Weekly insights about property in France!

Subscribe and don't miss an issue!

Are you Subject to Wealth Tax in France?

Volume XX, Issue 19

Note: The following information has been extracted from France Notarial websites…

Taxes are not a fun subject, but a necessary factor in our lives, especially in France which is famous for its high taxation, but just as famous for its huge and strong safety net provided for all of its citizens.

Article published December 5, 2018 in the Guardian

Every year, taxpayers residing in France, or having financial resources from French sources, must declare their income to the Fisc (tax department).

Being tax resident in France, in loose terms, is a minimum presence of 183 days or if your home in France is your habitual and permanent place of residence. This is becoming increasingly more difficult to determine as our lives have become more transient, something with which governments are already grappling.

See this government website for the details of the rules.

Taxation in the U.S. by comparison, is citizenship based and therefore, even if you are living in France, American citizens will always be obligated to the US and the IRS.

The deduction of income tax at the source of the earnings does not change this obligation in France. The declaration allows the administration to establish the situation of the tax household and to calculate the taxes due. The administration also checks if the taxpayer has to pay a balance of income tax in September 2022.

To file, you can submit a paper return or automatically online. The tax return is mandatory for all taxpayers. The period started on April 7th, 2022. Some taxpayers can benefit from an automatic return (paper or online) if their pre-filled return includes all the income and expenses of the household and if there is no change of situation in 2021 (except birth, adoption or reception of a minor child). In this case, the taxpayer must simply check the information indicated: marital status; family situation; salaries; allowances.

The schedule to file your tax declaration:

Type of return Deadline

– paper return May 19th

– online declaration for

departments from 01 to 19

and non-residents May 24th

– online declaration for

departments from 20 to 54 May 31st

– online declaration for

departments from

55 to 974/976 June 8th

In case of error, the taxpayer can send a second amended return before the deadline or modify his declaration on the Internet.

The “Wealth Tax” on real estate (IFI) is declared at the same time as the income tax, using the declaration annex n°2042-IFI.

The wealth tax is a tax on the real estate assets for individuals, which has replaced the solidarity wealth tax (ISF) since January 2018. It is due by taxpayers whose real estate assets exceed a limit of 1,300,000€. Real estate assets which had a net worth on January 1st less than this amount are therefore not subject to the IFI.

These assets include all property and real estate rights held directly or indirectly. The tax is calculated on the net value of the taxable assets as of January 1, 2022. The taxpayer must therefore make an estimated declaration of his assets (house, apartment, building land, buildings held indirectly via company shares, etc.). Certain debts are deductible, and the taxpayer can benefit, under certain conditions, from tax reductions.

In addition, certain assets are exempt from taxation:

• 30 percent deduction for the principal residence

total exemption for assets used for professional activities

• 75 percent exemption for woods, forests and shares of forestry groups if these assets qualify as professional assets, they are fully exempt from the IFI

• 75 percent exemption for long-term leased rural property and shares of agricultural land groups that cannot be qualified as professional assets up to a value of €101,987

• Beyond that, the exemption is 50 percent. The exemption is total if they are professional assets

Please note: The taxpayer also receives a pre-filled declaration if he paid the IFI in 2021. Online, the taxpayer obtains an immediate estimate of the amount of the 2022 IFI.

People who are tax resident in France are theoretically subject to the IFI on the basis of all their real estate (whether located in France or abroad).

Individuals who are tax resident abroad, are subject to the IFI on the basis of their property which is located in France.

People who return to France after having resided abroad for the past five years are, during the five years following their return, taxable for the IFI only on their property which is located in France.

A person living alone (single, widowed, divorced, separated) constitutes, in itself, as a full tax household.

Married couples form the same tax household and are therefore subject to common taxation on all of their property (sole property and common property), regardless of their matrimonial property regime.

However, there are two exceptions to the rule:

• When the spouses are married under the regime of separation and they live separately, each of the spouses shall be liable to the IFI but solely on their personal heritage

• When the spouses are in the midst of a legal separation or divorce, are authorized to live separately

The following are also subject to common taxation under the IFI on all of their assets (common or not):

• people in cohabitation

• people in civil union

It should be noted: property belonging to minor children is taxed, and therefore declared with the one of their parents, who have the statutory administration of their property. This can be divided equally between the two parents when the latter is subject to separate taxation, in terms of the IFI while exercising joint parental authority. On the other hand, the property belonging directly to adult children is not part of the taxable estate of their parents, even if the children have requested their incorporation to their parents’ tax household for the income statements.

