Weekly insights about property in France!

Subscribe and don't miss an issue!

Financing the Dream in France in 2026

Volume XXIV, Issue 10

By Jay Corless, edited by Adrian Leeds

If you’ve been sitting on the sidelines waiting for a sign that financing in France is becoming a little more workable, there is some encouraging news. Not because borrowing has suddenly become easy—this is still France, after all—but because the rules are a bit clearer, a few targeted incentives have been expanded, and the market feels more structured than it did during the interest-rate shock of the last two years.

The most important thing to understand is that French mortgage lending remains tightly regulated. The “Haut Conseil de stabilité financière” (HCSF), which sets the guardrails for residential lending, continues to cap a borrower’s debt burden at 35% of income. That includes the total cost of repayment, and the standard maximum loan term remains 25 years, with limited room for a short deferred period in certain cases. In other words, banks may be lending more willingly again, but they are still doing so inside a firm framework.

That said, the framework is not completely rigid. Banks are allowed to exceed those criteria for up to 20% of the home loans they issue each quarter. Most of that flexibility must still be directed toward principal-residence buyers, and a meaningful share toward first-time buyers. So this is not a free-for-all, but it does mean that well-prepared borrowers with strong documentation and a coherent project may find a little more room to negotiate than before. In France, that can make all the difference.

One of the most notable changes is the broader reach of the “Prêt à Taux Zéro” (Zero Interest Loan), or “PTZ.” Since April 1, 2025, the PTZ has been expanded so eligible buyers can use it for the purchase of a new home anywhere in France, including both apartments and detached houses. The measure is set to run through December 31, 2027. Depending on income and the type of property, the PTZ can cover a meaningful portion of the purchase price, up to 50% in some cases for new apartments.

That sounds exciting, and it is, but only if you fit the profile. The PTZ is meant to help finance a future principal residence. It is not for a second home, not for a pied-à-terre, and not for a classic investment purchase. It must also be combined with another loan rather than used on its own. So if you are relocating to France full time, or helping a child buy their main home here, the PTZ may be very relevant. But for many international buyers looking for a lifestyle purchase, the headline may be more appealing than the actual benefit.

There are also conditions tied to the program. The PTZ is generally reserved for first-time buyers, meaning those who have not owned their principal residence in the previous two years, subject to certain exceptions. There are also income ceilings. Once again, the logic is very French: support access to owner-occupation, but do so selectively and with careful targeting.

Another under-the-radar measure that could be quite useful is the temporary tax-free family gift regime linked to housing. For qualifying sums paid between February 15, 2025 and December 31, 2026, certain family members may make exempt cash donations to help fund the purchase of a home or qualifying energy-renovation work. The exemption can be substantial: up to 100,000€ from the same donor to the same recipient, and up to 300,000€ total for the recipient, subject to conditions. The funds must be used quickly, and the property must meet occupancy or rental commitments afterward.

Why does this matter? Because in today’s lending environment, the strength of your down payment matters enormously. A buyer who can bolster their personal contribution through a compliant family gift may present a much stronger file to a cautious French lender. It won’t rescue a weak application, but it can absolutely reinforce a solid one.

Then there is the renovation question, which is increasingly important in France’s older housing stock. The éco-PTZ remains available to help finance energy-efficiency improvements. This zero-interest loan can support eligible renovation work on a home that is or will become a principal residence, provided the property meets the required age and project criteria. Depending on the scope of the work, the amount can range up to 50,000€, with long repayment periods available. For buyers of older French properties—especially apartments that need energy upgrades—this is not a minor detail. It can be a useful part of the financing puzzle.

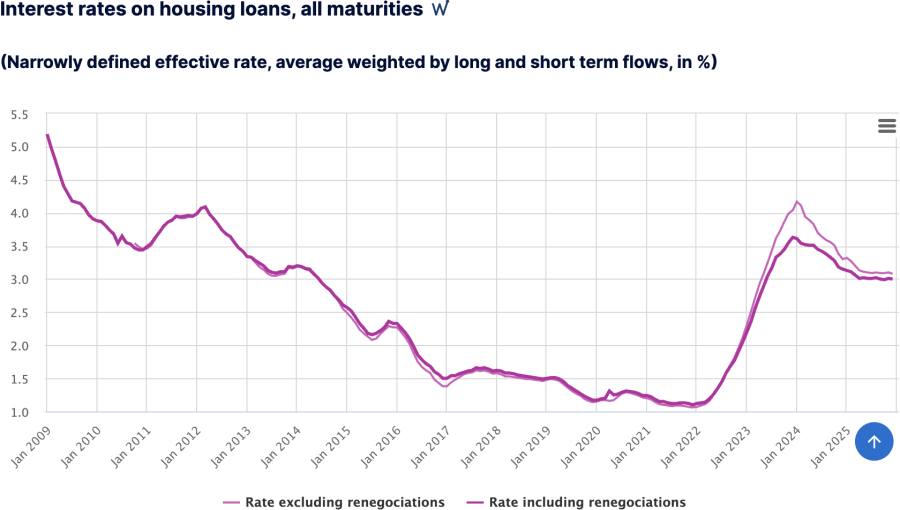

And what about rates themselves? Here the news is modestly reassuring. Banque de France reported that the average rate on new housing loans, excluding renegotiations, was 3.08% in December 2025. That is only a slight monthly improvement, but it is also well below the peak reached in early 2024. In plain English: financing is not cheap in the old sense, but it is no longer moving in the wrong direction at the same speed. That stability matters.

