Weekly insights about property in France!

Subscribe and don't miss an issue!

A Careful Comeback: More Sales, Steadier Prices, and a Market That Rewards Prepared Buyers

Volume XXIV, Issue 05

By Jay Corless, edited by Adrian Leeds

In the latest Notaires de France “Note de Conjoncture Immobilière” (their periodic market snapshot), the message is reassuring—but measured: the French housing market is no longer sliding, and it’s beginning a measured, orderly recovery. Not a stampede. Not a boom. More like a return to circulation—buyers and sellers moving again, with financing still acting as the great gatekeeper.

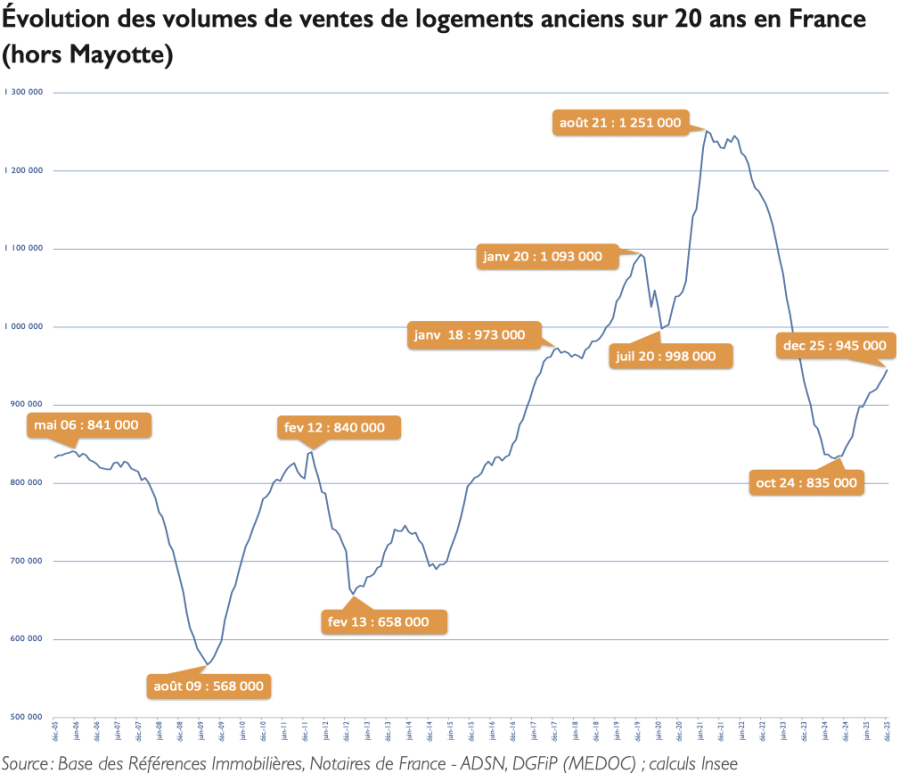

The clearest sign of that “back to life” moment is transaction volume. Over the rolling 12 months ending December 2025, France recorded 945,000 sales of “logements anciens” (existing homes), up roughly 12% year-over-year. That’s real progress after the slowdown of the last two years. At the same time, it’s worth keeping perspective: activity remains about 25% below the 2021 peak. In other words, the market is improving, but it’s doing so without the excess heat that can make buying from abroad feel frantic and opaque.

