Weekly insights about property in France!

Subscribe and don't miss an issue!

The Property Market in Paris and the Region

Volume XXII, Issue 36

The following report was released September 10th by the Chambre de Notaires de Paris:

In the second quarter of 2024, business is still sluggish and the annual decline in prices is slowing, but the first signs are a little more encouraging.

The wait-and-see attitude is still prevailing on the market, and sales volumes of existing homes have fallen again, by 18% compared with the same quarter last year, and by as much as 38% compared with the second quarter of 2022. However, while the market remains bearish, the decline in sales is becoming progressively less pronounced, in a very slow but steady movement. The annual fall in prices has slowed following the stagnation of values in recent months. Pre-sale contracts confirm these trends for the third quarter, with sales volumes likely to be even lower than last year, and annual price declines still visible but less sharp.

The crisis is deep-rooted, and is likely to be long-lasting in an uncertain and shifting economic and political context. But there are encouraging signs that we are approaching the lows before a hoped-for upturn in sales volumes.

The market remained at a standstill in the second quarter of 2024, driven mainly on the sellers’ side by constrained transactions (arrival of a child, divorce, professional change, inheritance…). Notaires describe buyers as taking their time, hesitating and sometimes giving up.

Financing conditions have eased, with interest rates announced by the Banque de France at 3.43% in June and 3.39% in July (compared with a high of 3.62% in December 2023), and, at the same time, access to credit has been eased. But solvency has improved only slightly.

