Weekly insights about property in France!

Subscribe and don't miss an issue!

What Does a French Property Cost to Own and Operate?

Volume XXI, Issue 50

One of the best aspects of owning French property is the minimal “carrying costs,” especially if it’s a multi-family dwelling with shared operational costs. Compared to the U.S., the costs are so much lower that even if you’re not generating rental income, or much of it, ownership won’t be too big a burden.

These are the expenses you will incur to own and operate the property which include mortgage payments (if applicable), annual taxes, utilities, homeowner association dues (if in a multi-family building), insurance and then lastly, what you can anticipate for regular maintenance.

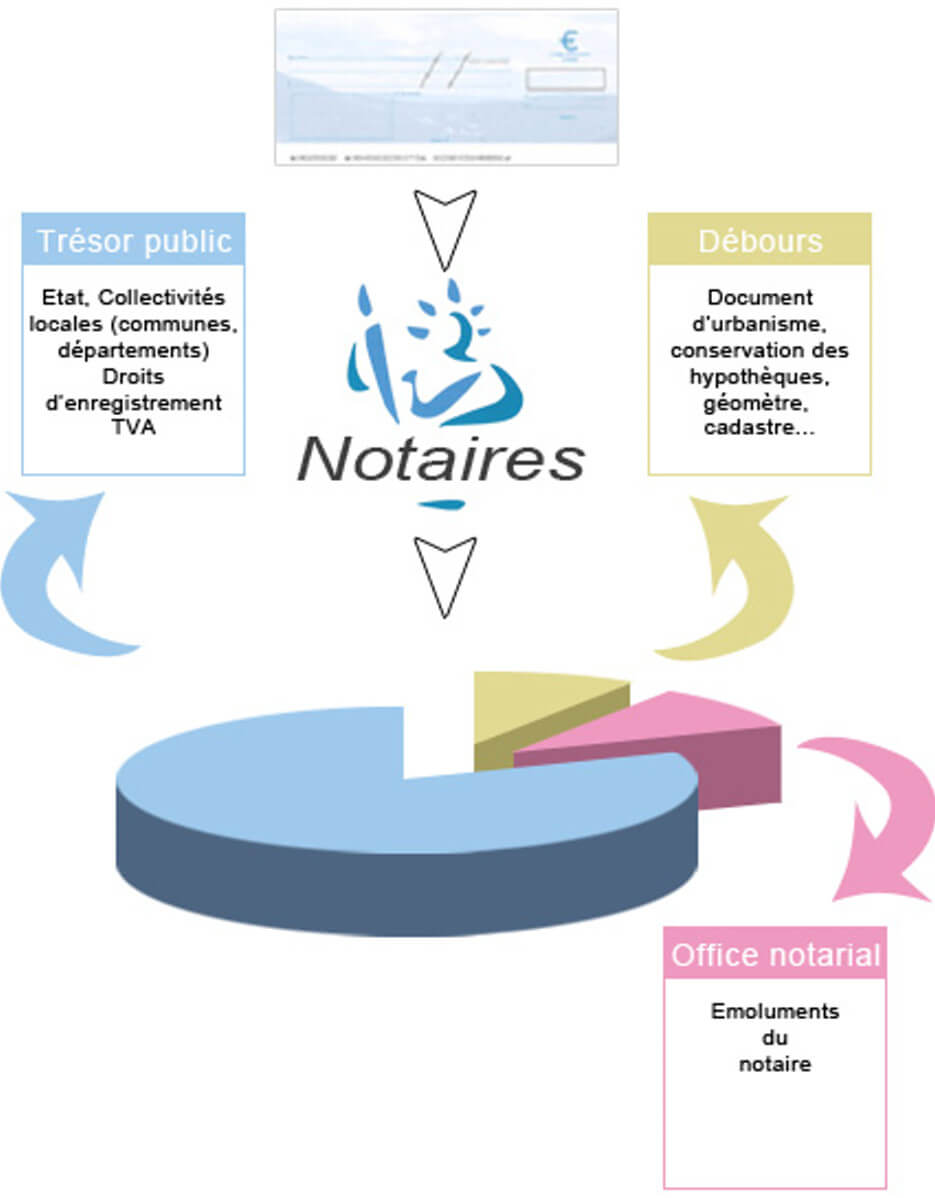

NOTARIAL TAXES AND FEES

Before that, however, there are the closing costs—the Notarial taxes and fees that add to the investment before you even begin to renovate or furnish it—incurred at the time of closing. Calculated according to the value of the property, their amounts vary depending on the property’s geographic location and are paid by the buyer upon the closing or final sale of the property. The French Notaires are responsible for collecting them on behalf of the state and to remit them to the Public Treasury.

