Weekly insights about property in France!

Subscribe and don't miss an issue!

Declare Your Secondary Residence + Get Ready for Higher Lending Rates

Volume XXI, Issue 4

The newest bit of French bureaucracy we must face is a mandatory declaration to be made on the official government tax website in regard to the annual “taxe d’habitation.” While the taxe d’habitation has been abolished for primary residences, 34 million owners must still declare their situation…now online.

YOUR DEADLINE IS JUNE 30TH TO DECLARE YOUR HOUSING SITUATION

The housing tax has been abolished for primary residences. However, it has not completely disappeared, and remains due for second homes. Therefore, in order to determine exactly who will still pay this tax, the Direction Générale des Finances Publiques (DGFP) is asking all homeowners, whether they have a primary or secondary residence, to make an additional declaration to the tax authorities. In fact, 34 million owners are concerned, confirmed Le Portail Internet de la Gestion Publique (DGFiP).

Here is how to take care of this formality:

For each of their premises, whether vacant or not, owners will have to go to this website, under the heading “Mes biens immobiliers” (“My real estate”), to fill out a “declaration of occupancy.” The idea is to indicate who lives in the home or uses the second home or the premises in question and their period of occupancy. Taxpayers have until June 30th to do this. Once the declaration is made for the first time, only a change of the situation will require a new one to be done.

Note that we are talking only about residential premises. A parking lot or commercial premises, for example, is not concerned.

The objective is simply “to identify the premises that remain taxable,” now that the housing tax is no longer in force on primary residences, but still on secondary residences and vacant housing, as explained by the Ministry of the Economy. Seventy-three million premises are concerned, according to the General Directorate of Public Finance.

The site is available in English—that’s the good news!

THE RATES ARE ON THE RISE

It seems that every day we get news from the lending market, which isn’t always very optimistic for our clients. The latest is that the real estate credit and usury rate will change as of February 1st, 2023 as was expected. The calculation formula of the usury rate will be applied every month instead of every quarter, which should facilitate (a little) access to credit for private individuals. That’s at least a good thing.

The usury rate caps all the costs of a real estate loan: the credit rate charged by the bank, possible broker’s commission, and borrower’s insurance. The way it is calculated has been an obstacle for many buyers for several months now. Interest rates have been rising in the wake of the key rates of the European Central Bank, and faster than this usury rate.

Raising the usury rate ceiling can thus provide a breath of fresh air to the market: it allows banks to lend more expensively, but also allows each other component of the cost of credit to be taken into account without exceeding the legal ceiling.

This allows, on paper at least, ultimately the acceptance of more credit application files. But, the formula for calculating the usury rate, defined by law, does not change: an average of the rates charged by the banks over the last three months, increased by a third.