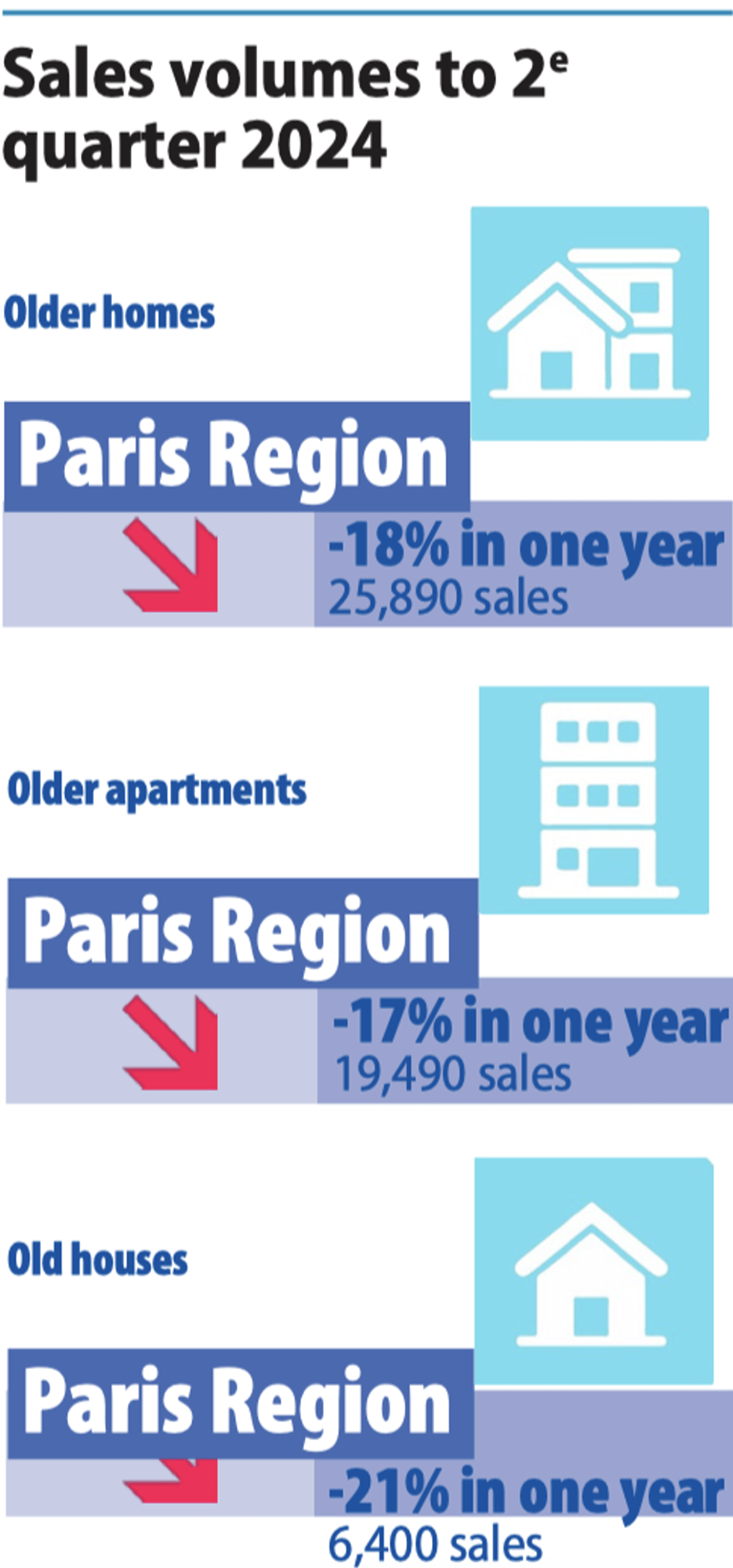

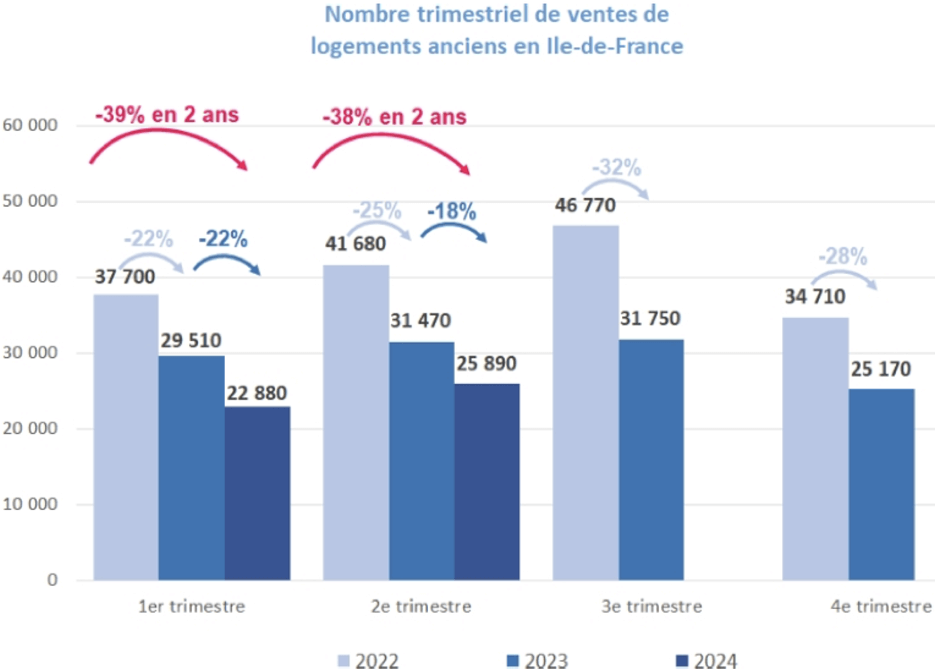

The slowdown in activity has continued, and sales volumes of existing housing in the Paris region fell by a further 18% in the second quarter 2024 compared with the second quarter 2023. The decline reached 38% compared with the second quarter 2022.

After being boosted by the consequences of COVID and a renewed desire for space and greenery, the house market is still experiencing the sharpest falls in activity, with sales down by 21% compared to the second quarter 2023, and above all by 44% compared to the second quarter 2022. In the Petite Couronne, in what is admittedly a very tight market, sales of existing homes have practically halved in two years. In the second quarter 2024, sales volumes of apartments in the Paris region were down 17% in one year and 36% in two years.