The taxes amount to about 8/10ths of the total fees. Disbursements amount to about 1/10th of fees—fees paid by the Notaire on behalf of its client and used to compensate the various parties and/or pay the cost of the various documents, but also to settle the exceptional costs incurred at the client’s request (e.g. certain traveling costs). The fees are split if another Notaire represents the other party.

The bottom line is between seven and eight percent of the net price of the property will be assessed for the Notarial taxes and fees. There is nothing you can do to negotiate these fees as they are highly regulated. This is a one-time cost and therefore you can consider it a cost of your investment.

For a very detailed look, visit this page on the notaire’s site. And/or this link. To estimate the fees on a particular property, visit this page on their site.

And here’s a video on Youtube you can watch that explains it all!

YOUR MORTGAGE

Now that you’ve paid the Notarial taxes and fees and own the property, the carrying costs are ongoing for the life of the property, or in the case of the mortgage, until the principal and interest is fully paid based on the term of the loan. When calculating this expense, keep in mind that your carrying costs are not the principal payment, as that counts toward the price of the property, but the interest and other costs are, such as life insurance, associated with the mortgage. Also, keep in mind that there are tax advantages associated with the interest, as currently, the home mortgage interest deduction in the U.S. (HMID) allows itemizing homeowners to deduct mortgage interest paid on up to $750,000 worth of principal, on either their first or second residence. This limitation was introduced by the Tax Cuts and Jobs Act (TCJA) and will revert to $1 million after 2025.

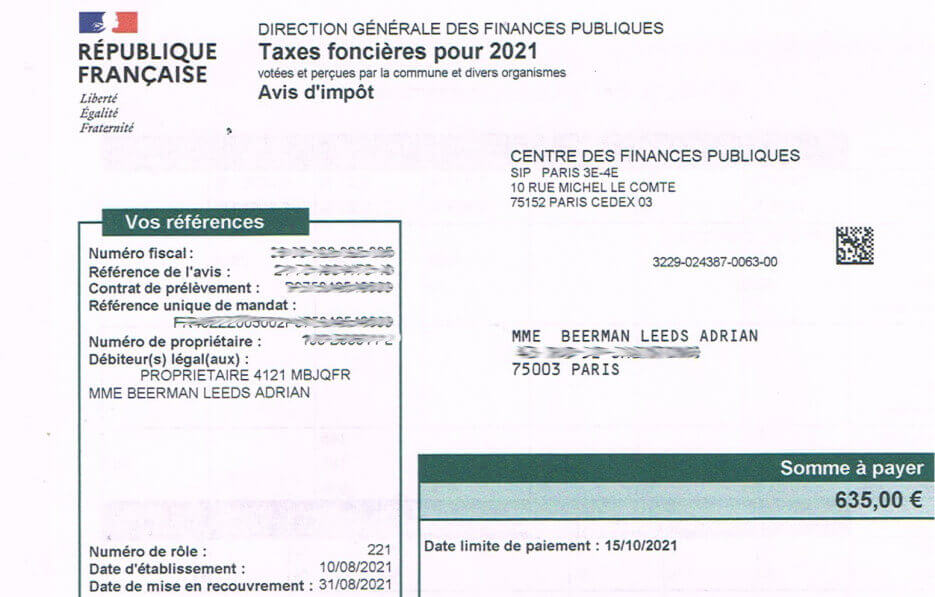

TAXES: TAXE D’HABITATION + TAXE FONCIERE + REDEVANCE AUDIOVISUELLE

One of the most surprising aspects of property ownership in France is the low property taxes assessed annually on homeowners, considering that France is well-known to be a highly taxed society. On the whole, I find that property taxes are about 1/10th of what they are in the U.S.! This is not a fact by which I can stand, but over the years, when asking our clients what they pay in property taxes in the States, more often than not, it’s about 10 times what they will experience in France.

