Weekly insights about property in France!

Subscribe and don't miss an issue!

The France Real Estate Market Trends as of October 2023

Volume XXI, Issue 46

The following market trends information is provided by the Chambre de Notaires de France as reported November 9, 2023.

REAL ESTATE MARKET: TRENDS AND DEVELOPMENTS IN PROPERTY PRICES – OCTOBER 2023

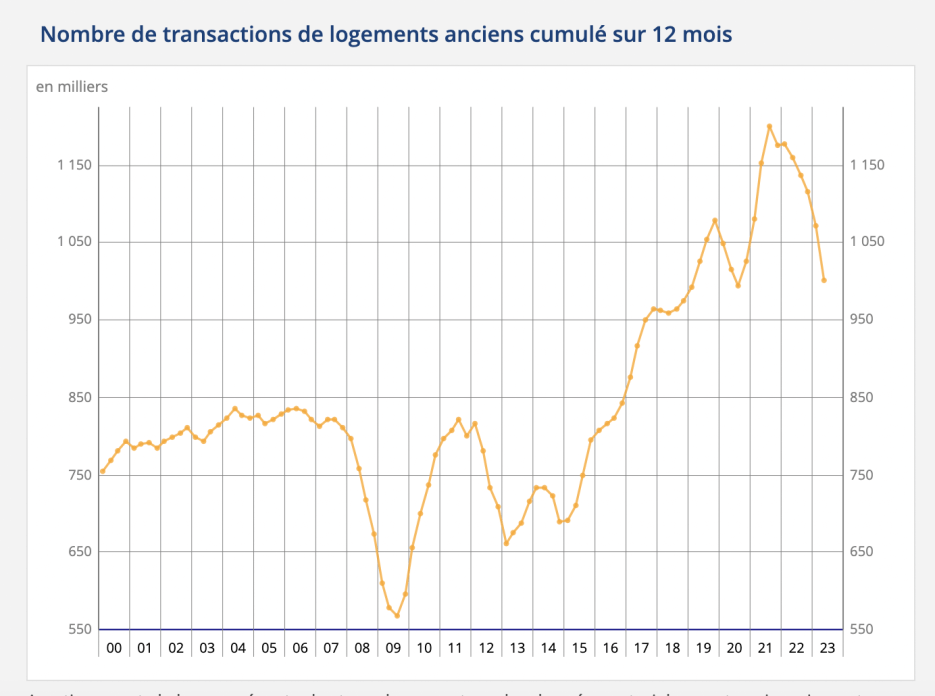

The cumulative volume of sales of existing homes over the last twelve months in France (excluding Mayotte) reached 955,000 at the end of August 2023. Since autumn 2022, annual sales volume declines have gradually intensified: from 3% at the end of July 2022, to 6% in January 2023, to over 10% since April 2023. By the end of August 2023, the year-over-year fall in sales volume had reached 16.6%. A year-over-year decline of this magnitude had not been seen for ten years.

In the wake of the eurozone debt crisis and during a recession in France, sales volumes reached 650,000 transactions, compared with about 800,000 a year earlier, which was considered normal. The current market is contracting as a result of the European Central Bank’s (ECB) monetary policy, which has the sole aim of ensuring that inflation returns as soon as possible to its medium-term target of 2%. Against this gloomy backdrop, the ECB nonetheless indicated in its end-of-September economic bulletin that inflation is continuing to slow, although it is likely to remain strong for too long a period.

But, it seems that the ECB’s key interest rates have reached their maximum. As a result, they could remain at these high levels for several months without increasing, and could even fall in the medium term once the objective of curbing inflation has been achieved. In this respect, notaries are noting a large number of loan refusals, bringing many projects to a halt and creating a disappointing effect, given the French people’s continuing appetite for property, a safe investment in troubled times. In any case, the year is likely to end at about 900,000 transactions, a sign of a very sharp year-over-year slowdown, combining inflation, high interest rates and the end of “euphoria.” The readjustment in sales volumes has been brutal, and could continue over the coming year.

As for prices of older homes in mainland France, they recorded their first annual fall at the end of summer 2023. After holding up until July 2023 (-0.2% year-over-year), prices in mainland France fell by 1% year-over-year in August 2023, for the first time since the end of 2015. This decline would accelerate in the following months, reaching 3% year-over-year in November 2023, and would be slightly greater for resale houses (-3.2%) than for resale apartments (-2.7%).

![]()

In the provinces, prices of existing homes are expected to fall less rapidly than in mainland France, with -1.9% to the end of November 2023. The market for existing apartments is expected to remain resilient at -0.3% to the end of November 2023, compared with -2.7% for existing houses. Apartment prices are expected to be virtually stable in Lille, Marseille and Toulon, while significant annual falls of at least 8% are expected in Besançon, Mulhouse, Nantes, Angers and Rouen.

Sales of existing homes in the largest conurbations at the end of November 2023 are expected to record sharp annual declines of at least 8% in Amiens, Orléans, Nîmes, Saint-Étienne, Valence, Lyon and Toulon. More moderate declines, in the 3 to 6% range, are expected in Le Havre, Maubeuge, Rennes, Valenciennes, La Rochelle, Toulouse, Le Mans, Grenoble and Lille.

