Weekly insights about property in France!

Subscribe and don't miss an issue!

Trends and Price Evolutions in The French Real Estate Market

Volume XXIII, Issue 7

By Jay Corless, edited by Adrian Leeds

The following information is based on the report issued by the Chambre de Notaires on February 5, 2025:

The French real estate market has been on a rollercoaster ride over the past two years but is now showing promising signs of recovery. Recent data suggests that we have reached the nadir, with signs pointing toward stabilization and a potential upturn. Although the current outlook is more favorable than previous quarters, potential investors should remain cautious and well-informed. Economic shifts, regulatory changes, and external geopolitical events can still significantly impact market conditions.

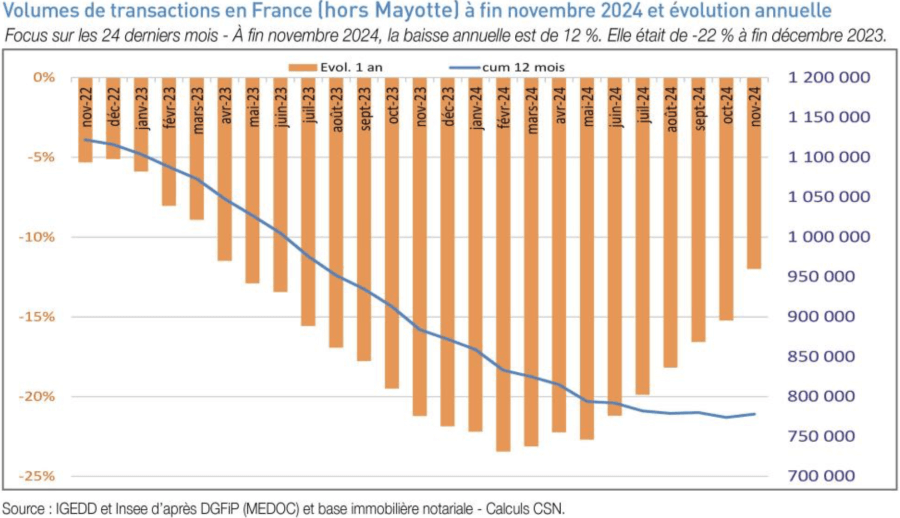

TRANSACTION VOLUMES: A GLIMMER OF HOPE

As of November 2024, the cumulative number of transactions for existing homes in France reached 778,000 over the past twelve months. This represents a decline from 872,000 in December 2023, marking a 12% annual decrease. This downward trend has significantly slowed since March 2024, when the yearly decline peaked at 23.4%. The current transaction volume reflects levels last seen at the end of 2015, indicating that the market is stabilizing. Despite this progress, regional disparities remain, with some areas experiencing a more significant recovery than others. Urban centers with strong employment growth are likely to rebound faster than rural regions with slow demand.

