Weekly insights about property in France!

Subscribe and don't miss an issue!

Capital Gains Tax Reforms? Not likely!

Volume XXI, Issue 41

Now is not a good time to sell in France because the market is down across the board (except for Nice!). However, news from the French tax authorities is that the finance bill for 2024 could include a new measure in favor of owners of second homes…all thanks to the downturn in the real estate market!

In an attempt to revitalize the real estate market, member of Parliament, Daniel Labaronne, proposed to make the capital gains made on the sales of second homes in 2024 exempt from social security contributions and taxes.

The authorities don’t think that this proposal has much chance of succeeding. Some will even say, there’s no chance of success at all. However, the trend could even be the opposite—for higher taxation of real estate capital gains relating to second homes! We certainly hope not!

“I propose that in 2024, the capital gain realized on the sale of a second home should be totally exempt from tax and social security deductions,” he said. “On condition that the second home is converted into a principal residence or is offered for rent.”

I remember when the law reduced the taxation to zero over the course of 15 years of ownership. And at the same time, short-term rental was “de rigueur” (fashionable), mortgages were easy to obtain and foreigners (Americans) were buying easy-peasy. Then, things changed with the 2012 Finance Act which assesses capital gains taxes on ownership of up to 22 years and another contribution for social security for a remaining 8 years.

The outlines of the finance bill for 2024 were clarified by Bruno Le Maire at the Council of Ministers on September 27, 2023. The proposal requires that the second home being transferred becomes either a main residence or a second home rented out. The capital gains you acquire on the sale of a property is subject to income tax, unless it’s your principal residence. You may benefit from exemptions depending on the nature of the property or your personal situation.

Second homes are a concern in many smaller towns, as they become “dormitories” in winter and overcrowded in summer. Would this measure change the situation? Probably not, since that’s not the problem. These communes are not sufficiently attractive for all second homes to be rented out. The rental market is so thin and so unprofitable that few investors will take up these financial gambles.

FROM THE NOTAIRES DE FRANCE WEBSITE:

The real estate capital gain is equal to the difference between the sale price and the purchase price or the declared value, when the property has been received by donation or inheritance.

The capital gain is equal to the difference between the sale price (minus the transfer costs and the amount of VAT paid) and the purchase price (mainly the registration costs paid during the purchase or 7.5% of the purchase price) or the declared value when the property was received through a donation or inheritance (plus actual costs and transfer rights, free of charge, if these were borne by the “donee” or the heir).

Paris

The purchase price may be increased due to construction, reconstruction, extension or improvement expenses, as soon as these have been borne by the seller and carried out by a company, who shall be subject to presenting the supporting documents (invoices concerning VAT. Note: the materials and works carried out by the owner himself are no longer deductible). Moreover, these must not have already been taken into account, in order to determine the income tax (mainly deduction for property tax revenue) and these must not be rental costs (CGI, art. 150 VB II, 4°).

The works taken into account to determine the real estate capital gains, are defined in the same way as those taken into account for determining taxable property income.*

Solely the incurred costs since the completion of the building or its acquisition, if it is later can be taken into account, in addition to the purchase price.

Strasbourg

In all cases, maintenance, and repair expenses, including major repairs, are not included among the expenses that can be taken into account, in order to calculate the capital gain. These concern works which are intended to maintain or restore a building, in proper condition and allow normal use.

Expenses in addition to the purchase price must be justified (CGI, art. 150 VB II). However, the documents justifying works are only provided at the request of the administration (CGI, ann. II, art. 74 SI). (*Note that the tax authorities will not recognize decorative improvements to the property, but only serious home improvements, such as a new bathroom or kitchen that didn’t once exist!)

Alternatively, the seller may increase the purchase value by 15%, if he has owned it for more than 5 years, on a flat-rate basis, without having to establish the reality of works, the amount of works genuinely carried out or his inability to provide supporting documents (CGI, art. 150 VB II, 4°). There is no need to check, if the work expenses have already been taken into account for the income tax base. The 15% flat rate is a simple option for taxpayers, who have owned their property for more than five years. It does not add up to the costs, which are borne by the owner.

Nice

If many works have been carried out in the second home, the notary will advise to keep all the invoices because the purchase price may be subject to an increase in the amount of the actual expenditure of the works, for which the invoices have been retained. Otherwise, only the standard increase of 15% shall be applied without proof if the property has been held for at least five years.

