Weekly insights about property in France!

Subscribe and don't miss an issue!

Take Advantage Now of the Change in Capital Gain

Volume IX, Issue 37

As one might guess, the changes to the capital gains tax laws is having an effect on the market…for the moment, in a relatively positive way for the buyer. These laws do not affect the sale of a primary residence, on which no capital gains tax is paid.

To fully understand the changes to the law and the affects it might have upon the current market, we’ve turned to SARF for information. SARF (Société Accréditée de Représentation Fiscale) is an accredited tax representative which specializes in capital gains tax on property payable by non residents. It is a private company and we make no recommendation here, but are merely citing it as our source of information on this issue.

The French government requires that a seller have a professional tax representative to calculate capital gains at the time of a sale of property and the tax is deducted at the time of closing. You may choose your tax representative, SARF being among the choices.

This past September 19th, the method of calculation of the capital gains tax laws was enacted.

In immediate affect, the new laws have removed the original tax deduction of 1000.

As of October 1st, 2011, residents will realize and increase in payroll taxes of 13.5%. This does not concern foreign, non-resident buyers.

Effective November 1st, 2011, 1) the deadline by the Notaires for recording of the transfers will be reduced to one month (except in cases where the award period is two months) and 2) property sold abroad must be recorded within one month of the sale by a recognized Notaire in France.

As of February 1st, 2012, the new tax laws will take affect. Until this time, the law has allowed a 10% reduction of tax after the first five years of ownership, so that in effect, after 15 years of ownership, no capital gains tax was due. This has been changed to 30 years in the following calculation:

* 2% for each year of ownership beyond the fifth (between 6 and 17 years of ownership)

* 4% for each year of ownership beyond the seventeenth (18 to 24 years of ownership)

* 8% for each year of ownership beyond the twenty-fourth (25 to 30 years of ownership)

* After 30 years of ownership of the property, the gain will be totally exempt.

The general rules of calculating the tax are as follows for sales by individuals:

* The chargeable gain is calculated as follows (see section 150 V of the French Tax Code (CGI):

Disposal price (Article 150 VA I of the CGI)

+ amounts due by seller but paid by buyer (Article 150 VA II of the CGI)

– costs borne by the seller (Article 150 VA III of the CGI)

– purchase price

– costs and expenses allowed by law

– acquisition costs

– works

= Gross chargeable gain

* The gross chargeable gain is then reduced by:

– an allowance of 10% per year from year 6 onwards,

– then a fixed allowance of 1,000 per joint owner

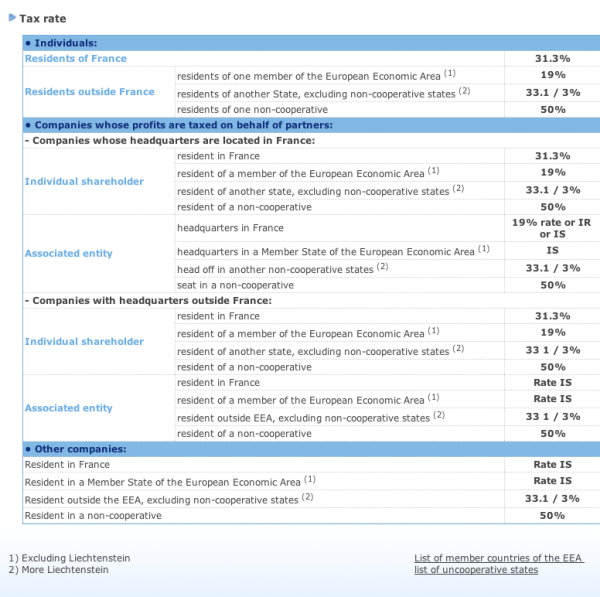

* This gives the net chargeable gain, which is taxed at the rate of tax which depends on the seller’s country of domicile.

Disposal price

(36 to 44 Instruction of 14 January 2004):

* This is the actual price as stated in the deed. If the price is not declared in full, the dissimulated amount is added to the price stated in the deed (Article 150 VA-I of the CGI)

+ Increased by any charges normally payable by the seller but which are paid by the buyer (38/39/40 Instruction of 14/01/04):

> These include any capital charges and any indemnities declared to benefit the seller for whatever reason, but which are paid by the purchaser instead of the seller,

– Less:

> the VAT paid by the seller on this disposal (43 Instruction 14/01/04)

> the costs borne by the seller, limited to (Decree of 31/12/03):

– fees paid to an intermediary (agency) or representative (tax representative),

– costs of the certificates and surveys imposed by law,

– eviction indemnities paid to a tenant by the owner who sells the property vacant,

– fees paid to an architect for surveys enabling a preliminary authorization for a planning permit,

– the costs paid by the seller to de-register a creditor’s mortgage charge on the property.