PRICE TRENDS: EASING DECLINES

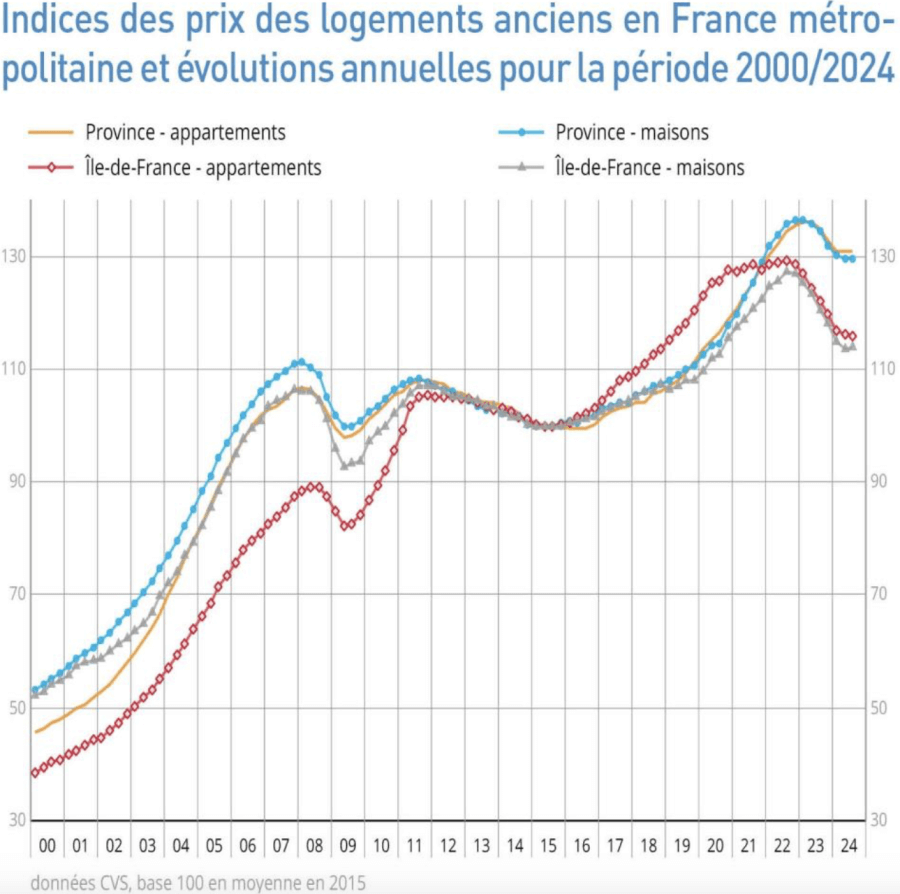

In metropolitan France, the third quarter of 2024 saw a 3.9% decrease in prices for existing homes, affecting both apartments and houses equally. Projections based on preliminary contracts indicate that this annual decline is slowing significantly, from 2.1% over 2024 to an anticipated 0.7% by the end of February 2025. By that time, prices are expected to stabilize across both market segments. This stabilization suggests buyer confidence returns, supported by more favorable lending conditions and government incentives to revitalize homeownership. However, affordability challenges remain for first-time buyers, particularly in major cities where prices remain elevated despite the overall market correction.

In the provinces, the annual price drop for existing homes was 3.4% in the third quarter of 2024. The decline was more pronounced for houses (3.6%) than apartments (3%). The annual decrease is expected to moderate to 1.5% over 2024 and further to 0.4% by February 2025. This suggests that regional variations will continue to shape price trends while the market stabilizes. Areas with strong economic drivers, such as significant employment hubs or regions with growing infrastructure projects, will likely recover faster prices. Buyers should pay attention to local market conditions when making purchasing decisions.

Île-de-France continues to experience significant price reductions, with a 5.3% annual decline in the third quarter of 2024. Houses and apartments both saw decreases of 5.3%. In Paris, the price per square meter is projected to reach €9,420 by February 2025, reflecting an annual decline of 1.4%, a notable improvement from the 7.7% drop observed a year earlier. While the market downturn has made Parisian real estate slightly more accessible, demand remains strong, particularly in well-connected neighborhoods. Investors should closely monitor shifts in rental demand and potential changes in municipal regulations that could impact long-term returns.

FACTORS INFLUENCING THE MARKET

Several elements are contributing to this emerging stability. The continued decrease in interest rates, bolstered by recent announcements from the European Central Bank and declining inflation in both the Eurozone and France, is enhancing the purchasing power of potential buyers who had previously been sidelined by unfavorable conditions. These developments foster a cautiously optimistic outlook, though the recovery remains uneven across different regions. Additionally, government initiatives to support homeownership, such as tax incentives and expanded loan programs, are expected to provide further momentum, reassuring stakeholders about the market’s future. However, ongoing global economic and domestic fiscal policy uncertainties could still pose risks to sustained market growth.

CAUTIOUS OPTIMISM AMID UNCERTAINTY

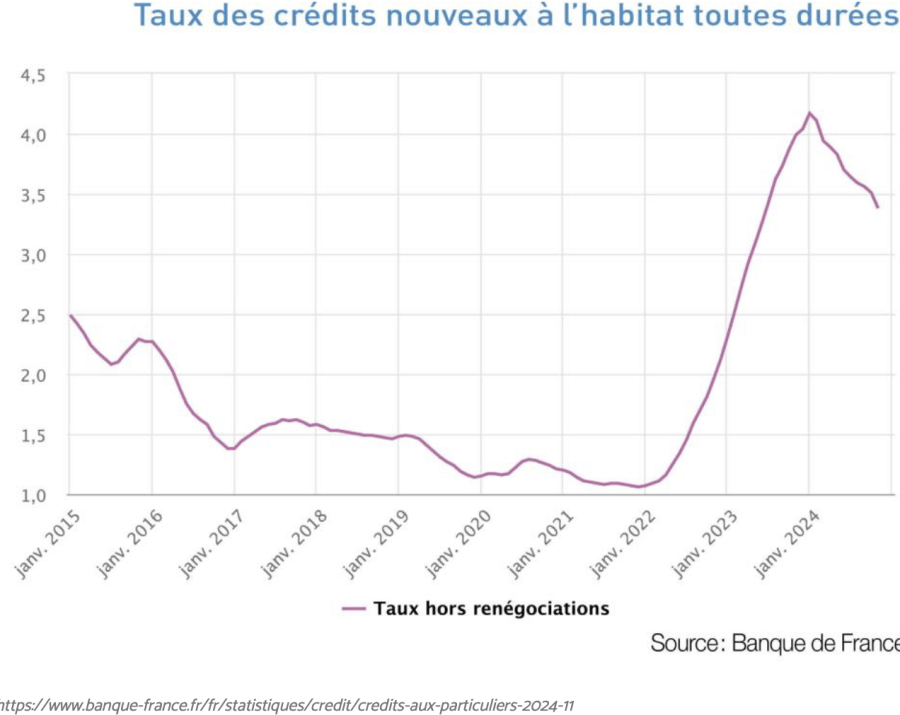

While traditional indicators suggest a more favorable environment, it’s essential to approach this optimism with caution. Geopolitical tensions, stringent budgetary constraints, and political instability continue to pose risks. According to the Banque de France, the average interest rate for new housing loans declined in January. However, the rise in the 10-year government bond yield (OAT 10 ans) could halt further rate decreases, potentially leading to stabilization at best. Additionally, consumer confidence in France is waning, with growing concerns that, while not directly tied to the real estate market, could influence buyer behavior. This underscores the importance of remaining adaptable and informed, as fluctuating economic conditions may impact purchasing power and investment potential, empowering stakeholders to make informed decisions.