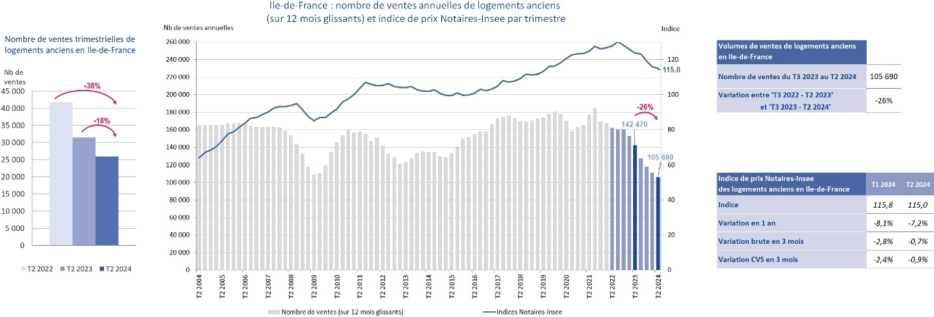

Over the past 12 months, there have been about 106,000 sales of existing homes, a decline of 26%, and around 37,000 sales in the Ile-de-France region alone. The level of activity is historically low, and close to that seen during the subprime crisis. The current crisis is both wide-ranging and long-lasting, and all the more severe for having occurred after a phase of extreme dynamism in the real estate market.

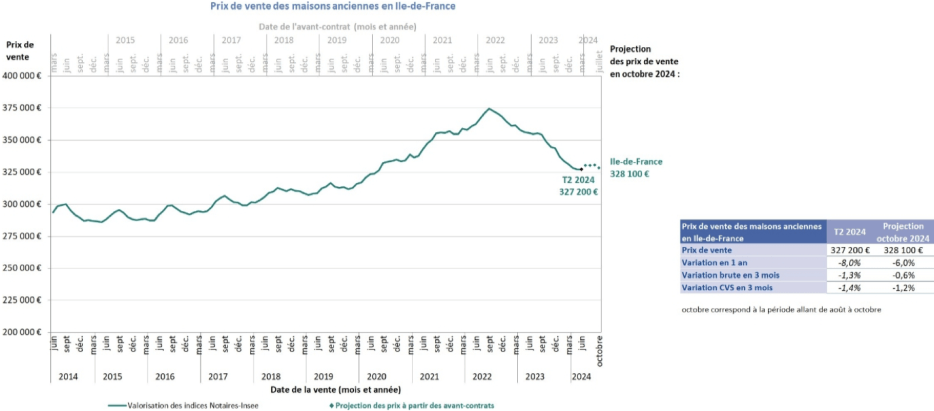

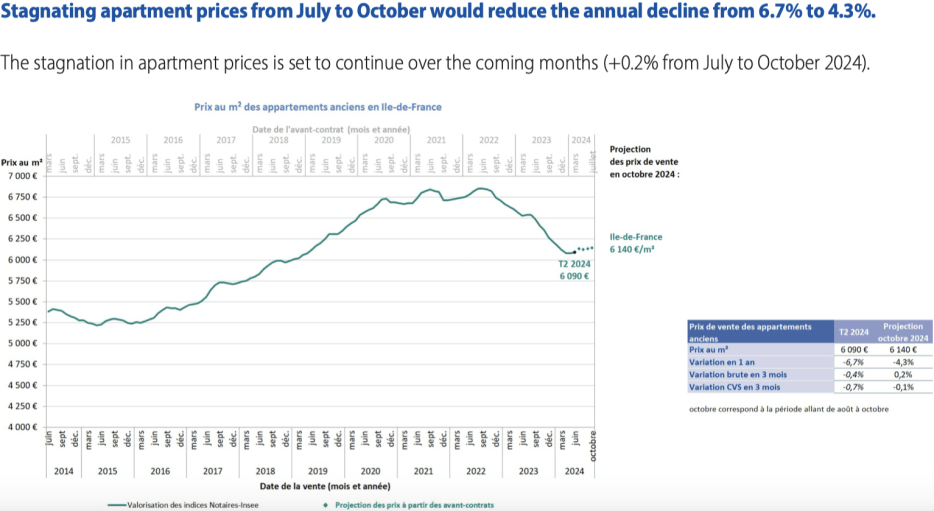

The contraction in activity has naturally weighed on sales prices. However, this downward trend is gradually easing or coming to an end, even as sales volumes continue to fall. This is true for all markets in the Paris region and, according to preliminary contracts, is set to continue into October.

From first to second quarter 2024, the annual fall in apartment prices is reduced from 8.4% to 7.4% in the Petite Couronne and from 7.0% to 5.5% in the Grande Couronne. The trends are identical for houses, but slightly less pronounced. The annual fall in house prices held steady at 8.5%, as in the previous quarter, in the Petite Couronne. In the Grande Couronne, it fell from 8.2% to 7.8%.