There are two taxes assessed annually are “Taxe Foncière” and “Taxe d’Habitation.”

The property tax, known as Taxe Foncière, is consistently borne by either the owner or usufructuary. The usufructuary is an individual who enjoys the right to use a property and receive rental income from it, yet lacks the authority to dispose of it, especially concerning the sale of developed properties. Property tax, specifically the Taxe Foncière sur les Propriétés Bâties (TFPB), must be settled for developed properties. Various exemptions are tied to either the property itself or the owner. Here’s a concise overview of key details you should be aware of.

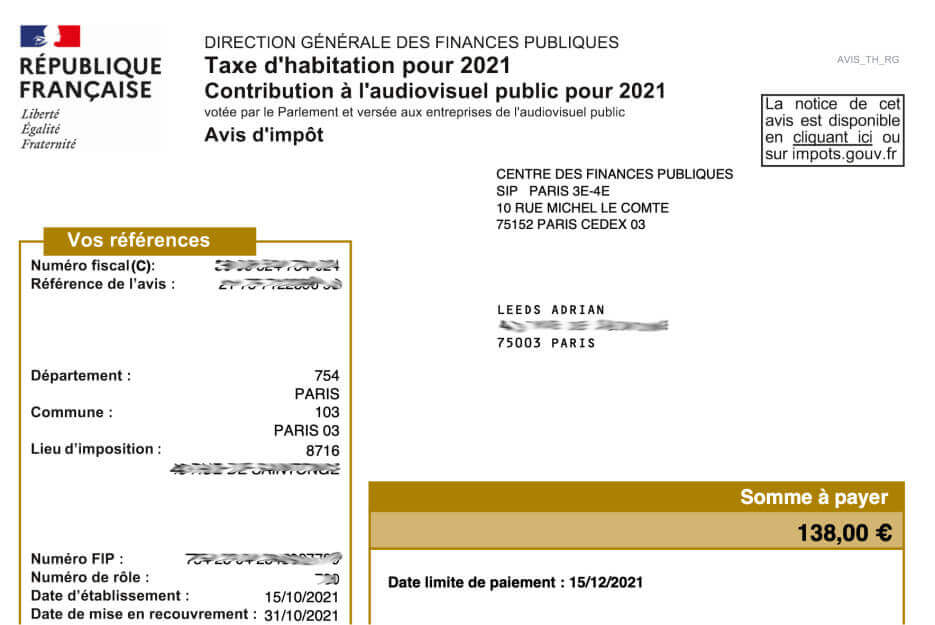

From January 1, 2023, all taxpayers no longer have to pay Taxe d’Habitation (Council Tax) on their primary residence. However, it continues to apply to second homes. Owners also have a new reporting obligation. You can benefit from an exemption from council tax if you leave your main residence to move into a specialized facility (long-term care center or retirement home). In this case, you may be exempt from the “Taxe d’Habitation sur les Résidences Secondaires” (council tax on second homes) for your former home.

Don’t start worrying about the tax on January 1st! You will receive a tax notice in the last quarter of the year, which can also be consulted on the “Espace Particulier” section of the tax website. So, you have at least nine or 10 months before it must be paid. If you own more than one dwelling, you will receive a tax notice for each of your premises.

This is a tax levied for the benefit of local authorities and therefore the amount varies from one commune to another. The tax rate is set by the local authorities and is levied for the whole year, according to your situation on January 1st of that tax year. It is calculated on the basis of the cadastral value of the dwelling and its outbuildings, applying the rates voted by the local authorities. The cadastral rental value is revalued every year in line with changes in the consumer index.

Yes, I know that’s a mouthful and why it’s pretty tough to determine the tax on your own. To understand this in greater detail, visit this site (in French).