So what does all of this mean for foreign and expat buyers? The answer is both simple and very French: the system is more favorable if you are buying to live in the property, if your finances are well documented, and if your project fits the profile French banks and French public policy are designed to support. Principal residence buyers, first-time buyers, and households with a strong contribution have the clearest path. Buyers seeking a second home or occasional-use Paris apartment may find that the headline reforms do little for them directly.

That does not mean opportunity is absent. Quite the opposite. It means the opportunity is selective. In 2026, the French financing environment is no longer defined by panic or paralysis. It is defined by discipline. And for buyers who understand the rules, that discipline can be turned into an advantage.

There is every reason to take advantage of the low interest rates in France if you can. Thanks to our excellent relationships with local mortgage brokers, we can help you get the financing you need.

Going directly to just any French bank as a non-resident can be difficult if not impossible. Unless you have a regular salary going into a French account, they tend not to be interested in dealing with foreign clients.

The good news is that obtaining a mortgage here can be doable. There are a few options, including applying with a French lender that specializes in non-resident/foreign clients. While there are fewer and fewer banks that will to do this, we do have relationships with those banks that are willing.

AND NOW THE NUTS AND BOLTS…

One of the many advantages of purchasing property in France is the opportunity to benefit from historically low interest rates—when financing is structured correctly. With the right guidance, obtaining a French mortgage as an international buyer can be both achievable and advantageous.

Thanks to our trusted relationships with experienced local mortgage brokers, we can connect you with professionals who understand the nuances of financing for non-residents. Approaching a French bank directly without local income or a French banking history can often be challenging. Many institutions are reluctant to engage with foreign clients unless specific criteria are met.

The reassuring news is that financing is possible. While the number of lenders willing to work with non-resident buyers has narrowed, there are still French banks that actively specialize in this segment. Through our network, we work with those lenders and brokers who know how to present international profiles effectively and efficiently.

For many investors, paying all cash is not always the most strategic approach. Leveraging financing at competitive interest rates may allow you to preserve existing investments—such as equities or diversified portfolios—while maintaining financial flexibility. Borrowing at a relatively low cost can be an effective way to optimize long-term value.

WHO THE LENDERS ARE

France’s banking system is layered and diverse, made up of mutual banks, regional institutions, and a limited number of national lenders. Each applies its own lending criteria, which can make access more complex for non-residents, particularly when applications are submitted remotely. Language and procedural differences can further complicate the process.

For this reason, Adriana Leeds Group works with carefully selected mortgage brokers who specialize in assisting international buyers. These professionals are equipped to guide clients through the process remotely while ensuring clarity, responsiveness, and realistic expectations.

LOAN QUALIFICATIONS

1. Income Considerations

French banks primarily assess affordability based on income rather than assets. While your overall wealth profile is reviewed, the determining factor is your ability to service the loan. Monthly credit commitments—including the proposed French mortgage—generally must not exceed one-third of gross monthly income.

Certain investment income may be taken into account, and in some cases, anticipated rental income from the property being purchased can be included. Existing obligations such as car loans, mortgages, and rental payments are deducted, while consumer debt, taxes, and insurance premiums typically are not.

2. Age Limits

For non-resident borrowers, loan terms are usually limited to 20 years and must be fully repaid by age 75.

Still many buyers go for an interest only 10 years. It optimizes their disposable income and acknowledges that their needs are likely to change over the years. In any case, the option of refinancing the asset remains open.

INSURANCE REQUIREMENTS

While life insurance is not technically a condition for borrowing, French lenders require a borrower protection policy. This coverage protects both the borrower and their family in the event of unforeseen circumstances and ensures financial security for surviving partners.

HOW MUCH CAN YOU BORROW?

As a general guideline, purchases below 1.5 million€ may qualify for financing of up to 70% of the purchase price. Higher-value properties may allow for loan-to-value ratios of 100% or even 110%, provided additional financial collateral is pledged to the lender.

PROPERTY APPRAISAL AND DUE DILIGENCE

In certain cases—particularly for unique properties or transactions priced at the upper end of the market—lenders may request a formal appraisal. France also has a robust due diligence process designed to protect buyers. Detailed reports cover energy efficiency, electrical compliance, environmental factors, and potential constraints. The Notary coordinates these steps to ensure full transparency.

PURCHASE COSTS

For higher-value transactions, notarial fees and related costs may sometimes be included in the loan. More commonly, buyers should expect to pay these costs at the time of the final deed signature, along with agency and brokerage fees.

FINANCING RENOVATIONS

Renovation costs—particularly those related to energy efficiency—may be included in the mortgage, generally up to 15% of the property value. Alternatively, a separate renovation loan can be arranged.

INTEREST RATES IN FRANCE

Due to longstanding regulatory frameworks, France continues to offer some of the most attractive mortgage interest rates in Europe. Fixed-rate loans over 20 years are standard, with new-build properties often eligible for 25-year terms. Government-regulated rate caps provide additional borrower protection. While variable-rate loans are available, the current low-rate environment often makes fixed-rate financing the preferred choice for long-term security.

To learn more about financing in France, contact one of our resources. Visit our website and be sure to let them know we sent you!

SPECIAL NOTES:

Sources:

– HCSF lending rules and flexibility quotas

– PTZ expansion update

– PTZ eligibility details

– Temporary tax-free family gifts for housing

– éco-PTZ guidance

– Banque de France housing-loan rates

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. We’re the folks who can make your French property investment dream come true, while protecting you from making serious mistakes. Review the services we offer to help you find the perfect property in France!

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.