According to pre-sale contracts and in October 2024, the annual decline for apartments could be reduced to 2.0% in the Grande Couronne and 4.9% in the Petite Couronne. For houses, it would remain more sustained (-5.0% in the inner suburbs and -6.4% in the Greater Paris area).

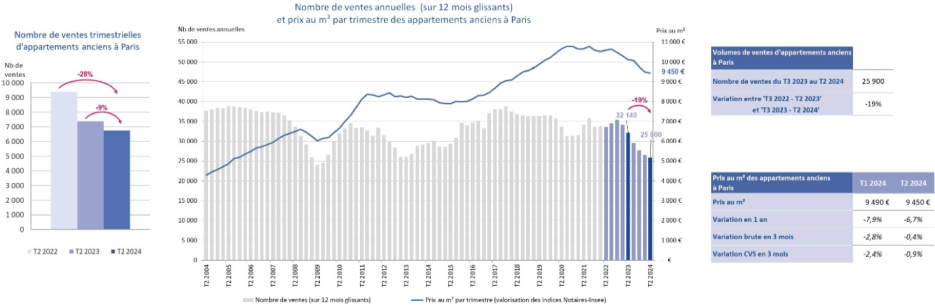

In Paris, the price per square meter stands at €9,450 (-6.7% in one year). It should stabilize at about €9,500 by October. Since the high point in November 2022 (€10,860 per square meter), the cumulative fall in prices has reached 12.6%.

Several hypotheses can be put forward to explain this slower decline in prices, but we don’t know how to validate them. Has the fall in interest rates encouraged owners to maintain their prices in the hope of a recovery in demand? Do they consider the accumulated decline sufficient and unacceptable? Is buy-to-let economically impossible, given current prices and interest rates? Or is awareness of the tight housing supply in the Paris region encouraging owners to hold on to their properties?

What is certain is that the slowdown in price declines is preventing a clearer improvement in household solvency.

The figures are in: at most, we’re seeing a less sustained decline in activity, which has fallen to historically low levels. Pre-sale contracts suggest that this downward trend in sales volumes will continue into the 3rd quarter, albeit at a slower pace. Beyond that, it is difficult to identify the market dynamics that will be at work (a durably constrained market and a prolonged pause, or a rebound?).

There are signs of improvement, with inflation expected to fall below 2% year-on-year in July 2024. should enable further cuts in home loan rates in the coming months. This remains an essential determinant of solvency, and the key driver of business recovery, given current price trends.

According to our estimates, in October 2024 and compared with August or September 2023, when creditworthiness was at its worst, monthly payments had fallen by 6.7% for apartments (enabling the purchase of 3.9 square meters more) and by 8.6% for houses (enabling the purchase of 7.7 square meters more).

This improvement in solvency could continue, although it is to be feared that acquisition conditions will not be as favorable as during the boom period in the near future.

The political context and the budgetary policy guidelines more specifically dedicated to housing also add further uncertainties to a market that seems to be permanently under severe constraints, despite the ever-renewed desire of households to become homeowners.

HOUSING IN ILE-DE-FRANCE

In the second quarter of 2024, sales volumes of existing homes in the Paris region fell by 18% and 38% compared with the second quarters of 2023 and 2022. Over 12 months, activity reached an all-time low close to that of 2009, with just 105,700 sales. Prices fell by 7.2% year-over-year, and by 11.6% compared with the peak recorded in September 2022.

Sales volumes in the second quarter 2024 fell by 38% compared with 2022 and by 18% compared with 2023 (versus -28% in the fourth quarter 2023 and -22% in the first quarter 2024). Business thus continues to decline, but at a slower pace.

