Weekly insights about property in France!

Subscribe and don't miss an issue!

Getting a Mortgage in France

Volume XXI, Issue 38

Last week, Brian Dunhill of Dunhill Financial, Simon Conn, an Overseas Property and Finance Specialist (AKA Mortgage Broker) and I gathered together on Zoom to offer up the “North American Expats in France Quarterly Financial Forum—3rd Quarter.” During the webinar, Simon was very encouraging about how our clients can get mortgages, in spite of the difficulties.

With more than 35 years of arranging financing in over 50 countries and having been heavily involved in creating the first residential mortgage facilities for foreign nationals and expats, to both purchase and re-mortgage properties in countries all over the world, Simon has a range of solutions most brokers don’t have!

Simon Conn

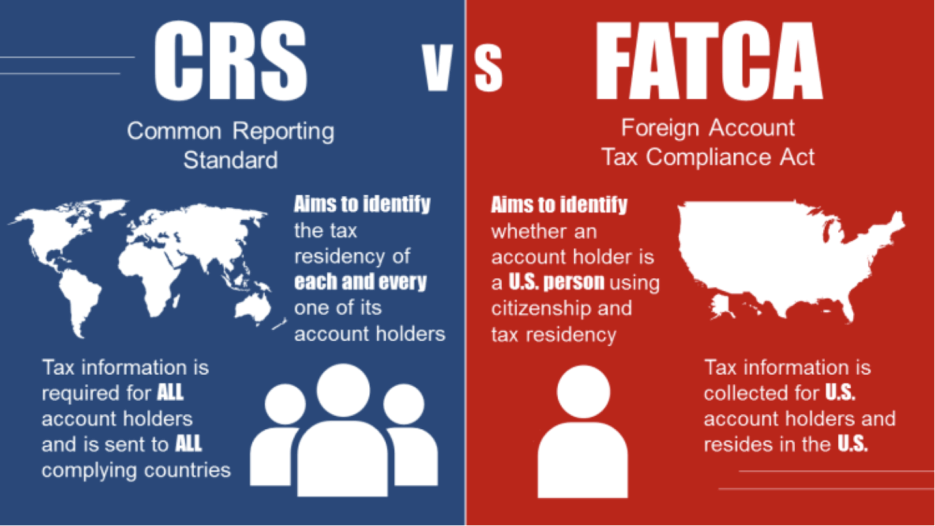

There is every reason to take advantage of the low-interest rates in France if you can. Thanks to our excellent relationships with local mortgage brokers such as Simon Conn, we can help you get the financing you need. Going directly to just any French bank as a non-resident can be difficult, if not impossible. Unless you have a regular salary going into a French account, they tend not to be interested in dealing with foreign clients, especially Americans thanks to the FATCA regulations.

The good news is that obtaining a mortgage in France can be doable!

Who qualifies? And what qualifies you?

In France, the affordability analysis by the lending banks is principally income-based, rather than asset-based. Your net asset profile forms an important part of the analysis but does not determine how much one qualifies to borrow, as is normally the case in North America. The French banks apply an affordability ratio which dictates that your monthly credit commitments (to include the proposed new French mortgage) cannot exceed one-third of the monthly gross income.

Investment income can be included in the affordability analysis and it could be possible to include some rental income from the property you are purchasing. Monthly credit commitments would include your car payments, other mortgages, rents, and other debts, which are deducted from your gross income. Consumer debt (credit card balances), taxes, and insurance premiums are not deducted from you’re your gross income.

The maximum term for a non-resident is typically 20 years and must be paid in full by the age of 75. This means that if you’re over the age of 60, it’s difficult, but not impossible.

A mandatory life insurance policy, assigned to the lender is a condition of borrowing, and therefore your age, lifestyle and health history become a factor contributing to the cost of borrowing. Depending on the loan amount for which you are applying and your age, medical exams may be required to qualify for the insurance…and therefore the loan.

Typically borrowing up to 70% or 80% of the purchase price (net of purchase costs) is achievable. It is not common practice for the lenders to perform an independent appraisal of the property for lending purposes, but they reserve the right to do so.

The notarial taxes and fees cannot be consolidated in the loan. It can be possible to include the agency commissions, if they are included in the sale price and to be paid by the seller. In the case when the buyer pays the agency commissions, the basis for the notarial taxes and fees is reduced, but the bank will not finance them.

It is not currently possible to include renovation costs in the borrowing from the lender.

The type of loan product offered (fixed or variable) depends on the prevailing market conditions. In the recent low-interest rate climate, the lenders have only offered fixed rates, but as the cost of borrowing increases, the lenders may offer fixed and variable options as well.

Notes:

• We highly recommend understanding your borrowing power before visiting properties.

• A loan is a commitment and must be repaid. Check your ability to repay before committing yourself.

• As a mortgage is secured against your home, it could be repossessed if you do not keep up the mortgage repayments.

• Your payments will be automatically deducted from your French bank account.

• We recommend you consult your accountant or tax attorney for advice regarding mortgage interest deductions on your tax return.

Simon Conn is an Introducer Appointed Representative of Seico Insurance & Mortgages Ltd Limited which is authorized and regulated by the Financial Conduct Authority under number 300024 in respect of UK mortgage, insurance and consumer credit-related activities only. If a mortgage is denominated in a currency other than your home currency, there is a risk that changes in the exchange rate may increase the equivalent value of the debt in terms of your home currency.

Simon will provide you with a free initial consultation and we will always explain exactly what you will be charged before you choose to proceed with an application. As we offer a personalized service, our charges can vary and the actual amount payable will be shown on any eventual quote. It may also depend on the country where you require financing, who arranges the financing for you, plus your personal circumstances and loan requirements. It is important that you seek independent legal and taxation advice on any property that you are going to purchase.

To watch the webinar in its entirety, and learn who makes a good candidate for a mortgage, visit our YouTube channel.

For more information and to contact Simon directly, please visit our website page or see his website.

Either way, be sure Simon knows we referred you! And good luck on getting a mortgage in France!

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

Adrian circa 1970

P.S. We are seeking to hire more rental search consultants for all of France. Your place of residence, as long as it’s in France, is not necessarily important to the search as much is done “virtually” by email, phone and online meetings. The skills required are: knowledge of the rental market and process, basic computer skills, a moderate level of French, the ability to be assertive, good communication skills and the ability to work well with a variety of personalities. If you are interested, please email us and provide a resumé.

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.