The “Redevance Audiovisuelle” for TV ownership in France is an antiquated tax that simply and finally went away as of 2022! Yeah!

UTILITIES: ELECTRICITY + GAS + WATER + INTERNET/PHONE/TV

You’ll find utility costs low in France…surprisingly. While the U.S. became a consumer society, Europe was watching its usage and therefore its pennies, focused always on saving energy in every way possible. You likely have already noticed this when the light in the hallways stays on for only a brief amount of time rather than burning continuously, or when using appliances that have economic/ecological settings.

Electricity

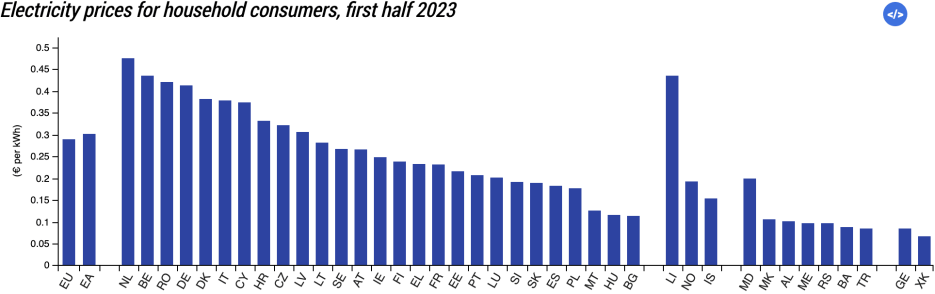

France holds the position of being the second-largest electricity producer in Europe and ranks tenth globally in electricity production. Renowned as a global leader in nuclear energy, France demonstrates a strong commitment to low-carbon sources. Notably, the annual electricity production in France consistently exceeds its consumption by a substantial margin, ranging between 50 and 100 terawatt-hours. Consequently, the country stands out as a significant exporter of electricity to other European nations, with export volumes nearly doubling the amount of electricity it imports, a trend observed as of 2021.

In 2023, 70 percent of the French population had an electricity contract with EDF, opting for its Tarif Bleu, which is the regulated sale tariff for electricity. Assuming that the majority chose the base meter option (with a consistent electricity price throughout the day) and an average meter power of 6 kVA, the average cost per kWh in France is estimated at 0.2062€, with an annual subscription charge of 143.87€. Considering the average household electricity consumption in France was around 4770 kWh in 2019, the annual electricity expenses ranged from 858.64€ to 898.02€, depending on the chosen provider and plan. This translates to an average monthly electricity bill of approximately 79€.

When making a property purchase, you can ask to see the seller’s electricity bills to determine what you can expect for the property in the future.

Gas

If you’re lucky enough to have gas in your home or apartment, then you have the possibility of having continuous hot water (no water tank) and heat via a “chaudière” or boiler that heats the water as its run through it. It also affords you the luxury of a stove with gas burners, if you prefer that kind of cooking. About one-third of all households in France use natural gas for heating, hot water and/or cooking, although this is diminishing.

A French “chaudière”

Unlike the electricity expense in France, the average gas bill is contingent not only on the amount of gas consumed by your household (consumption class) but also on your municipality (tariff zone). Certain locations are more easily served with natural gas, influencing transport costs and, consequently, the gas price. Similar to electricity, households supplied with natural gas can decrease their gas bills by selecting a supplier with more competitive gas rates. Competitive suppliers frequently provide rates lower than the regulated tariffs.

