Weekly insights about property in France!

Subscribe and don't miss an issue!

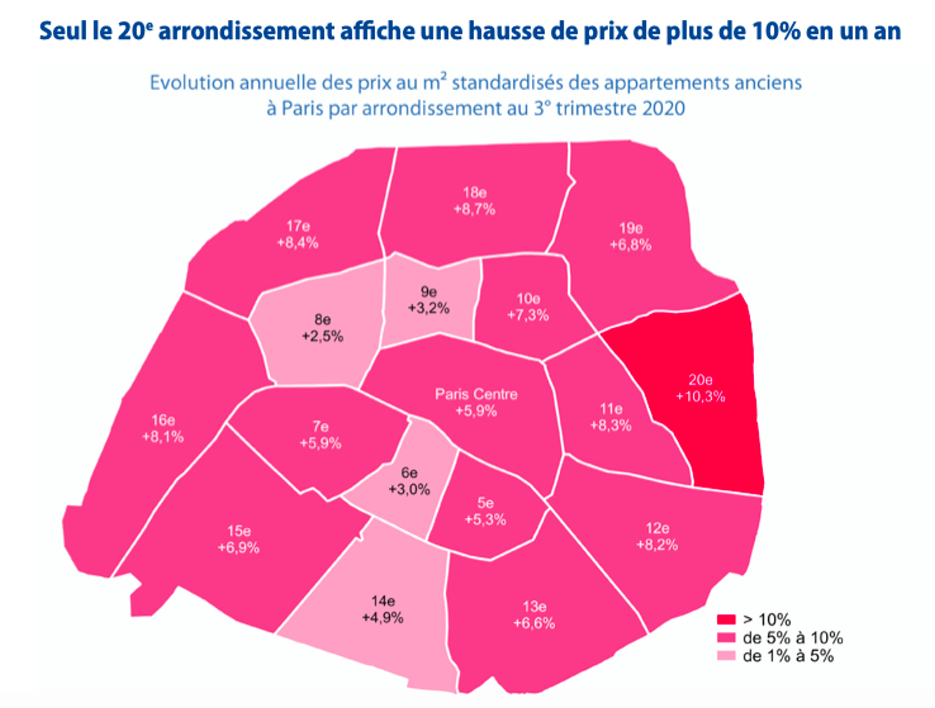

Paris Sales are Down, Prices are Up!

Volume XVIII, Issue 48

According to the recent report by the Chambre de Notaires de Paris, the health situation continues to weigh heavily on the real estate market. In third quarter of 2020, sales of resale homes were down 31 percent compared with third quarter 2019, a direct consequence of the first confinement. For apartments, prices are stabilizing from second quarter to third quarter 2020. Indicators from the Notaires du Grand Paris on pre-sale contracts anticipate a continuation of this trend, with, depending on the department, slight decreases in sales prices in December 2020 or January 2021. However, given past increases, apartment prices would still be on an annual increase at the beginning of next year. Conversely, for houses, the price increase would be accentuated at the end of the year and in early 2021, no doubt under the effect of a new interest among buyers for this type of housing in Ile-de-France.