APARTMENTS IN THE PARIS REGION

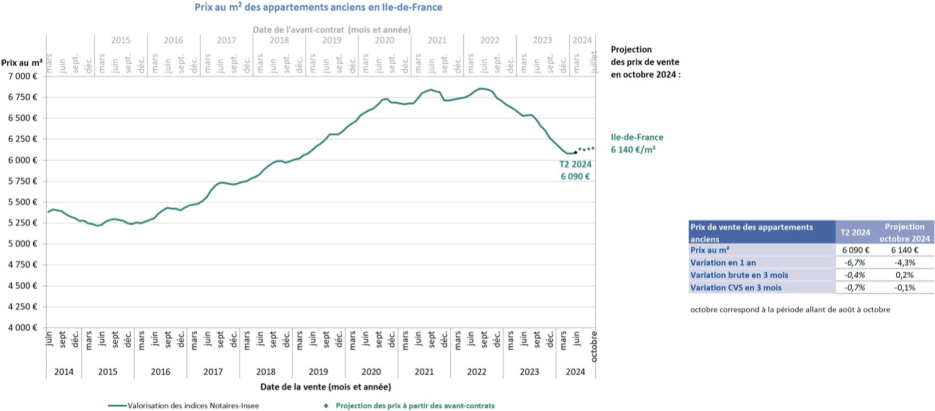

Sales of apartments in the Paris region barely reached 78,000 in 12 months (-24% compared to the previous 12 months) and 19,500 in 3 months (-17% compared to the second quarter 2023). Prices per square meter for apartments, down 6.7% year-on-year versus -7.9% in the first quarter 2024, are back where they were five years ago. They are down 11.1% on the high point of the third quarter 2022.

Stagnating apartment prices from July to October would reduce the annual decline from 6.7% to 4.3% and is set to continue over the coming months (+0.2% from July to October 2024).

HOUSES IN ILE-DE-FRANCE

Not seen in more than 25 years, with only 28,000 homes sold over the past 12 months and prices down 8% year-on-year.

The downturns are once again more marked for houses than apartments, both in terms of activity and prices. In the second quarter of 2024, sales volumes of existing homes fell by 21% in one year, and by 44% in two years, across the whole of the Paris region. House prices fell by 8% in one year, and by 12.7% compared with the peak recorded in the third quarter 2022.

As for apartments, the pause in prices is set to continue over the coming months (-0.6% from July to October).

PARIS APARTMENTS

Activity is historically low in the capital, while the annual decline in prices is slowing (-6.7% in the second quarter).

With just 26,000 apartment sales in 12 months, and fewer than 7,000 in the second quarter of 2024, Paris is close to its 2009 low. Nevertheless, the declines are less severe than in the Petite and Grande Couronne areas: -19% over the last 12 months, -9% compared to the second quarter 2023 and -28% compared to the second quarter 2022.

Apartment prices per square meter stood at €9,450 in the second quarter. This represents a year-on-year fall of 6.7%, as in the Paris region as a whole, and a 13% drop on the November 2020 record (€10,860). This is the only market where prices have fallen over 5 years (-4.5%).

Prices in Paris are expected to stagnate over the next few months, stabilizing at around €9,500 per square meter.

The expected stagnation of prices from July to October could reduce the annual fall in Paris apartment prices from 6.7% to 4.5% in October. Compared with the November 2020 peak (€10,860 per square meter), prices would fall by 12.6%.

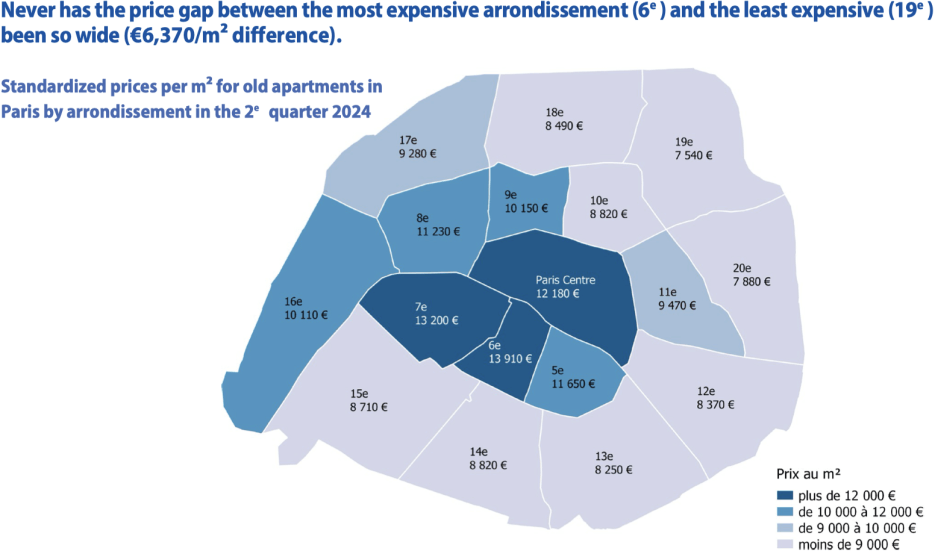

In the second quarter of 2024, prices per square meter ranged from €7,080 (La Goutted’Or district in the 18th arrondissement) to 16,620 (Champs-Elysées district, 8th ).