Acquisition price (Article 150 VB-I of the CGI)

* Defined as:

– For acquisitions made in return for payment: the price actually paid by the seller, as declared in the deed

– For acquisitions without payment: the value taken into account to calculate the conveyance tax (if ownership split into usufruct/bare title, see form n°16, Instruction of 4/8/2005).

* Are added to the purchase price, subject to justification and actual payment by the seller:

– All capital charges and all indemnities declared to benefit the seller in any way or for whatever reason,

– The costs associated with the acquisition:

>If acquired in return for payment:

->either an all-in amount equal to 7.5% of the purchase price (including agency commission),

-> or the actual costs (notary’s costs and fees, registration taxes, agency commission, etc.)

-> If acquired free of charge:the conveyance costs and fees

-> if they were actually paid by the seller

->and in proportion to the fraction of the value represented by the property or property rights.

Works

* The cost of building, rebuilding, extension and improvement works are deductible:

– either under certain conditions and with documents in proof at their actual value,

– or at an all-in value of 15% of the purchase price, under the condition that the person liable for the tax sells the property more than 5 years after purchase.

* Costs of roads, drains and utilities:

– incurred for building land,

– whether or not such works are imposed by the local council or group of councils

Allowance for number of years of ownership

The gross chargeable gain is reduced by an allowance of 10% per full year of ownership, from the 6th year onwards. There is total exemption after 15 years of ownership (Art. 150 VC-I of the CGI).

Allowance of 1,000 (Article 150 VE of the CGI)

* A fixed allowance of 1,000 per seller, whether the property is owned individually, in common, or with split usufruct/bare title.

* i.e. this allowance rises to 2,000 for sales by a married couple or by common law partners.

* For sales by an SCI or registered partnership, the allowance stays at 1,000 (and not 1,000 per partner).

As a result of the changes in the tax laws, owners of properties are quickly jumping on the bandwagon to sell their properties in order to realize the current tax benefits. The agencies are reporting a flood of panicked sellers and properties priced to sell quickly.

This presents a small window of opportunity, between now and February 1st, 2012, to have a wider choice of property than we have seen in years and at fair prices. In addition, the current weaker euro contributes to advantageous moment. (1 = U.S. $1.35490, £0.87420, Australian $1.35232, Canadian $1.37130)

After February 1st, my guess is that owners will be holding on to their properties longer, reducing inventory and thereby increasing values based on the law of supply and demand.

If your objective is to invest long term in a revenue-generating property, then now is a great time to make a purchase. And if you think that you’re ready to divest of your French property, then consider selling.

French Property Insider consultants can assist you with your decision and realizing your goals. For more information, email:Capital_Gains_Tax

Special Property Picks in Nice

Soon I will be signing the Acte de Vente on the Nice apartment and beginning the renovation soon after. Since our arrival on the Riviera scene, there has been more interest by our readers in investing in Nice and environs where prices are about half of what they are in Paris.

Our Property Search Consultant in Nice has been scouring the market for properties in central Nice that fit the bill for good investment. I doubt the properties will be on the market for long, so if you are interested in learning more about any of the following properties, be sure to contact us immediately.

Well, there you are for now. Let me know what you think!

Rue Dalpozzo #1 in the Carré d’Or:

Rue Dalpozzo #1 in the Carré d’Or:

Two rooms entirely renovated on the last floor with an elevator, cellar and pleasant views. 36m2. Individual gas heat.

Asking Price: 210,000 + 3% Finder’s Fee.

Rue Dalpozzo #2 in the Carré d’Or:

Rue Dalpozzo #2 in the Carré d’Or:

On the corner of rues Dalpozzo and de France, a two-bedroom, two-bath apartment on the second floor with an elevator (the rights of which must be purchased) with a balcony off the living room. 71 m2.

Asking Price: 360,000 + 3% Finder’s Fee.

Avenue Victor Hugo (near rue Bacquis and Maccarani):

Avenue Victor Hugo (near rue Bacquis and Maccarani):

Two-bedroom apartment with 25 m2 terrace and a retractable awning. Currently under renovation, it is on the first floor with an elevator in a good quality building facing the side street and therefore, quiet. 50m2.

Asking Price: 380,000 + 3% Finder’s Fee. (No photo)

If you are interested in learning more about these properties and others in the Nice area, please contact us at Nice_is_Nice

A bientôt,

Adrian Leeds

Editor, French Property Insider

Email: [email protected]

P.S. I am speaking on October 11th about property prices and trends at a free “Residential Property Investing Seminar” sponsored by BNP Paribas Investment Partners. (Scroll down for more information an to register to attend.) And for just a bit of blowing our own horn — Le Palace des Vosges (Le Palace des Vosges), our very own fractional ownership property in La Place des Vosges, will be the backdrop this coming month for filming ‘yours truly’ by Eurocinema On Demand and Seductively French (Seductively French) in the production of lifestyle segments celebrating the European way of life designed to reach 36 million U.S. and Canadian television homes beginning December 2011 as well as airing in China on Metan Development Group’s Hello! with half a billion viewers.

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.