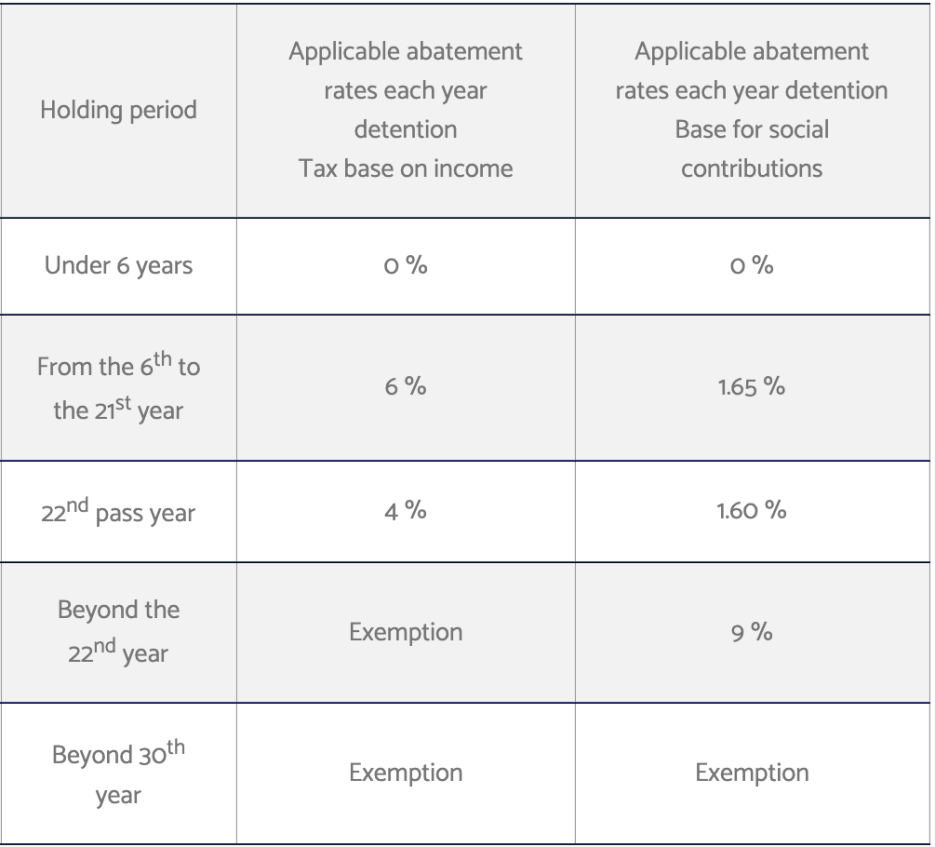

The rate and reduction rate for the detention duration are different, in order to determine the taxable base for income tax and social security contributions.

Thus, the real-estate capital gain is exempted:

• after 22 years of income tax detention

• after 30 years of detention for social security contributions.

The years of detention are counted from the anniversary of the property purchase (date of purchase, date of donation or date of death)

In accordance with the provisions of II article 28 of the law n °2017-1775 dated December 28, 2017 of amending finance for 2017, an exceptional reduction applies, under conditions and temporarily, in order to determine the net taxable capital gain, both for income tax and social security contributions, resulting from the sale of building land or built real estate, or related rights.

Lille

Therefore, the capital gains resulting from the sale of building land or built buildings intended to be demolished, towards a reconstruction of one or more collective housing buildings, located in geographic areas characterized by a peculiar imbalance between the demand and supply for housing, are determined after applying an exceptional reduction of 70% or 85%, on the dual condition that the sale:

– is either preceded by a unilateral or synallagmatic sale agreement and has acquired a firm date from January 1, 2018 and no later than December 31, 2020.

– be carried out at the latest on December 31 of the second year following the year in which the unilateral or synallagmatic* sale agreement acquired a firm date. Theoretically, the exceptional reduction may therefore apply to transfers, carried out until December 31, 2022.

* In civil law systems, a synallagmatic contract is a contract in which each party to the contract is bound to provide something to the other party.

The capital gain is taxed under income tax at the current flat rate of 19% (with a linear reduction of 6% from the 6th year) and under social security contributions at the current rate of 17.2 % (with a progressive reduction 6th year onward). The amount of the tax shall be deducted by the notary from the sale price, while signing the authentic act and paid by the latter to the tax authorities.

An additional tax (from 2 to 6% depending on the amount of the capital gain after applying the reduction) applies to capital gains on property, other than on building land of an amount higher than 50,000€ . The capital gains resulting from transfers carried out since January 1, 2013 are concerned.

One can collect a municipal tax during a sale of a land, which is now approved as a building land (CGI Art. 1529) and/or a national tax (CGI Art. 1605 ch).

Aix-en-Provence

The capital gain regime varies depending on the sale price, the nature of the property, and the ownership duration. Given the concept of taxation, there are cases of limited exemptions.

If you are a non-resident and realize a capital gain directly or indirectly :

• on the sale or transfer for valuable consideration of a property located in France

• or on the sale or transfer for consideration of shares in a company whose assets consist mainly of real estate located in France.

In these cases, your capital gain will be subject to 19% tax, regardless of your country of residence. It will also be subject to social security contributions at the overall rate of 17.2%. Since the taxation of property income received in 2018 and capital gains on property made since 1 January 2019, persons affiliated to a compulsory social security scheme, other than French, in an EEA country (European Union, Iceland, Norway, Liechtenstein) or Switzerland, are exempt from the general social contribution (CSG) and the contribution to the reimbursement of the social debt (CRDS).

Note, that this exemption is not done automatically and one must make a special claim for reimbursement!

Here’s how to calculate your capital gains tax.

Special note: if you move to France and live in that property you purchased before becoming resident in France, then if and when you sell, the property would be declared as a primary residence and you will pay no capital gains! This is yet another reason to make France your permanent home!

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. Now’s the time to schedule a consultation to discuss the possibilities of an investment in Paris (or elsewhere in France) or if you’re looking to sell your property. For more information, contact us.

1 Comment

Leave a Comment

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.

Loving your Nouvellettres! Just finished reading your post on A/Cs. As I currently live in Florida, the A/C is a MUST! Looking at Nice and while it too gets warm, I look forward to the coolness of Mediterranean. Look forward to our consultation next month!