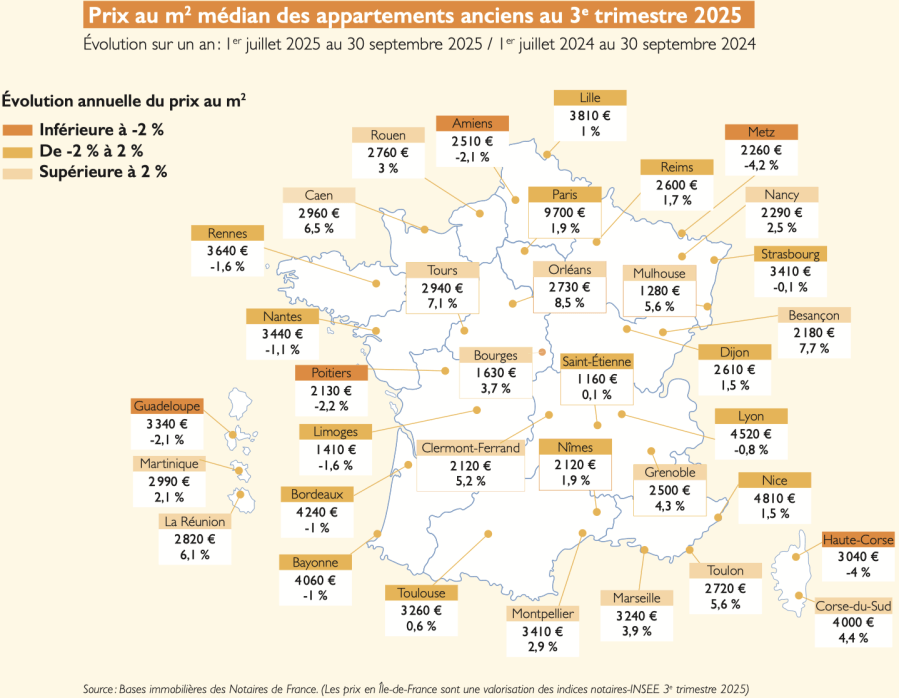

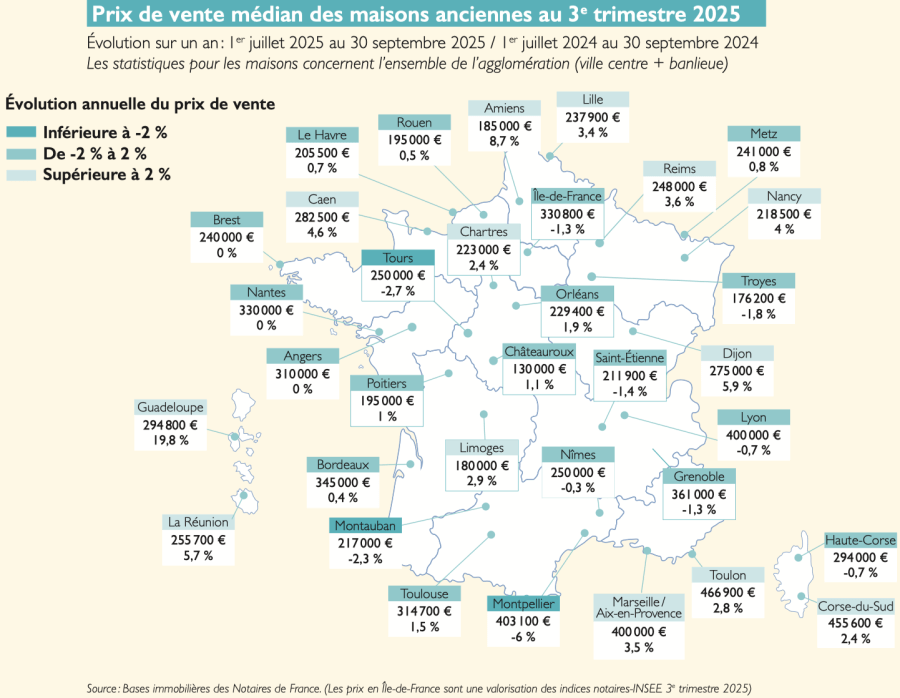

Prices, too, are telling the story of normalization rather than acceleration. In Q3 2025, national price change over one year was modest—+0.7% across existing homes—driven more by “appartements anciens” (apartments, +1.3%) than “maisons anciennes” (houses, +0.2%). If you’re looking for drama, you won’t find it here; the adjustment is happening through the very French mechanism of “négociation”—meaning the final agreed price is increasingly shaped after the property is listed, as buyers take time, compare, and negotiate. That’s not a bad thing for well-prepared purchasers.

For many of you, of course, the real question is Paris and the surrounding region. Here the report is especially interesting: after ten consecutive quarters of decline, Île-de-France has edged back into slightly positive territory (+0.4% year-on-year in Q3 2025). But the recovery is uneven—and very revealing. Apartments in the region were +1.3% year-on-year, while houses were still -1.3%. Paris apartments, in particular, showed the clearest bounce, +1.9% year-on-year. This split makes intuitive sense in a tighter credit environment: apartments are the region’s core product—more liquid, more in demand, and often easier to finance than a larger house farther out.

The Notaires’ near-term indicators—based on signed preliminary agreements, the “avant-contrats” (contracts signed before the final deed)—suggest this gentle upward drift continues into early 2026. Their projections through the end of February 2026 point to France: apartments +1.4% year-on-year and houses +0.4%, while Île-de-France apartments are projected at +1.7%, with Paris at +1.5%. Again: calm, contained, and segmented by property type.

If there is one constant underpinning all of this, it’s financing. Banque de France data cited in the Notaires’ snapshot shows the average interest rate on new housing loans (excluding renegotiations) was stable around 3.10% in November 2025, and the monthly production of new housing credit was around 12.3€ billion. Translation: the credit machine is functioning again, but it’s selective, and availability matters. If you need a loan, your timeline will often be dictated by the financing pathway; if you’re a cash buyer (or close to it), the current environment can quietly strengthen your negotiating position.

One of the most telling phrases in this issue is that the market increasingly resembles a “marché d’utilisateurs”—a “user’s market,” in the sense that it is driven more by people buying to live in the home (or truly use it as a base) than by pure investor speculation. The Notaires also underline investor hesitation linked to a perceived instability around regulation and taxation for “investissement locatif” (rental investment). For many North American buyers, that corresponds to the lived reality we see every day: Paris for culture and access; a pied-à-terre for work and family; the coast or countryside for a different rhythm of life.

Meanwhile, the new-build market is still constrained—an important backdrop, because when new supply is weak, pressure and demand tend to concentrate in the existing-home market (“ancien”). National construction statistics published by the SDES show softer authorizations and starts around late 2025, supporting the idea that supply relief from new construction is limited in the short term.

And because France is never just one market, this Notaires issue also zooms in on ski resort apartments—useful for anyone contemplating a mountain base. Median prices per square meter remain undeniably premium (Val d’Isère, Courchevel, Tignes, Chamonix among them), with momentum varying by resort, and with apartments representing the majority of resort resale transactions. If a ski home is on your horizon, this segment is where “copropriété” (co-ownership rules and charges), building quality, and rental constraints are as important as the view.

So where does that leave you as a prospective buyer? In a market like this—recovering, but not overheated—success tends to come from preparation and process. Our role is to help you keep control from first visit to keys: to structure the search intelligently, negotiate with data and positioning, coordinate the players (agents, brokers, notaires, diagnosticians), and help you read the documents that matter—especially the “compromis de vente” (preliminary contract) and the property’s diagnostic and co-ownership file—so there are no surprises hiding behind charming shutters. In 2026, France isn’t rewarding impulsive buying. It’s rewarding informed buying.

Read the report in its entirety (in French).

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. We’re the folks who can make your French property investment dream come true, while protecting you from making serious mistakes. Review the services we offer to help you find the perfect property in France!

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.