The least expensive neighborhoods have seen the sharpest annual declines (up to -11% in the Amérique and Charonne neighborhoods).

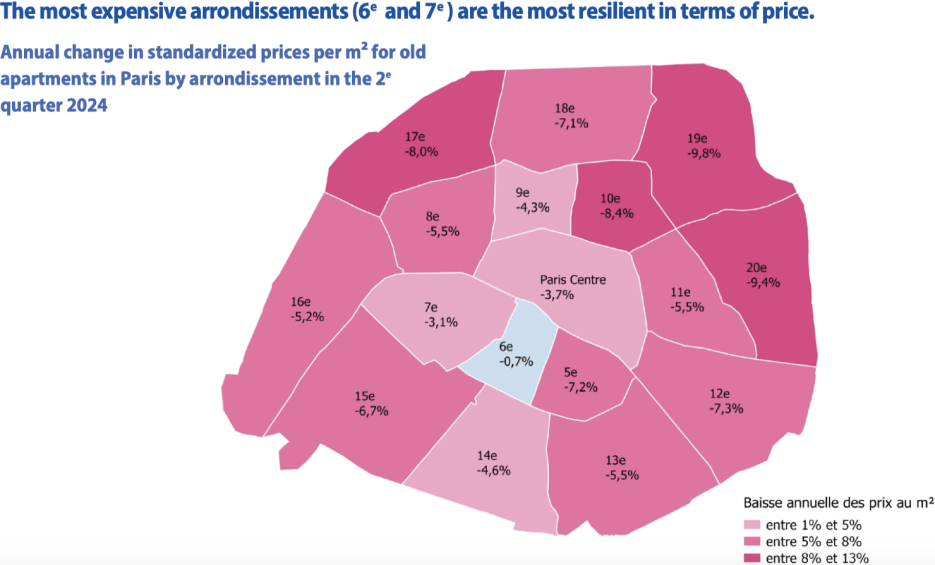

Never has the price gap between the most expensive arrondissement (6th) and the least expensive (19th) been so wide (€6,370/square meters difference).

Prices per square meter range from €7,540 in the 19th arrondissement to €13,910 in the 6 e (1.84 times more expensive than the 19th). The 10th arrondissement falls below €9,000 per square meter and the 20th joins the 19th arrondissement below €8,000 per square meter.

The most expensive arrondissements (6th and 7th ) are the most resilient in terms of price.

Annual price declines are heterogeneous, ranging from 0.7% in the 6 e arrondissement to 9.8% in the 19 e . 4 arrondissements show annual price declines in excess of 8%, including the 19 e and 20 e , the least expensive arrondissements in Paris.

FOCUS: Since 2022, the proportion of energy-inefficient older homes has risen sharply in the Paris Region

