Weekly insights about property in France!

Subscribe and don't miss an issue!

A Market in Decline—A Perfect Time to Buy

Volume XXI, Issue 31

The analysis of the real estate market in France is taken from the Note de Conjoncture Immobilière des Notaires de France. It presents the real estate situation in France, its trends and the evolution of property prices, with a projection until July 2023.

A Market in Decline

The cumulative volume of transactions for existing homes over the last twelve months in France (excluding Mayotte) reached 1,029,000 transactions at the end of May 2023. Since August 2022, the number of transactions carried out over the last twelve months has been contracting by around 5% month after month, but since the beginning of this year, the declines have taken on a greater magnitude, almost doubling (-12.6% until the end of May 2023). The deterioration in volumes is directly linked to the inflationary context and the sharp and rapid rise in interest rates, but also to the end of a golden age in which all the parameters contributed to a euphoria that itself called for the inevitable end of this cycle. The Notaires also noted that spring, traditionally synonymous with the peak of activity in the real estate year, will not have had any catch-up effect this time, confirming a market that is increasingly slowing down.

According to projections based on pre-sale contracts until the end of July 2023, prices of existing homes in mainland France appear to be entering a phase of decline: following the gradual deceleration in price rises observed since September 2022, prices are expected to fall by 1% year-over-year. The fall recorded in the multi-family market (-1.4% year-over-year) could be greater than that recorded in the single-family market (-0.7%).

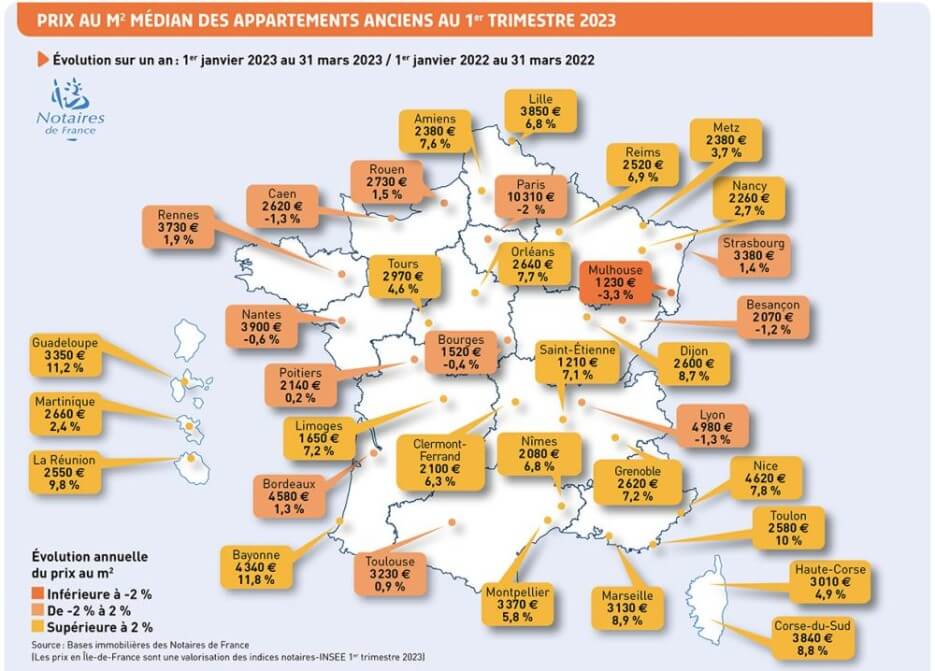

In the provinces, prices of existing homes are still expected to hold up at the end of July 2023, with an annual change of +0.2%. In contrast to the situation in mainland France, prices of existing apartments (+1.2%) are expected to continue to rise slightly, while those of existing houses will be virtually stable (-0.2%). At the end of July 2023, the vast majority of towns whose prices for existing apartments were still rising in the first quarter of 2023 could show stable or falling prices. This is the case, for example, in Rouen and Nantes, where prices were stable at the end of March 2023, but are expected to fall by around 4% by the end of July 2023. In Lyon, prices are expected to fall by 3% (versus -1% in First Quarter 2023). In terms of sales of existing homes in the largest regions at the end of July 2023, the picture could be similar, with negative trends of greater magnitude than for existing apartments. Declines of between 4% and 9% are expected in Angers, Saint-Étienne, Nantes, Lille, Dijon, Toulouse, Rouen and Strasbourg.

