Weekly insights about property in France!

Subscribe and don't miss an issue!

Getting Ready to Buy a Home in France

Volume XXIV, Issue 14

By Jay Corless, Edited by Adrian Leeds

For many expats, buying a home in France begins with a dream: a Paris pied-à-terre, a village house in Provence, or a permanent move to a place that feels more aligned with the life they want to live. But before the keys, before the champagne, and certainly before the signature at the notaire’s office, there is one thing every buyer needs: a complete and credible file. In France, property purchases are structured, secure, and highly document-driven. That is especially true when the buyer is coming from abroad.

The first documents are the most obvious. You will need valid identification, usually a passport, along with proof of address. But that is only the beginning. The notaire will also want to understand your civil status clearly: are you single, married, divorced, widowed, or buying with a partner? If you are married, the legal regime matters, because it can affect how the property is owned and what happens later in the event of inheritance or resale. In practice, that often means producing marriage certificates, divorce judgments, “pacte civil de solidarité” (“PACS” documentation), or other supporting records, sometimes with certified translations depending on the country of origin.

(We ask all of our purchasing clients to fill out a form filled with all of this important information as part of our service.)

For expat buyers, the most important part of the file is usually the money trail. French property transactions are closely supervised, and professionals involved in the deal are subject to anti-money-laundering rules. Notaires are classified as “reporting entities”—meaning they are personally liable if they fail to flag suspicious transactions to TRACFIN (France’s financial intelligence unit). Showing the funds come from the buyer’s own account is how the notaire fulfills this duty.

That means the notaire, agent, or lender may ask not only whether you have the funds, but where they come from and how they will arrive. A simple “I have the money” is not enough. Buyers should be ready to show recent bank statements, proof of savings, investment account statements, sale proceeds from another property, inheritance documents, or gift documentation if family money is involved. The cleaner the trail, the smoother the process.

Don’t be surprised if the notaire requires an attestation from the bank that the funds came from the buyer’s personal account. If the money comes from a third party—a relative, a company, or a foreign account, not in the buyer’s name—the notaire will typically require additional documentation: a “déclaration de don manuel” (gift declaration) or proof of a loan, for instance. Without satisfactory explanation, the notaire can and will refuse to complete the sale.

(Download the PDF all about it, in French.)

This can get a bit tricky when the buyers’ names change between the pre-sale agreement to the final deed. The “Compromis de Vente or Promesse de Vente” (pre-sale agreement) normally carries a “clause de substitution” (substitution clause) that allows the original buyer—known as the “promissaire” or “acquéreur initial”—to substitute another person or legal entity in their place as the final purchaser at the time of the “Acte Authentique de Vente” (the completion).

When the “Compromis de Vente” is signed, the buyer reserves the right to designate a substitute purchaser before the final deed is executed at the notaire’s office. The substitute steps into the original buyer’s shoes and becomes the legal buyer of record. The original signatory effectively steps out of the transaction.

The reasons this happen vary, but the most common reasons are: tax and estate planning, investment structures, family arrangements, or uncertainty over the purchasing vehicle. It’s standard procedure, but be prepared to move money between bank accounts to make the transaction fully “kosher” under French law.

If you are financing the purchase with a mortgage, the file becomes even more detailed and complex. Lenders typically want proof of identity, income, tax documents, debt information, and details about the property itself. If your financial life is spread across more than one country, expect the bank to ask more questions, not fewer. French lending is perfectly accessible to international buyers in many cases (less so to American buyers—we have “FATCA” to thank for that), but it rewards organization and penalizes ambiguity. (See this page for official information.)

(Note: when applying for a mortgage, be sure to consult with us first on how to present your financial information to the bank. Remember: they are assessing their risk lending you the money, so if you tell them about your dream of quitting your job, moving to France and opening a B&B, they might not be so open to lending you money!)

And then there is the property file itself, which matters almost as much as your own. In France, the seller must provide a substantial package of diagnostics and disclosures. These can include the “Diagnostic de Performance Énergétique” (DPE), asbestos and lead reports where relevant, electricity and gas diagnostics, natural-risk information, and, in the case of apartments, a stack of “copropriété” (homeowner association) documents. Buyers should review these carefully, because they reveal not just the condition of the home, but the likely future cost of ownership. (See this site for more information on the diagnostics.)

This is where recent changes are especially important. Since January 1, 2025, DPEs carried out between January 1, 2018 and June 30, 2021 are no longer valid for a sale, which means some older files now have to be updated before a transaction can proceed properly.

Energy-related obligations have also become more important. For houses and certain buildings held in single ownership, the mandatory energy audit that already applied to the least efficient homes has expanded further. Buyers should pay close attention to whether it is required and included in the technical file. In practical terms, a buyer today needs to think not just about charm and location, but about renovation exposure.

(Note: when working with the Adrian Leeds Group, we do all this due diligence for and with you. We will review all of the important diagnostics and explain them so that you are fully aware of the assets and liabilities of the property before signing even the pre-sale agreement.)

Apartment buyers also need to pay closer attention to the building as a whole. The collective DPE requirement for copropriétés has been phased in over time and expanded again from January 1, 2025 for buildings with 50 to 200 lots, with smaller qualifying buildings following from January 1, 2026. That means more apartment purchasers are now expected to examine building-level energy performance, not just the flat they are buying.

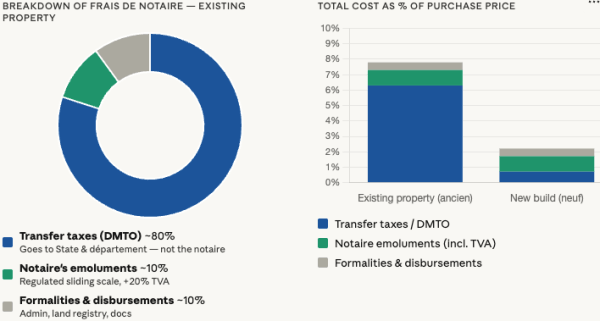

There have also been recent cost changes that buyers should factor into their preparation. France’s 2025 budget gave local authorities the option to increase transfer taxes on property purchases by up to 0.5 percentage points from April 1, 2025, while first-time buyers were excluded from that increase. That is not a document issue, strictly speaking, but it does affect how much cash you need ready at the moment of purchase. Allow for approximately 7-8% of the net price of the property.

(Here’s how you can estimate the notarial taxes and fees.)

So what should an expat have prepared before signing a pre-sale agreement? A valid passport, proof of address, civil-status documents, tax identification information, and a well-organized source-of-funds file are the essentials. If financing is involved, add income documents and bank paperwork. If you are buying with a spouse, partner, or through a company, the documentary burden rises, so it is wise to prepare early rather than react under pressure once the deal is underway.

France still offers one of the safest and most transparent property-purchase systems in the world. But it is not a place to improvise. The buyers who succeed are usually not the ones who move fastest after finding the right home. They are the ones who had their paperwork ready before they ever walked through the front door.

We’re a group of North Americans who enjoy helping expat buyers do exactly that. Beyond the property search itself, our role is to help clients understand the buying process, prepare the right documentation, communicate effectively with agents and Notaires, and avoid the confusion that can come with navigating a foreign legal and administrative system. We act as a kind of “insurance” to avoid a buyer making very costly mistakes.

For international buyers, that guidance can make the difference between a stressful purchase and a smooth transition into life in France.

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. To learn more about our services to assist you in finding and purchasing the right property in France, visit our website (You don’t want to do it alone!)

P.P.S. If you have friends interested in making a property investment in France, forward on this Nouvellettre® so they can subscribe and learn as much as you have! (Or send them to our subscription page.)

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.