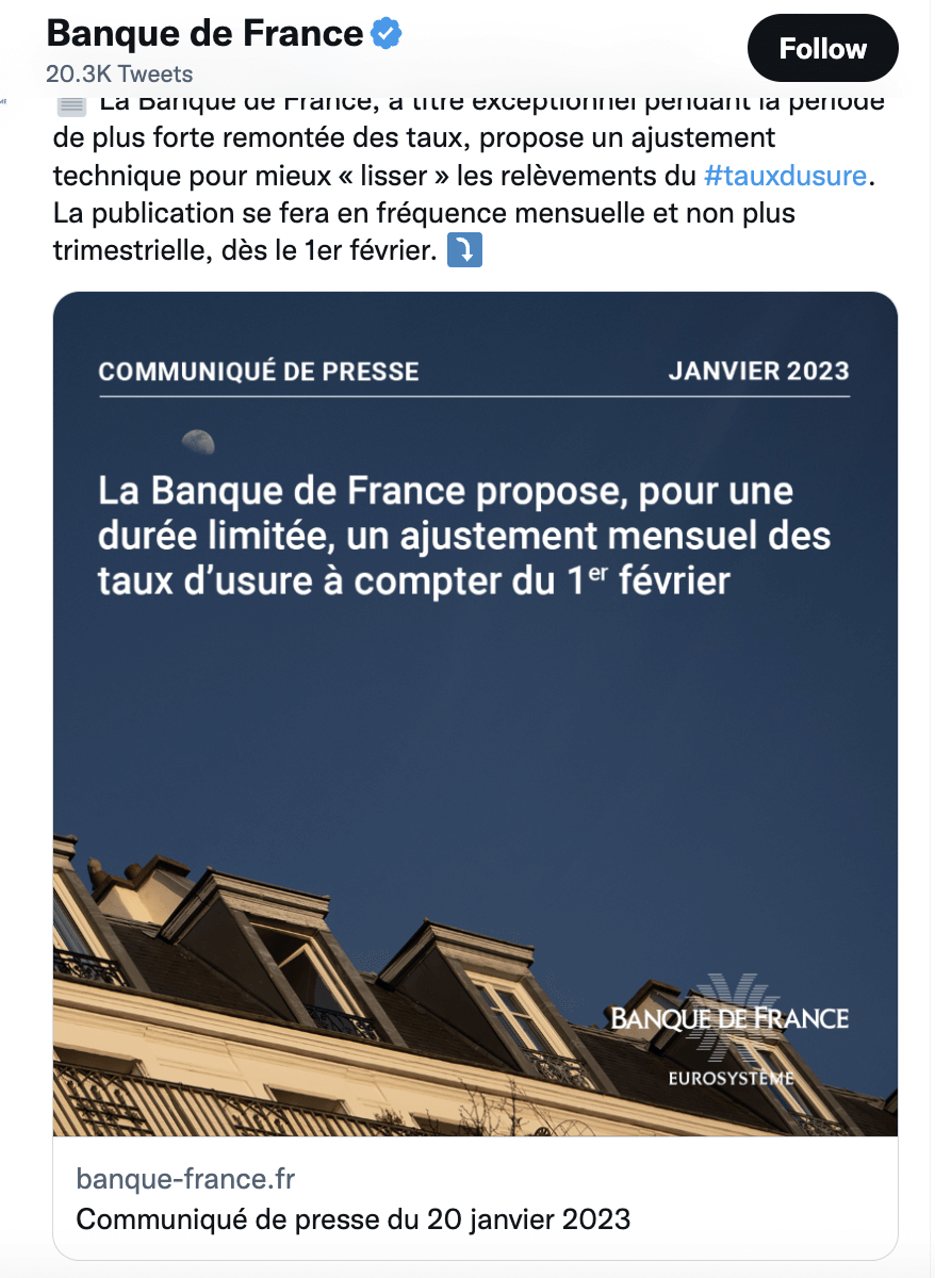

The Banque de France, on an exceptional basis during this period of the highest rise in rates, proposes a technical adjustment to better “smooth out” increases in the usury rate. The publication of the rates will be monthly and no longer quarterly of all categories from February 1, 2023 for the rates applicable from February 1 to July 1. The usury rates will remain established on the basis of the average of the rates practiced during the three previous months.

The Banque de France had noticed in recent months that at the end of the quarter “certain files, pending the next significant quarterly increase in the usury rate,” were postponed to the start of the following quarter, creating an imbalance in the distribution credits. The idea of this monthly increase had been studied at a meeting held at the Banque de France last week which had brought together brokers, bankers and the services of Bercy.

The Governor of the Banque de France, François Villeroy de Galhau, had himself mentioned before the Senate Finance Committee that there was a need for “a technical adjustment,” recalling in passing that “the usury rate is intended to protect borrowers against abnormally high rates.” No bank can lend you beyond this level of usury rate. Since January 1, it is, for example, 3.57% for a loan taken out over 20 years or more (insurance and miscellaneous costs included, therefore).

With high real estate prices and rapidly rising rates, it is also the level of buyers’ indebtedness that is worrying. The rates charged on average in December were estimated at 2.34% by the CSA Housing Credit Observatory, and they continue to climb. This monthly update of the usury rate should not completely unblock the credit market. Faced with the sustained rise in the cost of existing housing (+ 4.2% in 2022 and + 14.5% between 2019 and 2022) and the increase in interest rates, the ability of households to buy has been affected in the latter months, insists the CSA Housing Credit Observatory.

In 2022, the number of loans granted fell by 20.5% compared to the previous year. The purchasable area fell by 4.5 m² for the whole of France. The average duration reached a new unprecedented level: 20.7 years in December (248 months), whereas it was 13.6 years in 2001 (163 months). An extension that is no longer sufficient to compensate for the consequences of the rise in housing prices or to cushion the effects of the increase in the required personal contribution rates, underlines the Observatory.

All this means that we can bank on rates rising in France, but we can hope that by capping the usury rates, there is a chance that we’ll see the banks be more willing to lend and maybe even more willing to lend to foreign buyers.

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. We have developed relationships with a number of financial and tax experts to assist our clients. For more information, please visit our Global Money Services page today.

2 Comments

Leave a Comment

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.

Thanks a lot Adrian! My husband is about to take care of it but it’s such a maze. Your Nouvellettre is arriving just ont time and full of practicals. Take care Eileen and Adam.

Good luck!