Weekly insights about property in France!

Subscribe and don't miss an issue!

Grand Paris Property Market: Activity Returns, Prices Steady, and a Reminder to Think Long-term

Volume XXIV, Issue 7

By Jay Corless, edited by Adrian Leeds

The latest communiqué from the Notaires du Grand Paris confirms what many buyers and sellers have been feeling in real time: the Paris-region market is regaining its footing, but in a measured way. The recovery is real, transaction volumes are rising again, yet the rhythm is steady rather than euphoric, and the momentum is being carried more by the outer ring of the region than by central Paris. The underlying figures and methodology are detailed in the communiqué itself.

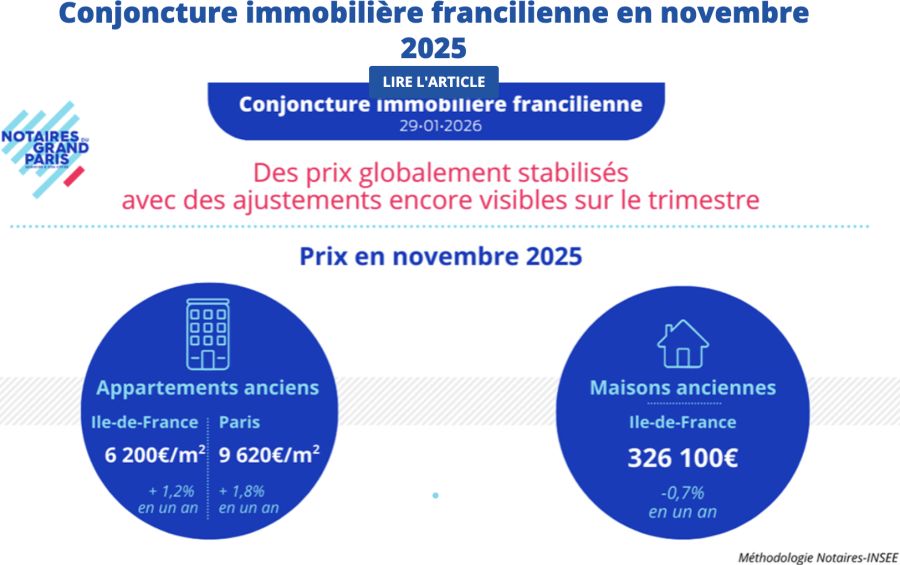

Over the three-month observation window that corresponds to “end of November” reporting, September through November 2025, the Notaires recorded 30,780 existing-home sales across the Île-de-France region, a 7% increase versus the same period one year earlier. What stands out is not only that activity is improving, but also where the improvement is concentrated. Houses are leading the rebound: house sales rose 10% year-on-year, compared with a 6% increase for apartments. The Grande Couronne remains the main engine, with sales up 9% overall (and +12% for houses), reflecting continued demand for more space and better value. Paris and the Petite Couronne are improving too, but less dramatically, at roughly +5% in Paris and +6% in the Petite Couronne over the same comparison window. The Notaires also note that, compared with the same period in 2023, volumes are only about +5%, which reinforces the idea of a gradual reset rather than a sharp snap-back.

On prices, the headline is stability, with gentle, and very local—variations. Region-wide, apartments are reported at around 6,200€ per square meter, up 1.2% year-on-year. Paris apartments sit around 9,620€ per square meter, up 1.8% year-on-year. Houses, meanwhile, are quoted at roughly 326,100€ on average regionally, still slightly down year-on-year by 0.7%, suggesting that the house market is stabilizing, but not yet uniformly turning upward everywhere. Over the most recent quarter covered in the communiqué (August to November 2025), movements are small and close to flat overall, consistent with a market that is normalizing rather than accelerating.

One of the most useful elements in the Notaires’ reporting is their use of “avant-contrats” (signed pre-sale agreements) to provide short-term indicators. Here, the message is cautiously constructive. Their projections suggest a modest near-term rise for apartments into March 2026 in both the Petite Couronne and Grande Couronne (respectively +1.2% and +1.8% from December 2025 to March 2026), while houses are projected to stabilize (around +0.2% over three months). The communiqué also flags that an uncertain macroeconomic backdrop and the possibility of renewed rate pressure could limit the extent of the recovery.

This month’s focus section is particularly relevant for international buyers who sometimes wonder whether Paris property can be treated like a quick flip. The Notaires are clear: after the post-2022 adjustment, reselling quickly has often produced losses. At the regional level, apartments resold after three years show an average decline of around -9.1%, which they illustrate as roughly -35,960€ on an average surface of 58 m². Losses are highlighted as especially sharp in high-priced areas such as Paris (about -8.9%, or roughly -50,350€ on 53 m²), Hauts-de-Seine (about -10.8%, or roughly -44,530€ on 61 m²), and Val-de-Marne (about -9.7%, or roughly -29,640€ on 57 m²). These figures are presented on price movement alone; in practice, short holding periods are further penalized by acquisition costs “frais de Notaire”, agency fees, and financing.

Yet when you widen the lens to reflect how property is typically held in France, the long-term picture remains intact. The Notaires note that holding periods have lengthened significantly, around 13.7 years for apartments and 15.8 years for houses on average (2024), which aligns with how many owners treat French property: not as a short-term trade, but as a long-term “patrimonial” asset. Over ten years, the region-wide apartment market is cited at about +17.5%, which they associate with an average gain around 54,000€ per apartment, while Paris is cited around +21.1% over the same horizon, with an estimated average gain around 89,570€ (based on an apartment around 53 m²).

So what does all of this mean for buyers and sellers today? For buyers, stability can be a gift. It tends to reduce the fear-of-missing-out dynamic and refocuses on fundamentals. In Paris and its surrounding communes, that means location at the micro level, building quality, and “copropriété” context, light, layout, noise, and increasingly, perceived energy comfort and future running costs. For sellers, the message is equally clear: the market is moving again, but it is selective. Correct positioning, clear presentation, and a coherent building story still matter enormously—and overpricing still tends to cost you time and negotiating power.

Our job is to help clients read this moment like locals. We translate notarial data into street-level strategy, help you evaluate value beyond the headline €/m², shape an offer plan that fits the property and the market, and coordinate the administrative and transactional complexity so the process feels controlled rather than opaque. In a market that is recovering gradually, good decisions are less about racing and more about choosing wisely, and then letting time do what it tends to do best in French real estate.

Note: Sources: Notaires du Grand Paris monthly communiqué (PDF); Notaires du Grand Paris summary page; Notaires du Grand Paris portal.

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

P.S. We’re the folks who can make your French property investment dream come true, while protecting you from making serious mistakes. Review the services we offer to help you find the perfect property in France!

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.