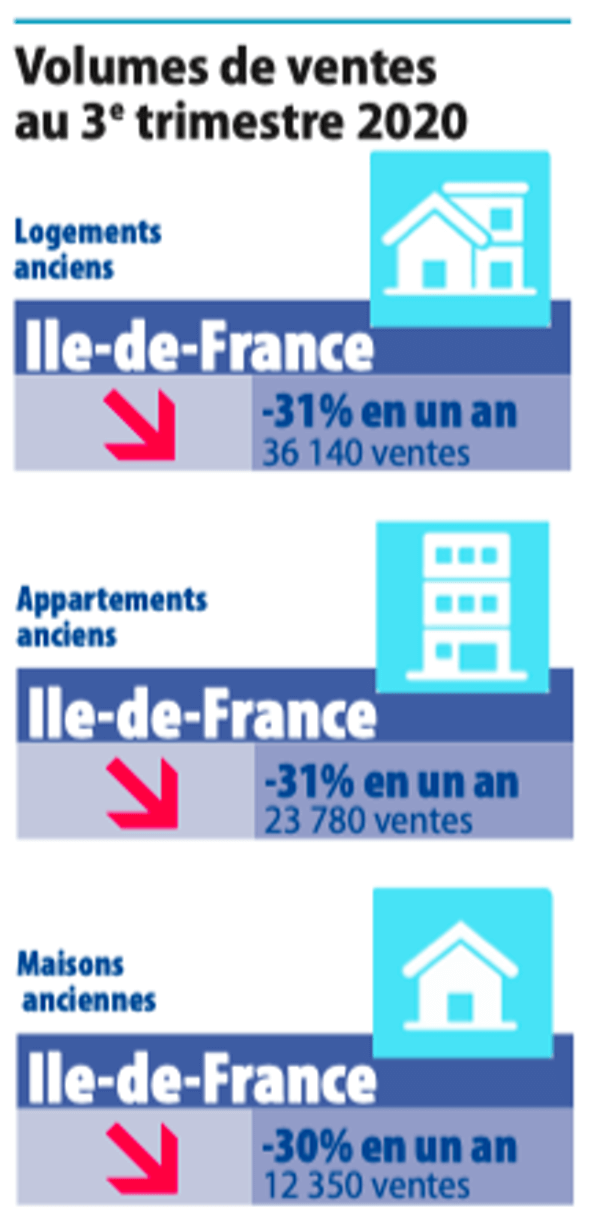

While there are still specific supporting factors for real estate activity, the Paris Region notaries are worried about the consequences of the new confinement on the market and the repercussions of the various shocks expected on households. The first confinement caused an unprecedented worldwide shock of unprecedented magnitude and violence to our lifestyles and economies. Overall, during the first nine months of 2020 and compared to the first nine months of 2019, sales declined by 21 percent in the Paris Region.

Year-to-year and over the last known 12 months, 152,000 resale homes were sold in the Paris Region, 15 percent less than a year earlier. The level of activity is comparable to that of 2014 or 2015, but far from the high levels of 2017, 2018 or 2019 when 170,000 to 180,000 sales were concluded each year.

Three quarters of consecutive declines in activity follow one another. In the first quarter of 2020, the nine percent decline is attributable to the confinement and collapse of sales in the last two weeks of March. The 22 percent decline in the second quarter is the sum of two very different dynamics: April, when activity collapsed, then May and June, when it rebounded to return to the levels of the exceptional year 2019.

Finally, in third quarter, the decline in sales volumes deepened further (-31 percent) and affected all geographic areas and all market segments. Everywhere, confinement prevented visits and then pre-sale contract signatures for a good part of the second quarter and weighed on activity, with a delay of approximately three months on sales.

The Paris market proved to be slightly less resilient from third quarter 2019 to third quarter 2020. Sales were down 34 percent. In the Greater Paris region, the decline in sales volumes (30 percent for apartments and 29 percent for houses) was limited to 7 percent and 13 percent, respectively, compared with the average for the third quarters of the last 10 years.

The Paris market proved to be slightly less resilient from third quarter 2019 to third quarter 2020. Sales were down 34 percent. In the Greater Paris region, the decline in sales volumes (30 percent for apartments and 29 percent for houses) was limited to 7 percent and 13 percent, respectively, compared with the average for the third quarters of the last 10 years.

Lower sales volumes or changes in market dynamics do not systematically or immediately impact prices. Often sales lead times are initially longer and negotiations become tighter on prices. Notaries in Paris describe such tensions, whereas the market remains much more fluid in the Greater Paris area, where people often become homeowners.

Apartments: slower price increases in the third quarter, which heralds a period of stagnation or very slight decreases

From the 1st to the 2nd quarter of 2020, apartment prices in the Paris Region rose by a further 2.1 percent, then with more moderation of 1.4 percent from the 2nd to the 3rd quarter of 2020.