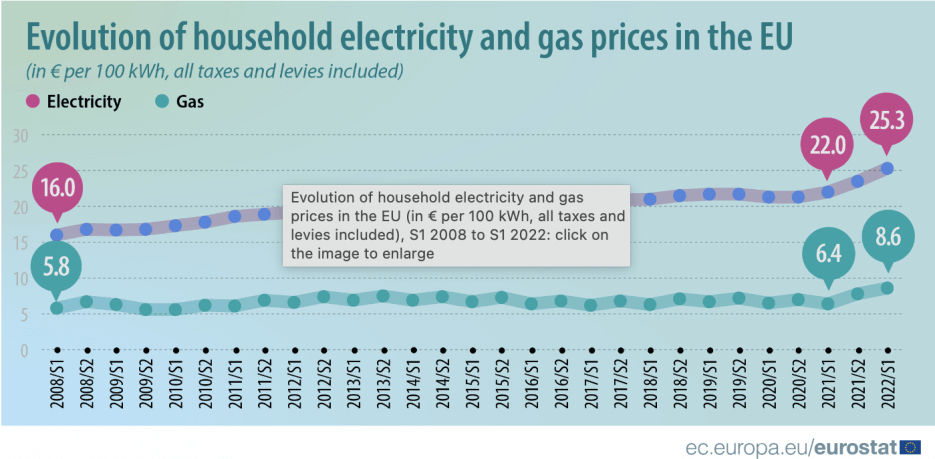

A tariff shield that was put in place in 2021, and already extended to December 2022 for gas, and to February 1st 2023 for electricity, was renewed in 2023. The rate increase was limited to 15 percent from January 1st, 2023 for gas, and also 15 percent for electricity as of February 1st, 2023. There is no catch-up announced for 2024 to be borne by households; the shortfall for energy producers having to be borne by the State. In addition, aid of up to 200€ is also provided for French people heating with fuel oil or wood.

Water

Water in France is supplied by a number of private companies, the largest of which are the Saur Group (part of Bouygues), which also supplies mobile phone services, Suez Environment (formerly Lyonnaise-des-Eaux), and Veolia Environment (part of Vivendi), who between them supply some three-quarters of the water in France. The water supply infrastructure, however, is owned and managed by local communes, so rates vary across the country. Most properties in France are metered, so that you pay only for the water you use and are charged per cubic meter (1,000 liters).

You’re billed by your local water company annually or every six months and can pay by direct debit. If you own an apartment in a condominium, the water bill for the whole building is usually divided among the apartments according to their size as are the other maintenance charges. In some situations, there will be a separate meter per apartment so that you will be responsible only for your own usage and not more.

