Weekly insights about property in France!

Subscribe and don't miss an issue!

It’s Still a “Wait-and-See” Market

Volume XXII, Issue 7

According to the latest report (“Conjoncture immobilière francilienne en novembre 2023”) by the Chambre des Notaires de Paris, sales volumes in Ile de France are still a wait-and-see market. The decline in activity continues, with just 31,910 sales of existing homes in the Paris region between September and November 2023, down 30% and 13,840 sales compared with the same period in 2022 (45,750 sales).

Even more significantly, sales volumes are down 25% on the average for the last 10 years. The market remains stuck at a very low level of activity. This is hardly surprising, given that household solvency remains very poor, despite some encouraging signs from banks and price cuts that are now widespread, but insufficient to offset the rise in mortgage rates.

A number of major trends observed over the last few quarters persist, beyond the sharp, widespread downturn in activity. For example, sales volumes are down slightly more for houses (-32% in one year) than for apartments (-29%). At the same time, the fall in activity in Paris (-27%) remains slightly less marked than in the rest of the region. Lastly, the housing market in the inner suburbs (Petite Couronne) remains the hardest hit (-35% in one year).

The downward trend in prices has recently intensified. In Ile-de-France over 3 months, from August to November 2023, house prices fell by 2.8%. After adjusting for seasonal variations, the quarterly fall in prices remains high (-2.5%). Over a one-year period, from November 2022 to November 2023, house prices in the Paris region fell by 6.8%, with comparable declines for apartments (6.7%) and houses (7%).

In Paris, the price of old apartments would fall from €9,870/m² in November 2023 (-6.7% in one year) to €9,520/m² in March 2024, according to the leading indicators on pre-contracts. The annual fall in prices could increase further to 7.7% from March 2023 to March 2024.

In the coming months, price adjustments are likely to be slightly more marked in the Petite Couronne than in the Grande Couronne. This is true for both apartments and houses. According to our leading indicators on pre-contract sales, we expect apartment prices to fall by 8.7% in the Petite Couronne and 7.2% in the Grande Couronne. House prices are expected to fall by 9.1% in the Petite Couronne and 7.3% in the Grande Couronne.

Purchasers who are not resident in France at the time of purchase continue to buy more apartments in Paris. The previous focus showed that the number of non-resident foreign buyers remained stable from 2022 to 2023 (1,180 and 1,250 acquisitions respectively for the first 9 months). They benefit from high purchasing power, often buy a pied-à-terre without a mortgage. As a result, they have not been as sensitive to the economic downturn as other customers. As the market as a whole contracted sharply, they became proportionally more numerous (from 0.8% to 1% of total sales), while remaining a micro-market.

These foreign buyers living outside France have a confirmed preference for the French capital. 68% of them have chosen to invest in Paris in both 2022 and 2023, compared with 49% in 2021 and even fewer in previous years. Only the Hauts-de-Seine department has managed to attract more than 10% of these transactions, with no other department exceeding 5%.

This refocusing of demand on the heart of the conurbation naturally benefits apartments, and the share of houses in these transactions has fallen to 5% in the last two years, from 15% up to 2021.

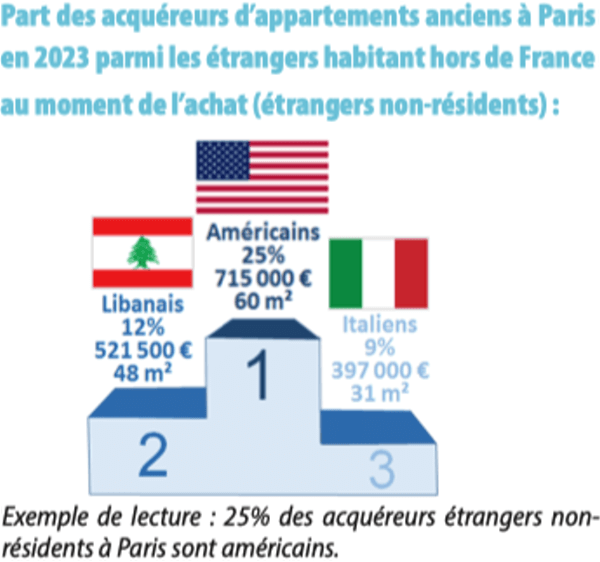

Buyers from the USA account for a quarter of all purchases by non-resident foreigners in Paris. Their purchase budget of €715,000 is twice as high as that paid by French residents, as they buy mainly in the capital’s central districts, where prices are highest. The second most represented country is Lebanon, with 90 Lebanese buyers, ahead of Italy (70) and Germany (45).

A record 62 nationalities are represented, one more than in 2022 and 15 more than in 2021, confirming the diversification of the customer base. The Portuguese and Chinese are still the most numerous among foreign buyers residing in France at the time of purchase.

The proportion of foreign buyers residing in France is slightly higher (10% for the first 9 months of 2023 vs. 9.2% for the first 9 months of 2022), but like the vast majority of buyers, they have been penalized by the difficulties of accessing credit and the decline in their purchasing power.

The Portuguese remain the leading foreign buyers of homes in the Paris region, with 13% of this category and 1,470 purchases in 2023. They are particularly attracted by houses, which they choose in 45% of cases. The Chinese are the second most represented nationality, with a very strong preference for apartments, which account for almost 90% of their purchases. The proportion of Portuguese buyers has fallen significantly over the years, accounting for 18% of foreign resident buyers in 2019. Chinese buyers remain stable at around 10%, closely followed by Algerians, Tunisians and Romanians.

To read the report in its entirety, download the PDF (in French).

Note: Our North American clients, for the previous couple of years, have tended to prefer the sunny Côte d’Azur to make their purchases rather than Paris—due to the lower prices, warmer weather and less restrictive rental laws. However, NOW is an excellent time to buy in Paris while prices remain low and the rate of exchange is favorable.

Don’t hesitate to contact us to learn more on how to make a smart investment in Paris (or anywhere in France).

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. We can help you make the move from beginning to end. Visit our website to learn more and to request a consultation and to learn more.

P.P.S. Friday I am headed to New Orleans, Maui and Los Angeles for 2.5 weeks to visit family and friends. I will be writing from these destinations so I hope to bring you a kind of travelogue, but beware that the timing of the Nouvellettres® may be a bit more erratic than usual. Please forgive me.

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.