In the Paris region, an increasingly marked deterioration in activity and falling demand are leading to further price adjustments: annual price falls are set to spread to all markets in the Paris region by July 2023. Moreover, the annual rate of decline is set to accelerate (-4.8% for apartments and -3.2% for houses in July). This could be a departure from the trend seen from 2013 to 2015, with annual declines of between 1% and 3%. However, the pace of decline is still slower than during the subprime crisis, when annual prices fell in 2009. In Paris, the price per square meter will be €10,310 in the First Quarter of 2023. The downward trend, so far limited to 2%, could rise to 5% year-over-year in July 2023, for a price of €10,090. If the downward trend continues, the price could fall below €10,000 per square meter in the 3rd quarter of 2023.

The predicted adjustment in prices, the logical and mechanical consequence of falling volumes, is fast approaching, albeit in a disparate manner across the country, with some areas still benefiting from their natural attractiveness, such as the coastline. But the period of bullish prices, boosted by abnormally low interest rates, is well and truly over. The market has yet to find a new dynamic, as the sharp rise in interest rates has put a damper on buyers and driven out first-time buyers, whose income levels are no longer sufficient to make a purchase. The panel of potential buyers has been largely reshuffled by the increasingly complex use of credit and trade-offs against real estate acquisition in view of the French people’s living standards. At the same time, Notaires are seeing a return to traditional negotiation, coupled with a mechanical increase in sales lead times due to a wait-and-see attitude on the part of buyers. After having largely benefited sellers, the market is now turning around. It can only be unblocked when sellers agree to lower their prices, which, in view of the price rises of recent years, is by no means prohibitive for the time being. Nevertheless, it should be noted that these price and volume reductions will have an impact at the local level on the collection of transfer duties, in an already delicate context of public finances.

In this gloomy climate, the Banque de France nonetheless predicts that “after peaking in the second quarter, total HICP (Harmonized Index of Consumer Prices) inflation will gradually ease in the second half of 2023 and beyond, returning to around 2% by 2025, subject to the absence of new shocks on imported raw materials.”

In any event, the year could end at around 950,000 transactions, signaling a very sharp deceleration over the year, taking us back to a pre-2018 pace. The real estate market as a whole is undergoing a period of brutal readjustment, with the new-build market suffering a severe downturn, due to the lack of a position from the public authorities on a new Pinel-type rental investment scheme, but also to constrained production costs for developers which, correlated with an inevitable increase in the savings effort imposed by rising interest rates, are squeezing the potential for buyers.

The Return of the Non-resident Foreign Buyers in 2022

After peaking in 2015 at 2%, the share of non-resident foreign buyers in mainland France fell almost continuously until 2020. After this year, marked by the onset of the health crisis, it stabilized at 1.3% in 2021. The year 2022 marks the return of non-resident foreign buyers, who account for 1.8% of all transactions for existing homes. This is confirmed in the First Quarter of 2023, with an equivalent proportion.

This increase is felt throughout the country, but is particularly significant in Provence-Alpes-Côte d’Azur, where the share of non-resident foreign buyers rose from 3% in 2021 to 3.8% in 2022. However, this share remains much lower than in 2015, when it reached 5.2%. Nouvelle Aquitaine, Occitanie and Bourgogne – Franche-Comté also see a significant rise in the share of purchases by non-resident foreigners, which will represent between 2% and 2.4% in 2022 (i.e., around +0.5 points over one year). In Brittany, Hauts-de-France, Centre – Val de Loire and Pays de la Loire, non-resident foreigners account for less than 1% of purchases.