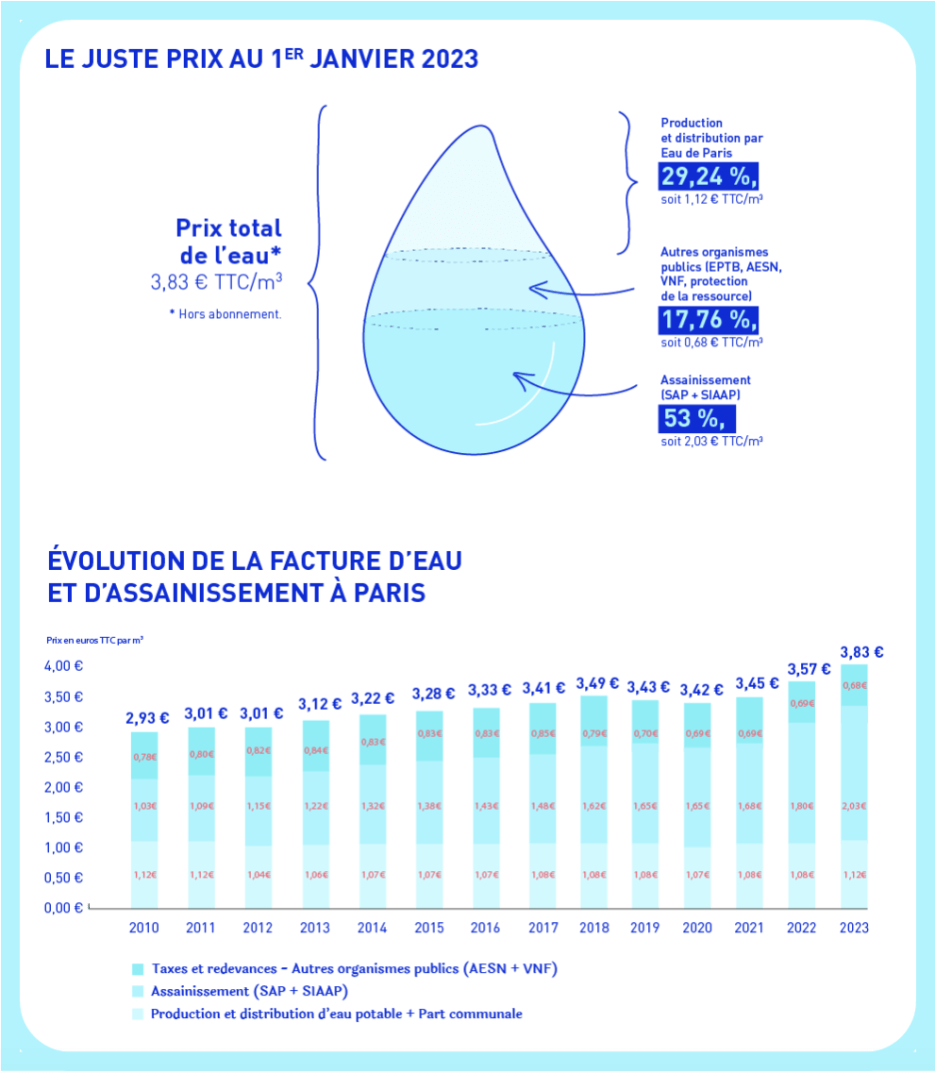

The price of water in Paris is one of the lowest in Île-de-France! For all types of daily use, Paris water costs less than 0,004 euros per liter. At January 1st, 2023, the total price per cubic meter of water amounts to 3.83€/m3, VAT included excluding a subscription. Despite the evolution of prices, water in Paris remains the cheapest in the metropolis. The daily water expenditure for a family of four in Paris is approximately 1.8€. The calculation is very advantageous for drinking water: a Parisian who drinks 1.5 liters of Parisian water per day spends only 2€ per year!

Internet/TV/Phone

There are several companies in France that offer a “triple play” package that includes high-speed Internet, a Voice-Over IP phone and satellite TV with hundreds of channels. The main players dominating the market are Orange, SFR, Bouygues Telecom, and Free. Free is the second-largest ISP in France and claims to have invented the box concept when they released the “triple play” modems long before any of the others who had no choice, but to follow suit.

This is one of the biggest savings of all compared to life in the U.S. Their offerings start at 9.99€ a month! And you can add a cell phone for as little as 2€ a month! You can get 5G service with unlimited calls and text messages to almost anywhere in the world at these rates. For the purpose of budgeting, allow about 40€ a month for a complete package + a cell phone at 20€ a month. Can you imagine? How much do those services cost where you live?

Note: When using a Free mobile phone with an unlimited usage plan to over 100 countries, it will be free to use within those countries with free calls back to France! When I travel within Europe and to the U.S. or Canada, I never need anything but my Free mobile phone to make calls, send text messages or even have internet via a Personal Hotspot for not a penny more! I’ll bet when you travel to France with your U.S. cell phone, it can be very expensive!

HOMEOWNER ASSOCIATION DUES

If your property is located in a multi-family building (condominium), you will pay what is known as “les charges”—or annual maintenance fees. The co-ownership charges correspond to all the costs generated for the operation and maintenance of a group of owners.

The calculation of the distribution of the payment of charges between the co-owners is defined in the co-ownership regulations, the share corresponding to the size of each lot of the co-ownership. The co-owners appoint a representative, the “syndic” (manager) of co-ownership, to manage the maintenance and the proper functioning of the building.

The general charges represent all the expenses incurred for maintenance (resurfacing, structural work, painting, etc.), conservation (cleaning, security, lighting, etc.) and administration of the common areas (fees of the syndic, general meeting fees, etc.). The special charges include all the costs generated by collective equipment and services such as water, collective central heating, elevator charges, garbage chutes, etc. For example, someone who lives on the ground floor (and who does not have a garage or cellar in the basement) will not pay any maintenance and repair charges for the elevator. The payment of these costs will also be made in proportion to the residential floor. Those who live the highest will pay the most.

On average, the co-owner of a 60 m2 apartment paid 3,000€ in charges (fees) per year (250€ a month), according to news site L’Obs. If you figure 50€ per square meter per year, your guesstimate will be close, but again, when purchasing a property, you can ask to see the syndic invoices to determine your annual costs.