According to our leading indicators on pre-sale contracts, prices per square meter would increase again from September to November 2020, before eroding. From October 2020 to January 2021, prices for older apartments would fall by 0.8 percent in the Paris Region. This evolution, which can be read graphically, is very moderate (-0.5 percent in the Petite Couronne and the Grandee Couronne in three months). It is slightly more marked in Paris (-1.2 percent). The price per square meter will not reach €11,000 per square meter and will be brought down to around €10,700 in January 2021.

If we analyze the annual variation of prices, this recent and moderate slowdown will not erase the increases of the first part of the year 2020. In January 2021 and compared to January 2020, prices would increase less rapidly, but still by 4.1 percent in Paris, 5.5 percent in the Petite Couronne and 4.6 percent in the Grande Couronne.

In this new context of stagnating apartment prices, the house market is going it alone. The annual price increases, already sustained in the third quarter of 2019, (+5.5 percent in the Lesser Couronne and +4.5 percent in the Grande Couronne) are expected to strengthen. According to our leading indicators on the pre-sale contracts, house prices could increase in January 2021 by 9.5 percent in annual percentage in the Petite Couronne and 6.2 percent in the Grande Couronne. We will have to wait for the sales figures for the 4th quarter of 2020 to confirm quantitatively, the renewed interest, already confirmed by the notaries, of the people of Ile-de-France in owning a house.

In this new context of stagnating apartment prices, the house market is going it alone. The annual price increases, already sustained in the third quarter of 2019, (+5.5 percent in the Lesser Couronne and +4.5 percent in the Grande Couronne) are expected to strengthen. According to our leading indicators on the pre-sale contracts, house prices could increase in January 2021 by 9.5 percent in annual percentage in the Petite Couronne and 6.2 percent in the Grande Couronne. We will have to wait for the sales figures for the 4th quarter of 2020 to confirm quantitatively, the renewed interest, already confirmed by the notaries, of the people of Ile-de-France in owning a house.

The new confinement is once again turning the tide and darkening the outlook for the real estate market. This new shock will have repercussions on the social economic landscape, even though the first shock wave has not yet produced its full effects and household confidence is affected.

The health crisis has confirmed that housing remains a safe haven. But economic and health uncertainties are weakening households, who need visibility and confidence to build their real estate projects. Low interest rates are reassuring. But the tightening of credit conditions, reported by several insurance brokers, is worrying. Financing facilities have been a decisive support allowing buyers to become homeowners over the last three years.

It is hoped that the deterioration in sales volumes in fourth quarter 2020 will not be as strong as in previous quarters. Indeed, the summer has been active and pre-sale contract volumes in third quarter 2020, which determine the 3-month sales outlook, are up one percent for apartments and 18 percent for houses compared with third quarter 2019. The terms of the new confinement give reason to hope that these pre-sale contracts will be transformed, thus limiting the decline in sales volumes during the quarter.

Nevertheless, October already seems to be marked by an initial decline in the volume of pre-sale contracts, and November should be very affected by the new confinement. When questioned over the last few days, 68 percent of Paris Region notaries said they had signed fewer pre-sale contracts in their office and 86 percent said they had received fewer pre-sale contracts from real estate agencies, compared with the same period in 2019. In addition, in this survey, eight out of 10 Paris Region notaries anticipated a (moderate or sharp) decline in their activity at the end of 2020 and beginning of 2021, confirming the increased fragility of the real estate market and the wait-and-see attitude of both sellers and buyers.