In the Ile-de-France region, leading indicators for pre-sales contracts point to an extension of the downward trend between now and November. The price per square meter in Paris, set at €10,130 in July, would fall below the symbolic €10,000 mark in November 2023 (€9,940). The annual fall would then be 6.1%. Compared with the high point of €10,860 per square meter in November 2020, prices in the capital would therefore fall by 8.5% in 3 years. An annual fall in prices of around 6% is expected in November for both apartments and houses, with no department escaping.

The inflationary context has mechanically impacted the purchasing power of the French, and with borrowing capacity shrinking, buying a property has become extremely complex, even more so for first-time buyers whose income levels are no longer sufficient to make a purchase possible. Trade-offs are being made to the detriment of real estate acquisition, in view of the French people’s means of living.

The initial stages of the declared price adjustment show a cautious beginning, as sellers are hesitant to embrace a significant price reduction that aligns more closely with the economic reality of the market. Despite the potential for a decrease in their prices, this notion is gradually gaining traction amid a shift toward more open negotiations, favoring the buyer, in response to the prevailing economic conditions in the market.

However, the market is still suffering from a wait-and-see attitude towards prices, which is also impacting the rental market, as tenants wishing to buy a property are likely to stay put for longer, thus restricting the supply of rental properties. Similarly, since the beginning of 2023, homes with a final energy label worse than class G on the DPE (>450 kWh/square meter/year), i.e. around 140,000 homes, are no longer considered habitable, and therefore excluded from the rental market for new leases.

The property market as a whole is undergoing a period of contraction, and the new-build market has not been spared. The extension of the PTZ (Prêt à taux zéro, zero interest loan) until 2027 even though its disappearance was scheduled with an increase in the maximum amount to €100,000 and conditions of resources, as well as an expansion of the perimeter to 210 municipalities additional. Its scope of application seems far from satisfying building stakeholders who note on the one hand the exclusion of the individual house (particularly with regard to the fight against the artificialization of land), but above all the tightening of the PTZ on purchases of new apartments in tight areas or old housing with work in non-stressed areas, de facto excluding rural areas.

The Energy Efficient Housing in 2022, from the Note de Conjoncture Immobilière, October 2023

Since the beginning of 2023, homes with an energy label G on the DPE (diagnostic de performance énergétique, energy performance diagnosis) that consume more than 450 kWh/square meter/year in final energy (around 140,000 homes) are no longer considered decent and are therefore excluded from the rental market (for new leases). Since the end of August 2022, it has also been forbidden to increase rents on F and G-rated properties. Article 160 of the August 2021 Climate and Resilience Act plans to successively increase energy decency criteria for rental until 2034. Ultimately, all housing with a label higher than D will be affected by the rental ban, representing around 45% of the private rental stock by January 1, 2022. More recently, an implementing decree published in August 2023 maintains the deadlines set out in the law, and clarifies the timing and level of the first minimum energy performance requirements imposed on landlords to be able to rent out their homes. In mainland France, the ban will apply to all G-rated homes by January 1, 2025, to F-rated homes by January 1, 2028, and to E-rated homes by January 1, 2034. The decree also specifies the exemptions allowed for landlords. These may include, for example, architectural constraints that prevent work from being carried out to meet the thresholds. Or they may be unable to carry out the necessary renovations, due to a lack of funds.

In mainland France (excluding Corsica), the proportion of older homes sold with energy labels F and G rose from 11% to 16% between the 2nd quarter of 2021 and the 1st quarter of 2022. The increase is more significant for G-rated homes, from 3% to 6%, compared with 8% to 10% for F-rated homes. This change occurred, in particular, in the 2nd half of 2021, following the revision of the DPE calculation method, but also following the first announcements of minimum energy performance requirements. Until the beginning of 2023, the proportion of older homes sold with energy labels F and G continues to grow, but at a much slower rate, reaching 18% in the second quarter of 2023 (+7 points in two years).

This phenomenon is common to all departments, although a few stand out from the general trend. These are mainly those already recording a high proportion of F and G label sales. Along with Haut-Rhin, Savoie and Haute-Savoie are the only departments to see their share fall slightly between Q2 2021 and Q2 2023. Conversely, many departments in the south-west of France had a low share of sales of very energy-intensive homes in Q2 2021, but saw their share more than double by Q2 2023, as in Tarn-et-Garonne, Landes and Pyrénées-Atlantiques. In Gironde, it even increased almost fourfold.

In 2022, around one in three sales of apartments with F or G labels will take place in a city of over 100,000 inhabitants, compared with one in four a year earlier. This represents an increase of around 10 points, while the increase in overall sales is just 2 points. While in previous years the impact of the energy label on housing prices was less significant in multi-family homes, particularly for the worst labels (F and G), this is no longer the case in 2022. In fact, the discount generated by an F or G label, compared with a similar class D apartment, is significant in all regions of mainland France (excluding Corsica). This discount even exceeds -10% in the Grand Est and Hauts-de-France regions.

Download the report in PDF (in French).

For more information about France property market trends and related issues, don’t hesitate to contact our office.

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. Special note: Our Office Hours are Monday through Friday 9 a.m. to 6 p.m. France Time. The office is also closed for all France holidays and December 24th through January 1st annually. If you were planning on using these holiday times to visit properties, these are not the best times as we cannot promise that we or the other agents and owners will be available.

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.