free right now…do so with an eye on the reality of today’s world.

Be prepared for just about any scenario…

For more information about interest free loans, visit the Notaires France website.

To contact Kim Bingham, visit our Get Financing page, and be sure to tell her we sent you.

A bientôt

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. This year, we took one extra day off from publishing French Property Insider during our conference and tour in the South of France in October. Because we promise 50 issues, we will be make an exception by publishing on Thursday, November 25th on Thanksgiving Day, which is normally a holiday for us…and for you! Enjoy!

2 Comments

Leave a Comment

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.

Adrian, have you ever thought of leveraging an individual’s 401k to bridge the gap if there is a delay in the mortgage loan process? As you know, many Americans have substantial 401K balances and many of those 401k plans allow the owner to take a loan against the balance. If the problem is mainly just a delay, as opposed to the possibility of the loan not being given, is there a way for somebody to use a loan from their 401k as a “bridge loan” until the delayed financing from the French bank is finalized? Then might they be able to use the French loan to pay back the 401k? I am by no means an expert and there may be any number of laws I am not aware that might make this process impossible but I thought I’d ask the question.

Yes, we have. We work with an excellent financial advisor who can assist our clients with alternative solutions.