HOMEOWNER INSURANCE

In most situations, you will want to cover all risks with comprehensive insurance called MRH (Multi-Risque Habitation) under French law. It covers all material damages (theft, fire, explosion, water damage, glass damage…) and it includes civil liability for all the people living in the insured home. There are the usual suspects in the insurance business in France such as AXA and Allianz, as well as the various brokers, but most of the banks also provide this service. They have either created their own subsidiary insurance companies or signed an agreement with an insurer to offer insurance to their clients: Pacifica/Credit Agricole, Banque Populaire/Maif, Société Générale/CGU and Credit Lyonais/Allianz.

The average annual cost of a home insurance premium to insure a house in the Île-de-France region was about 447€, compared to 240€ for an apartment. Meanwhile, it cost 531€ for a house and 369€ for an apartment on Corsica.

For our recommended insurance providers, visit our website.

MAINTENANCE

Everything listed above is what you can expect on a monthly or annual basis, but what about the extra maintenance that occur along the way, such as a plumbing mishap or a refreshment of the paint? Don’t forget to budget for these unexpected costs. There are a few ways of planning for these expenses. One is to simply take a percentage of the price of the property, such as a quarter of one percent, to set aside so that when you have to replace that old faucet, you’ll be ready.

Another and more realistic way is also much more complicated, but is something we use to create a “reserve fund” assessed for future maintenance. Create a spreadsheet detailing the current value of each item in the property, determine an estimated lifespan for that item, then estimate its replacement value multiplied by the inflation rate for each year of its life. Yes, I told you it was complicated, but it will give you a very realistic idea of how much money you should set aside for such situations.

You will also have building assessments to consider, such as the “ravalement” or resurfacing of the building which can be done as much as every 10 years. And if your building needs to repaint the stairwell, you’ll find yourself with additional costs—however, these assessments must be voted by the co-ownership so at least you should be a part of that decision and therefore forewarned and therefore forearmed.

Be forewarned: regular maintenance and upkeep of a single-family residence will cost quite a bit more than an apartment in a shared multi-family dwelling.

THE BOTTOM LINE

The bottom line is that the carrying costs in France are considerably lower than you’d likely expect or that you are likely paying now in your home country, especially the taxes! And the good thing is that there will be no real surprises as you should be fully aware of the estimated future costs before ever signing the deed on your new French property.

A bientôt and a very happy new year!

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. Believe it or not, February 13, 2003 was our first issue of French Property Insider…so for more than 20 years we’ve been promising and producing 50 issues a year! If you like reading FPI, then perhaps your friends will, too, so don’t hesitate to pass it on. Here’s where you can subscribe!

1 Comment

Leave a Comment

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.

Very informative!

However, I think doing away with the “redevance” was a dreadful mistake and a false economy for residents.

<>

The fee helped make France’s enviable network of non-subscription television and, especially, national network of outstanding state-funded radio stations possible. It paid for investigative reporting, royalties to musicians, maintenance and maintaining the excellent regional outposts of the main French broadcast system.

In the U.S., the GOP is forever trying to get rid of the tiny contribution Americans make to public broadcasting. I believe it’s in the vicinity of a dollar a person, but even that amount rankles people who think “the market” should pay for everything (or that NPR and Public Broadcasting simply should not exist in the first place.)

In exchange for roughly $150 per household, per year, people all over France (or internet listeners and podcast fans all over the world) could be sure to have access to excellent audiovisual programs. The trade-off of having that “extra” $150 a year in your pocket is a poor one.

The notion of public service reamins strong but the funding has been dealt an enormous blow.

Thanks to the annual license fee, France, until recently, did a fine job of keeping advertising to a minimum. THAT is better for children and for consumers in general. Now the missing funds have to be made up somehow — either by getting rid of staff and cutting back on programs or seeking out additional advertising. Not progress in my book.

I gladly paid the redevance even when money was tight because I listen to French radio so much. Try France-Inter or France Culture or FIP if you want to sample the quality of public radio.

Lisa Nesselson