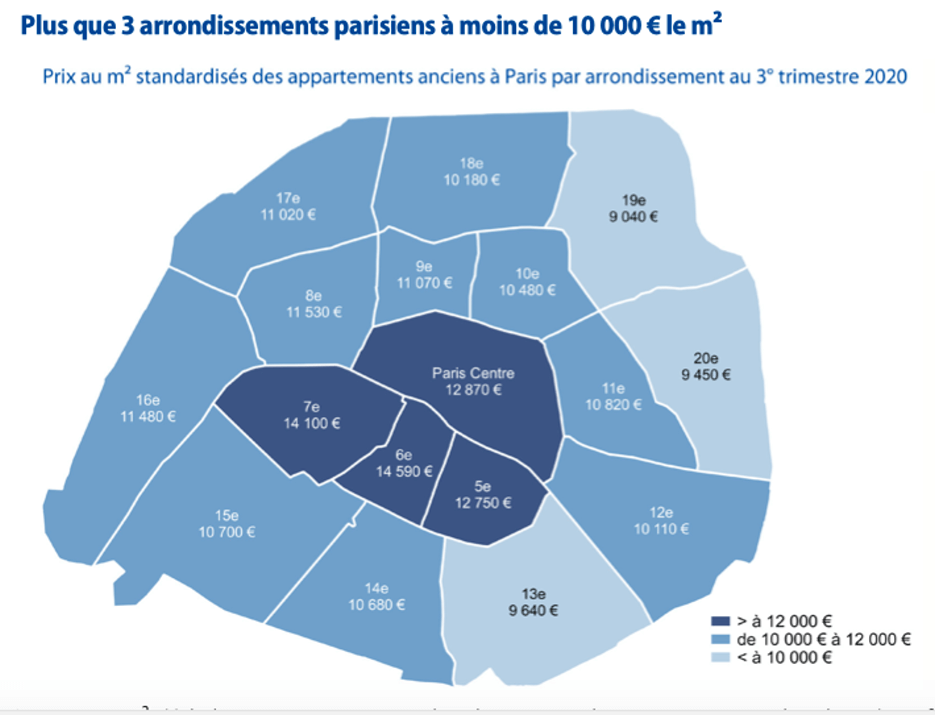

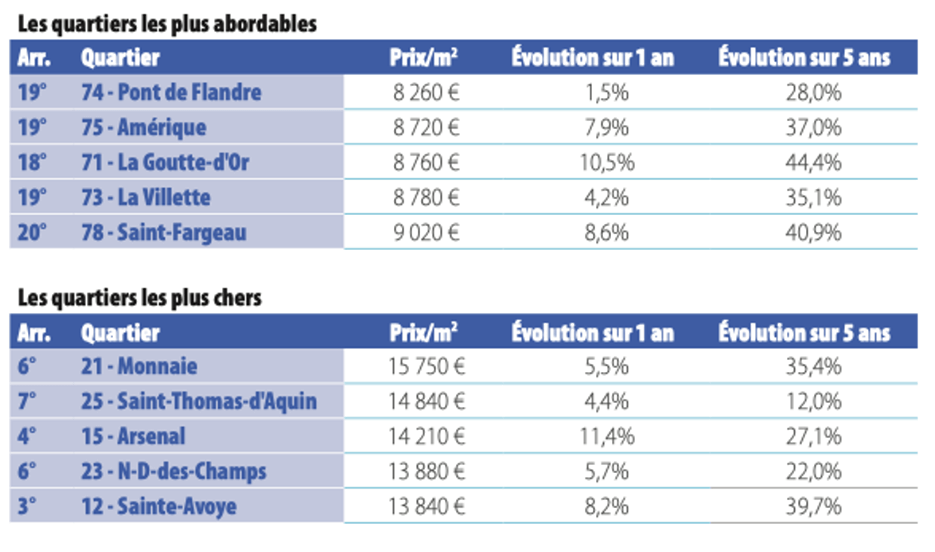

Note: As of the third quarter of 2020, prices in Paris per square meter range from €8,260 in Pont de Flandre (19th arrondissement) to €15,750 in the Monnaie district (6th arrondissement). The Monnaie district is 1.9 times more expensive than the Pont de Flandre district and €7,490 per square meters separates them.

To download and read the entire report, in French, click here.

To visit the interactive price chart for the Ile-de-France, click here.

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group

P.S. If you are considering a property purchase in France, don’t do it lightly. Let us help you make the smartest decisions to ensure you make the best investment you can. Contact us to learn more!

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.