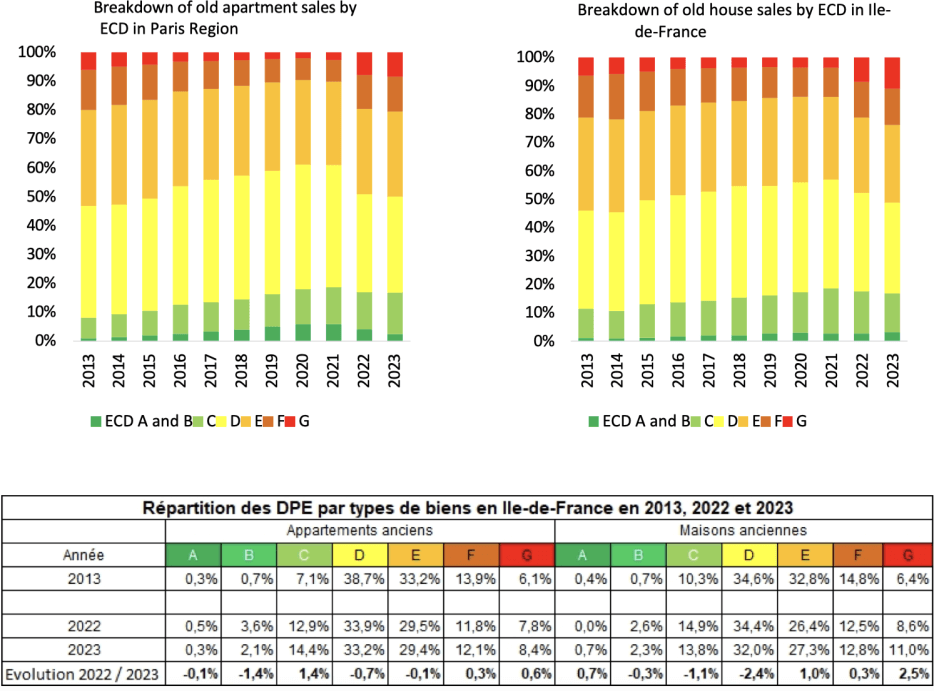

Until 2021, we have seen a gradual increase in the share of energy-efficient older homes in sales. The proportion of apartments rated F or G has fallen from 20% of sales in 2013 to 10.2% in 2021. Houses have followed the same trend, albeit at a slightly slower pace (21.2% F and G ratings in 2013, down to around 14% from 2019 to 2021). Conversion, renovation and a preference for higher-rated homes have undoubtedly driven these slow but steady trends.

But this trend has come to a halt. On the contrary, since 2022, the proportion of energy-inefficient property sales has increased. The impossibility of renting (Climate and Resilience Act) and the prospect of a potential discount on the value of the property have undoubtedly prompted owners to dispose of their energy-guzzling properties. At the same time, these properties have found takers. The proportion of apartments rated F or G, which had fallen to around 10% between 2019 and 2021, rose sharply in 2022 (19.6%), a trend that will continue in 2023 (20.5%).

A similar trend can be observed for homes, with the share of energy-intensive home sales rising from 13.9% in 2021 to 21.0% in 2022 and 23.8% in 2023.

At the same time, the share of sales of energy-efficient homes is eroding. Apartments with an A, B or C label accounted for 18.7% of sales in 2021, but only 17.0% in 2022 and 16.8% in 2023. For houses in the same category, sales fell from 18.5% in 2021 to 17.4% in 2022 and 16.8% in 2023.

This phenomenon is particularly pronounced in Paris, where the housing stock is very old and made up of small, low-rated units. The proportion of homes rated F and G, limited to 20% in 2013, has jumped to 30.3% in 2022 and 32.2% in 2023.

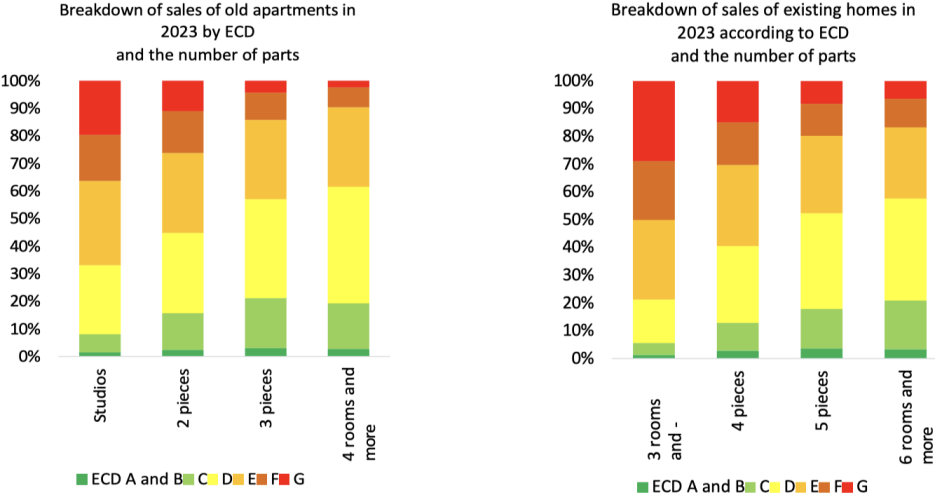

Pending a change in regulations for small dwellings, the number of rooms in a dwelling has a major impact on its energy rating. The current method of calculating performance diagnostics (which relates energy consumption to surface area) is to be revised by a decree on July 1, 2024, to avoid penalizing small homes.