Subject to exemptions, the taxable property in terms of the IFI is the property rights and values belonging to the tax household dated January 1, and mostly:

• built buildings (houses, apartments, etc.), and undeveloped buildings (land, agricultural land, etc.). It should be noted that the main residence benefits from a 30 percent reduction on its value

• investments related to real estate: SCPI, OPCI

• the fraction of the redemption value dated January 1, 2018 representative of taxable real estate assets included in accounting units of life insurance contracts

Those assets that are mostly exempted are:

• professional real estate, which means the required property for pursuit of the occupation which is the main activity of the taxpayer and of his spouse, civil union partner, cohabiting partner, and minor children: business, land agricultural, medical office, etc. Professional furnished rentals entitle you to this exemption

• up to 3/4 of their value, timber and forests as well as shares in forestry communities (on the other hand, shares in forest savings plans do not give right to an exemption)

Deductible liabilities are property debts payable by the taxpayer on January 1 of the taxation year, in particular:

• ongoing property loans (up to the amount of remaining due capital)

• debts related to the payment of improvement, construction, reconstruction or enlargement works.

• taxes which have not been paid yet on the basis of immovable property such as property tax. The housing tax is not deductible

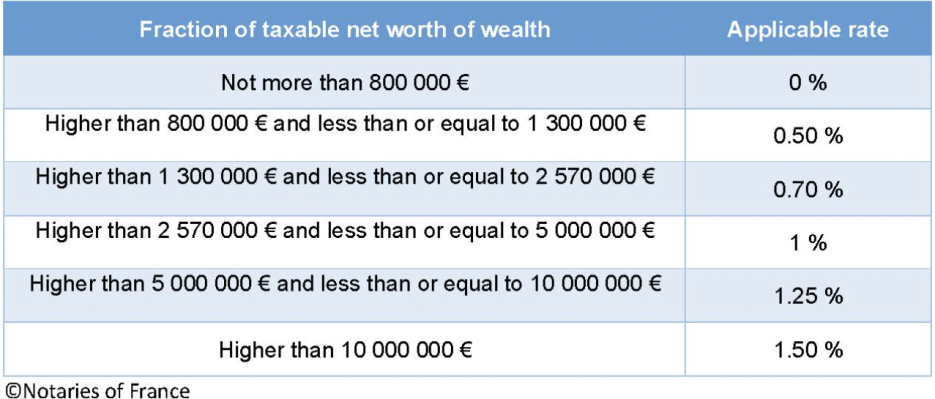

When the net value of taxable assets exceeds 1.3 million euros, the wealth tax (ISI) is calculated using a progressive schedule, which is the same as for the old solidarity wealth tax (ISF). It is made up of six tax brackets with rates ranging from 0 to 1.5 percent.

The schedule is the following :

As soon as the limit of 1.3 million€ has been exceeded, the calculation of the tax begins at 800,000€. For example, for real estate assets valued at 1.3 million euros, the IFI is also calculated on the brackets between 800,000 and 1.3 million euros, i.e. 500,000 euros at the rate of 0,5 percent.

A discount mechanism is implemented for assets whose net worth is between 1.3 and 1.4 million euros. Moreover, taxpayers of the IFI having their tax domicile in France, may benefit from an upper limit.

The amount of the IFI is then reduced by the difference between:

• the total of the IFI and taxes due in France and abroad on income and products for the previous year

• and 75 percent of total worldwide income net of professional expenses for the previous year but also the income exempt from income tax or subject to withholding tax carried out during the same year in France and outside France

The IFI must be declared at the same time as the income tax. On the other hand, if you do not have taxable income for income tax, you must complete the 2042-IFI-COV declaration.

In spite of having outlined much of the details of wealth tax here, I continue to recommend consulting with our professionals to minimize your tax, minimize your anxiety and maximize your enjoyment of life!

Visit our website to learn more about our recommended advisors.

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group

P.S. We have developed relationships with a number of financial and tax experts to assist our clients. For more information, please visit our Global Money Services page today!

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.