![]()

Creuse, Alpes-Maritimes and Ardennes are among the most popular départements for non-resident foreign buyers in 2022. While Creuse retains top spot, with 8% of transactions within the département, it is the one where the share of non-resident foreign buyers has fallen the most, particularly between 2019 and 2021, from 11% to 7%. In the Alpes-Maritimes, the share of non-resident foreign buyers is stable at 7% compared with 2019. By contrast, the share of purchases by non-resident foreigners in the Ardennes has risen steadily, from 4% in 2019 to 7% in 2022. Ten years ago, they accounted for just 2% of purchases. In Île-de-France, the share of non-resident foreign buyers reaches its highest level in the last ten years, at 1.2% in 2022 and up to 1.6% in Q1 2023. Nonetheless, they are poorly represented outside the capital. After hovering around 2.3% between 2019 and 2021, the proportion of non-resident foreign buyers in Paris reached a ten-year high of 3.4% in 2022 (+1.2 points year-over-year). At the start of 2023, the increase in the proportion of non-resident foreign buyers in Paris is confirmed: they represented 4.2% of buyers in the First Quarter of 2023.

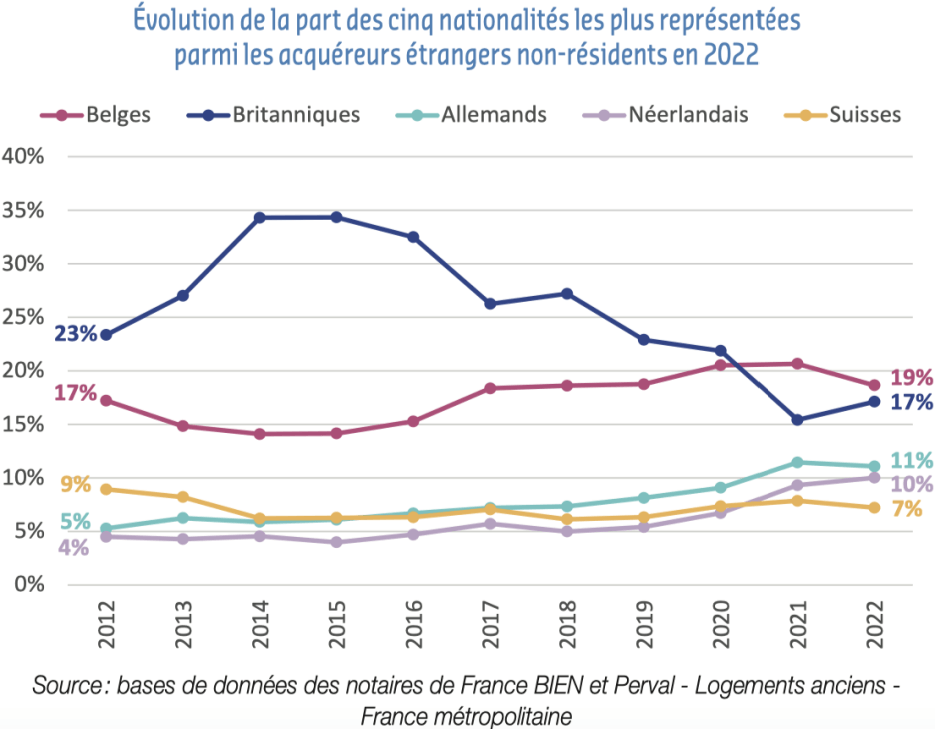

The British share, which has been falling steadily since 2016, fell sharply between 2020 and 2021 (-6 points), dropping below the 20% threshold for the first time. This drop is similar to that recorded between 2016 and 2017 at the time of the referendum on the United Kingdom’s membership of the European Union. Despite a 2-point rise in 2022, they do not regain top spot in the ranking, with 17% of purchases among non-resident foreigners. Since 2021, Belgians have been in the lead with 19% of purchases. Nevertheless, their share registers its first decline since 2014, down -2 points year-over-year.

For more information, visit these sites:

• For the property price charts

You can also download the full PDF report.

To learn more about purchasing property in France, visit our website.

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. Due to a last-minute rental cancellation, Le Jardin de la Promenade in Nice is available for bookings through August 26.

Visit our website for details and contact information TODAY!

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.