LOOKING AHEAD

The recent downturn in the real estate market has impacted various stakeholders, particularly French citizens seeking housing. Although economic indicators for 2025 appear encouraging, the strength of the market’s recovery will largely depend on a stable economic and political environment that fosters confidence. Proposed measures to revitalize housing—such as boosting construction, implementing sustainable land management, and addressing energy-efficient renovations—are promising but must be effectively executed. For instance, boosting construction could increase the housing supply, while land management efforts could ensure sustainable development. However, if mismanaged, initiatives like restricting rentals of energy-inefficient properties and limiting land access could further diminish the housing supply. Moreover, investors should remain vigilant about shifts in taxation policies and regulatory frameworks that could affect profitability and long-term property values.

In conclusion, while the French real estate market shows signs of stabilization after a tumultuous period, the path to recovery is fraught with challenges. As the market navigates these uncertain times, stakeholders should remain vigilant, balancing optimism with prudent risk management. Buyers looking for opportunities should focus on well-positioned properties with strong long-term potential. At the same time, sellers may need to adjust pricing expectations to align with evolving market conditions.

See the January report PDF (in French).

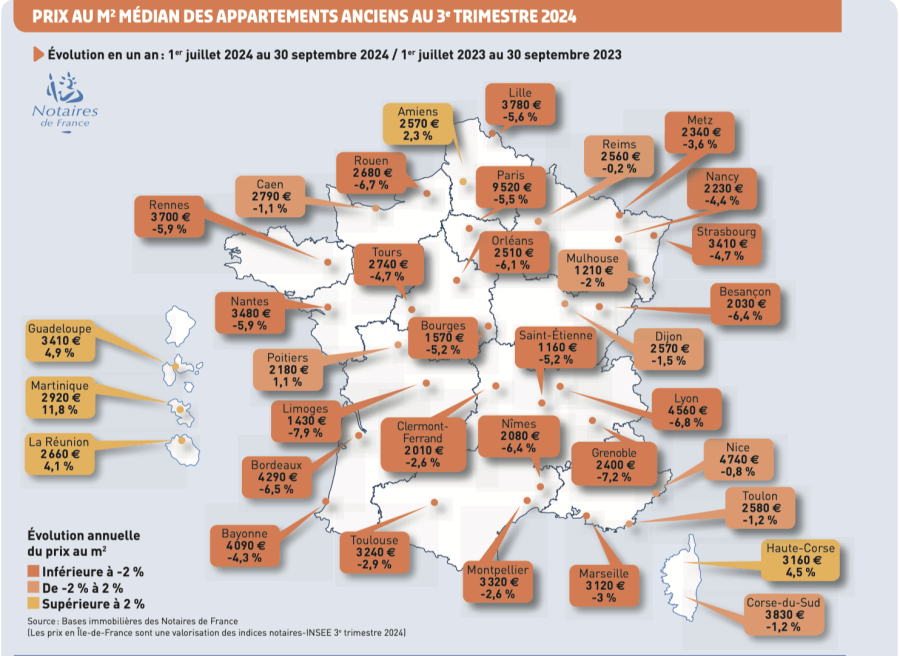

Note: Nice apartments saw the lowest decrease in value in all of France! We’ve seen prices rise in Nice exponentially compared to all other areas of France…for good reason! It’s the hotspot for retirees and you may love living in Nice as much our community there does!

We can easily assist you in finding your Nice dream home—our team on the ground in Nice is batting 1000! For more information, visit our website.

A bientôt,

Adrian Leeds

Adrian Leeds

The Adrian Leeds Group®

Adrian with Jason Gardner at Après-Midi in Paris (photo by Meredith Mullins)

P.S. We had an SRO crowd at Après-Midi in Paris on Tuesday that didn’t mind being wedged in to fit! The room filled up even before 3 p.m., the official start time, so we were able to get a head start and photographer Jason Gardner was ready to take the helm and make his presentation. Jason showed a healthy smattering of photos from his two books of carnivals from all over the world. What he has been able to document is fascinating and like nothing else any other photographer has accomplished, as he has spent 15 years ferreting out some of the most obscure festivals—most of which we’ve never even heard of. See the report, the photos and watch the video on YouTube.

Let Us create a custom strategy for you

You can live or invest in France-now.

Property for sale

what's happening

Check out upcoming events, conferences, or webinars. Join us!

GET FINANCING

Learn about French Property Loan Information.

Read & Subscribe

Dive into more by reading the Adrian Leeds Nouvellettre®

Better yet, subscribe to both and get the updates delivered to your inbox.

Get started with your dream of owning property in Paris.

Join us on Youtube

Dive into more on how to live, invest & escape to France

Be sure to subscribe!

To read more, click the links below.