Small, energy-hungry units, are over-represented in sales. In 2023, 36.4% of studio sales in the Paris region will be “energy wasters” (F or G), and 30.5% will be rated E. This leaves just over a third of studio sales with an DPE rating between A and D.

At the other end of the scale, only 9.6% of large apartments with four rooms or more were sold with an F or G label, and 28.9% with an E label. 60% of sales of large apartments therefore have an DPE ranging from A to D.

The situation is similar for houses.

The change in DPE regulations that is about to be enacted should therefore lead to an improvement in diagnoses for properties under 40 square meters, and will probably rebalance these data.

It should also be noted that frequent changes in regulations can skew the analysis of ECD data. In fact, current ECDs remain valid for several years, despite changes in regulations. We are therefore led to aggregate data on the same energy labels, but calculated using different methods.

FOCUS: How solvent will Paris Region buyers be in the coming months?

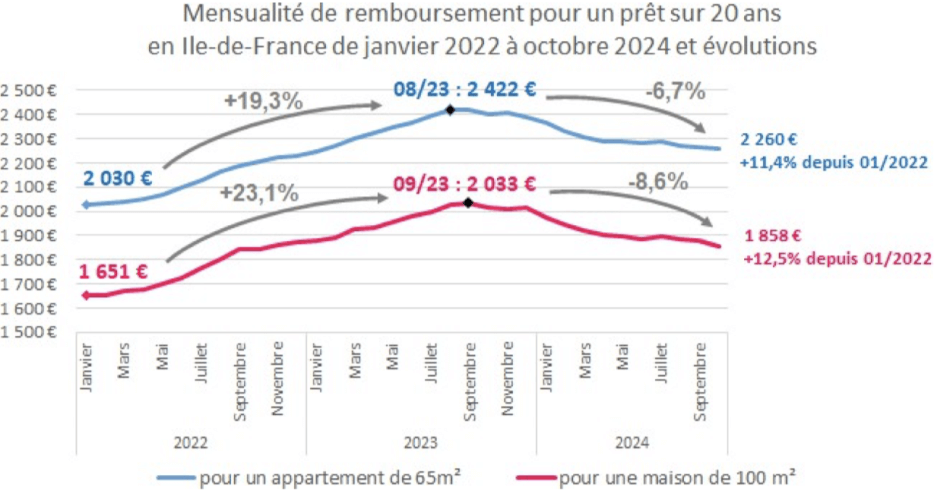

Monthly payments are expected to rise by 11.4% for apartments and 12.5% for houses between January 2022 and October 2024 in the Paris region.

If you could buy a 65 square meters apartment in January 2022, for the same total cost of borrowing and taking into account the evolution of interest rates, you will be able to buy 58.4 square meters in October 2024.

If you could buy a 100 square meters house in January 2022, for the same total cost of borrowing and taking into account the evolution of interest rates, you will be able to buy 88.9 square meters in October 2024.

Read the full report (in French).

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. If you are an American living outside the U.S., please be sure to vote absentee in the upcoming presidential election. I just submitted my U.S. Absentee Voting Registration by email.

P.S. If you are an American living outside the U.S., please be sure to vote absentee in the upcoming presidential election. I just submitted my U.S. Absentee Voting Registration by email.

Visit Vote From Abroad to find all the information you need to register and vote.

If you want to ensure we won’t have a dictator in the White House, you may want to join Democrats Abroad, the official Democratic Party arm for millions of Americans living outside the United States. Democrats Abroad gives overseas Americans a voice and helps elect Democratic candidates by mobilizing the out-of-country vote.

And, you can join a States Team as well so you can get up-to-date information about voting in your state.

Do it now!

1 Comment

Leave a Comment

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.

Adrian, thank you for telling expats to vote! You probably cheered on Kamala Harris during the debate. She was born about a mile from where I live in Oakland, CA, so I’m very proud that you’re supporting her too!

If you have a chance in an upcoming newsletter, please consider asking your readers to vote for Democrats in the House and Senate so that Harris has a congress who can pass bills on her agenda.

Thanks!